In his pivotal Jackson Hole address, Jerome Powell said that in his view, it “seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon.”

That sentence presaged what quickly became the speech’s most oft-cited line: The Fed, Powell went on, does “not seek or welcome further cooling in labor market conditions.”

And just like that, the Fed had adopted a de facto single mandate, this time focused on jobs. For two years, the Fed actively sought a softer (but certainly not a weak) labor market in the service of corralling runaway wage growth, which threatened to exacerbate inflation. As of Jackson Hole 2024, Fed policy would be leveraged to prevent labor market softening.

Far from the conditions which prevailed in 2021 and 2022 — when some economists feared a wage-price spiral — the US labor market’s now generally balanced, according to key metrics like the job openings to unemployed ratio. Although workers still have more leverage than they did pre-COVID, it’s probably not enough to sustain wage growth at “dangerous” levels going forward.

I put the word dangerous in scare quotes because how you think about this situation depends a lot on which side of the system you’re on: Capital or labor. Labor, as an economic actor, is effectively being told that their own demands for higher pay to keep abreast of inflation are in fact the source — or one source — of that same inflation. Workers, capital says, should do themselves a favor and stop asking for higher pay and better benefits. If not, prices for the goods and services they buy when they’re not working will keep going up.

If that strikes you as cruelly ironic — and if it also seems to you that labor habitually finds itself in lose-lose situations, leaving capital to reap the many benefits of a structural “heads we win, tails you lose” conjuncture — it’s not your imagination. This is capitalism. You can’t spell it without “capital.”

Anyway, Powell’s probably right. The figure below, from Goldman’s David Kostin, shows the share of S&P 500 companies who mentioned labor shortages on last quarter’s earnings calls.

Suffice to say that’s just one more metric which is now back to pre-pandemic levels. If you’re not short on labor, you’re not gonna pay up to get it.

This is good news for capitalists and the people to whom they’re beholden: Shareholders.

“Wage growth has decelerated and reflects the loosening of the labor market indicated by both macro and micro data,” Kostin wrote, in his latest, noting that Goldman’s in-house wage tracker sits at around 3.9% YoY. The high on that measure was 6% two years ago. As the figure on the left, below, shows, a leading measure — derived from forward-looking surveys — suggests wage growth should slow to around 3%, which is generally viewed as consistent with consumer price stability overall.

The figure on the right, above, gives you a sense of the read-through for corporate bottom lines. Corporate America’s EBIT margins naturally expand when the prices companies charge consumers outstrip the cost of the labor required to produce products and services. Although core inflation’s obviously moved lower, recall that unit labor costs grew at just 0.3% on 12-month basis in Q2, the slowest in over a decade.

