Who’s on gilt watch?

Everyone’s hands should be raised.

The UK government bond market’s coming off a truly disastrous week that saw benchmark yields climb to the highest since 2008 and 30-year yields to the highest since the late 1990s.

Without mincing words, it’s a nascent crisis. Whether the tumult morphs into a full-blown panic remains to be seen. Over the weekend, while on a trip to China, Rachel Reeves said there have “undoubtedly been moves in global financial markets over the last few days.” It was an understatement, and a rather amusing one at that.

The simultaneous selloff in UK government bonds and the pound was dramatic enough to conjure the ghost of Liz Truss’s short tenure at No. 10. Indeed, if you don’t mind extrapolation, the current episode’s actually more acute than the Truss mini-budget boondoggle.

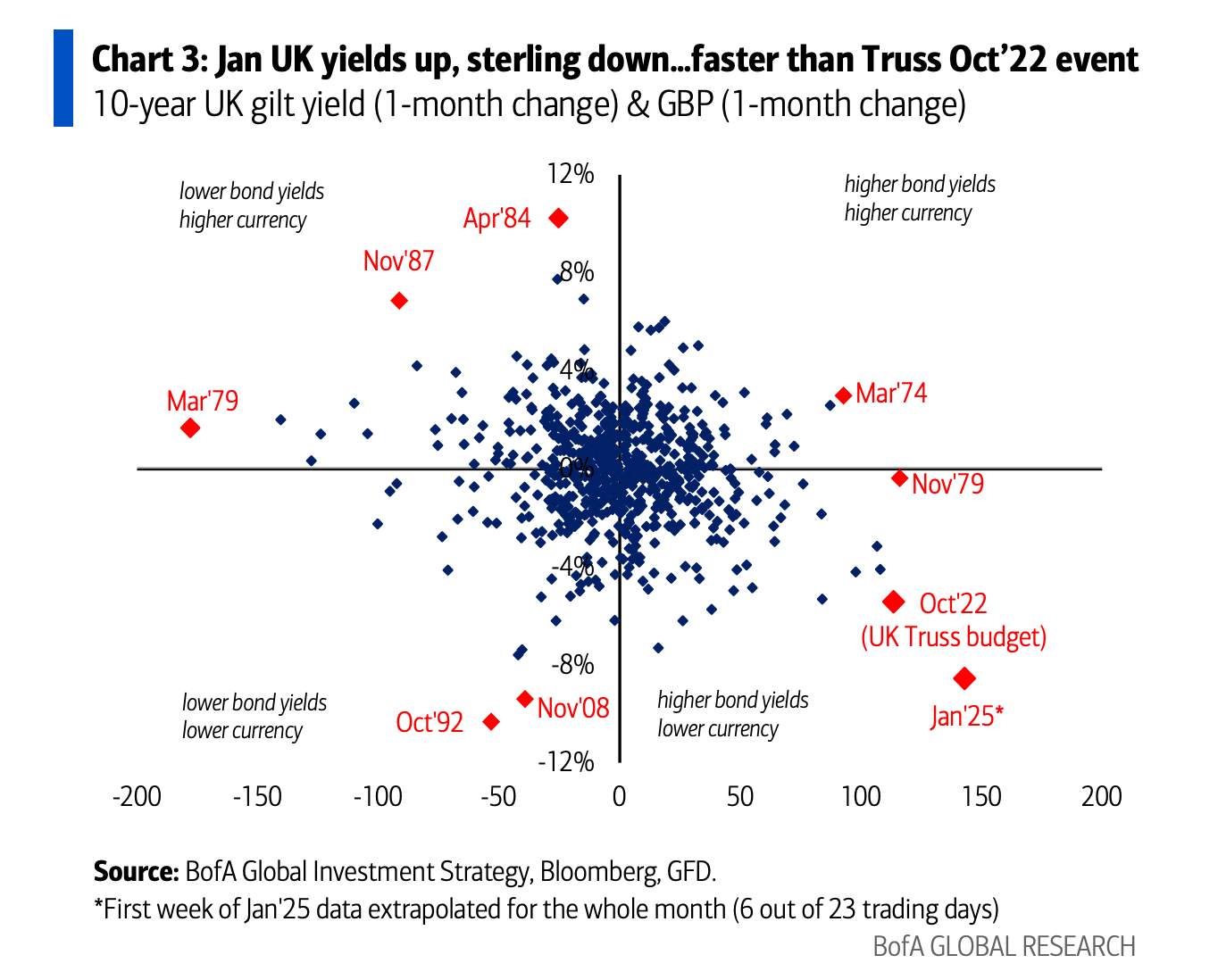

The scatterplot, above, from BofA, projects the MTD moves out to 23 trading days — in other words, it shows you how bad things would be if the rest of this month looks like the first half-dozen sessions of the year.

Again, the speed of these moves is quicker than the unraveling that occurred when Truss was in charge. And to reiterate: Theory suggests advanced economies shouldn’t experience simultaneous selloffs in their sovereign debt and in the currency. That’s the stuff of emerging markets, not hard currency-issuing, developed democracies.

Note from the figure above that if things keep going the way they’re going, sterling would fall ~8% on a rolling one-month basis. As it happens, some options traders are targeting just that. As Bloomberg noted, documenting the trades, “demand for pound options last week surpassed levels seen during [the Truss crisis] and even around the 2016 Brexit referendum.” (Emphasis mine.)

For those interested ahead of what promises to be an(other) thrilling week for UK assets, I’ll leave you with some color from Kit Juckes, SocGen’s widely-followed, veteran FX strategist. To wit, from Kit:

The similarity between what has gone into folklore as the ‘Truss Crisis’ and the current situation is that sterling and gilt yields have moved sharply in opposite directions. The extent of the move is much smaller so far, and I doubt it will become as critical. In 2022 a new PM, with her new Chancellor, came up with a bafflingly ill-considered set of Budget proposals and triggered a crisis of confidence. Even then, the September 2022 fall in GBP/USD from 1.16 to 1.05 was fully reversed by the end of October and so was the spike in gilt yields. What has happened this time, is that the increase in employers’ national insurance contributions announced at the Budget appears to have put the brakes on growth to a greater extent than (I, for one) expected. Deteriorating public finances may force unhelpful fiscal tightening sooner than expected. A global bond selloff doesn’t help and gilts having a worse time than others support the idea that the pool of investors who will step in to ‘buy the dip’ in gilts isn’t what it was pre-Brexit. Especially in thin post-New Year markets.