Are we still living in a FOMO regime?

How would one go about determining such a thing?

Those aren’t random questions. At various intervals, you’ll hear me talk about “fear of the right-tail,” where than means market participants are more concerned about missing a rally than hedging downside.

That’s a fairly common occurrence in the era of unchecked gains for AI beneficiaries and generalized “sky’s the limit” sentiment around mega-cap names which, notwithstanding antitrust litigation, are thought to have virtually unlimited upside thanks in no small part to the very same monopoly dynamics that’ve landed America’s most successful tech companies in the regulatory and political crosshairs.

In the equity options space, FOMO manifests as, among other things, expensive upside and, relatedly, the sometimes perilous “spot up-vol up” conjuncture. With that in mind, consider the figures below, from SocGen’s Jitesh Kumar and Vincent Cassot.

The figure on the left shows the spread between “down” vol and “up” vol. The header says it all: US shares remain more volatile in rallies than in selloffs. The scatter plot on the right gives you some additional context. When equities exhibit more volatility in up moves than in downdrafts, that’s a FOMO regime.

Regular readers will harken back to “Skew Has A Story To Tell.” If you’re underexposed to equities, you have to grab for upside optionality into any burgeoning melt-up, lest you should underperform. The corollary is subdued demand for downside protection — because you don’t need to hedge exposure you don’t have. Hence the very flat skew and put skew and very steep call skew environment observed periodically over the past two years.

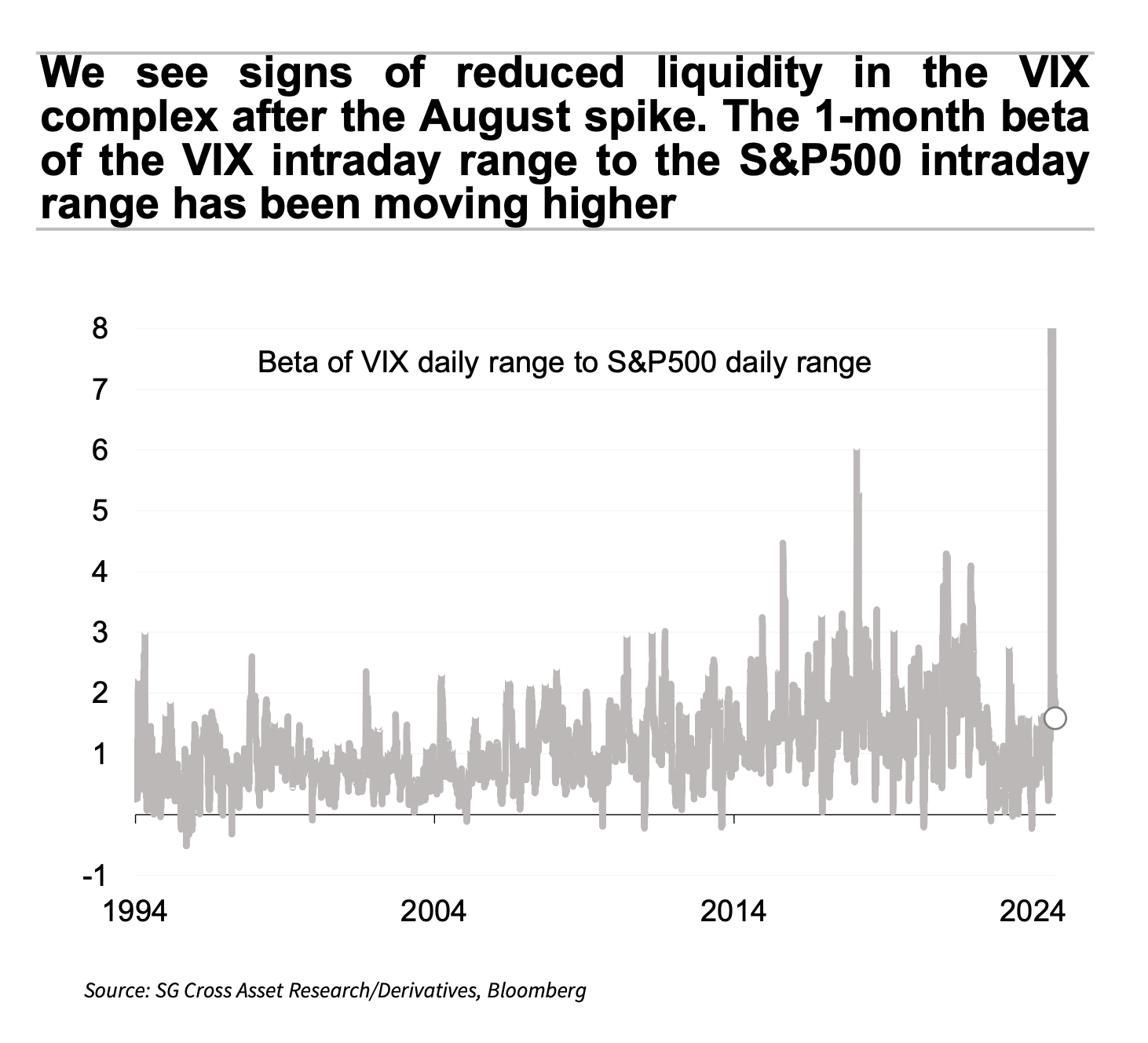

More recently — i.e., over the last two and a half months — we saw bursts of downside hedging into the burgeoning US growth scare, leading to steeper skew and steeper put skew, alongside violent vol-of-vol shocks and extremes in VIX beta to spot equities, which in turn suggests liquidity issues in the VIX complex where dealers short upside have struggled to recycle risk.

{kind=link}

Combine the info H presents here w/ comments about “wealth effect” in The Daily, “Promises, Promises,” and other recent Fed meeting-related articles, and what do we have? No risks anywhere; Father Fed sees the future for us and proclaims it perfectly balanced for months ahead.