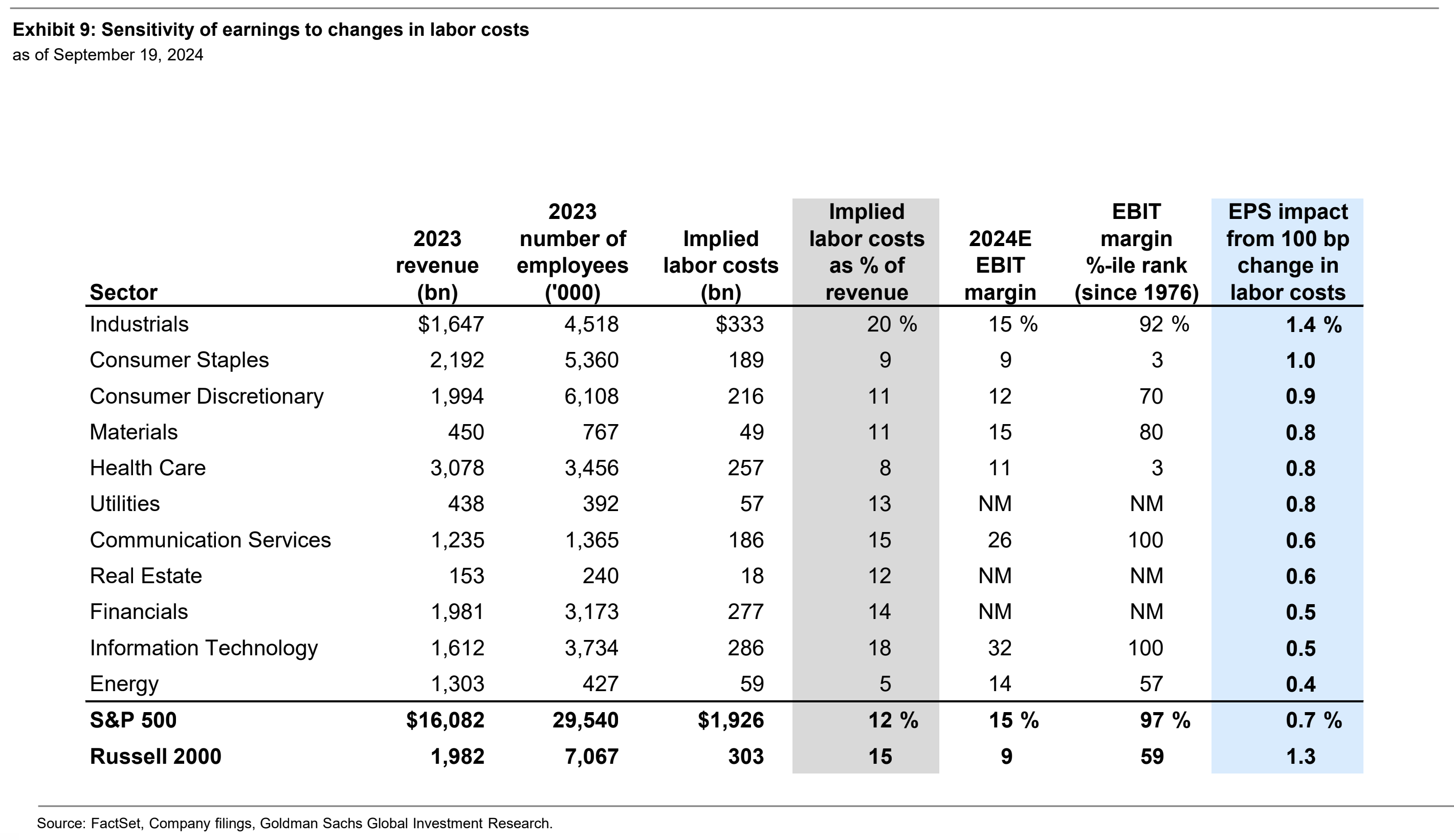

As with everything else in American society, including and especially the capital versus labor debate itself, this is a “haves” / “have-nots” story. “EBIT margins for the S&P 500 and most sectors sit at or above their 30-year averages,” Kostin remarked, before noting that Russell 2000 EBIT margins, by contrast, “are much lower, making small-caps more sensitive to shifting wages.”

On Kostin’s math, a 100bps change in labor cost growth impacts S&P 500 bottom lines by just 0.7%. The figure for the Russell 2000 is twice that.

{kind=link}

{kind=link}

The American polity’s contradiction is best captured through capitalists pretending to be laborists most notably on the right. This is best represented by the old adage of “pulling yourself up by your bootstraps” that many on the right pretend to espouse to make themselves appear to be middle class. If you look at the background and education of most of the right wing congress their life experience isn’t even close to middle class so instead they embrace these euphemisms to fool people into thinking they are aligned. These bootstrap pullers will espouse labor being a priority and how much they love “small business” (the backbone of America and such). But in reality they vote and write polices that alway favor Capital over Labor and thus reveal what Capitalists truly value (Capital itself). The fact that the Supreme Court, who must have seen an opportunity in the Citizens United ruling for their backchannel favors to themselves, says Capital can be considered “people” makes this whole scenario and easy playbook. While these same people espouse laborist euphemisms they attack the party that most aligns with labor as “socialists” (as if bailing out and giving tax breaks to corporations isn’t socialism). This post has me pondering a new strategy that democrats may want to lean into. Flip the “socialists” slander on its head and instead subscribe themselves to be laborists. Most voters are in fact laborers and the pain that the right plays these voters on are in fact the Labor/Capital divide that has disenfranchised most of them for the past 50 years. Labor really doesn’t have an official party in the US (unlike in the UK) and since the GOP is the party of Capital it only makes sense for Democrats to make themselves the party of Labor.