One way or another, this’ll be a two-day week for a lot of US market participants.

Wednesday’s a holiday, and people tend to plan vacations around holidays, so some folks won’t be on the desk at all. Others are currently enjoying a five-day weekend. They’ll show up (or log in, whichever the case might be) on Thursday. Still others will show up Monday, work two days, then take Thursday and Friday off making next weekend a five-day recess. Anyone who’s around post-Wednesday will be tuned out even if they’re clocked in.

That’s not to say the week’s destined to be a total loss. The US isn’t the only market in the world, believe it or not, and besides, the docket stateside isn’t blank. Retail sales figures are on deck, for example.

Nominal spending probably advanced 0.3% in the US last month. According to economists, anyway. Recall that spending was tepid in April.

I wouldn’t call the release mission critical, exactly, but a miss (and particularly a downside surprise on the control group) would add to a string of releases which together suggest the establishment survey in the jobs report has become an outlier — that notwithstanding the NFP headline and the seasonally adjusted AHE prints, the US economy’s decelerating.

The Atlanta Fed GDPNow tracker’s showing 3.1% for Q2. That’s hardly slow. In fact, it’s well above-trend. As the figure below shows, the most widely-cited “nowcast” inflected meaningfully in recent days.

Still, it’s more than a full percent off the modeled pace in early May, and 0.4ppt of the current reading is attributable to the May jobs report.

The first of this month’s US housing releases (covering activity in May with the exception of NAHB, which captures builder moods for June) are due as well, starting with builder sentiment scheduled for Wednesday’s holiday. The NAHB gauge is seen below the 50 demarcation line separating net optimism from pessimism for a second month. Housing starts are due on Thursday (consensus sees a second straight monthly gain) and existing home sales for May on Friday (economists see another decline, the third straight and the 23rd in 28 months).

Anyone who bothers to tune in on Thursday will eye initial jobless claims closely. Last week’s update saw the headline claims print jump to 242,000, the highest since August. The next release will cover NFP survey week for June. In addition to existing home sales, Friday also brings flash reads on S&P Global’s PMIs for this month.

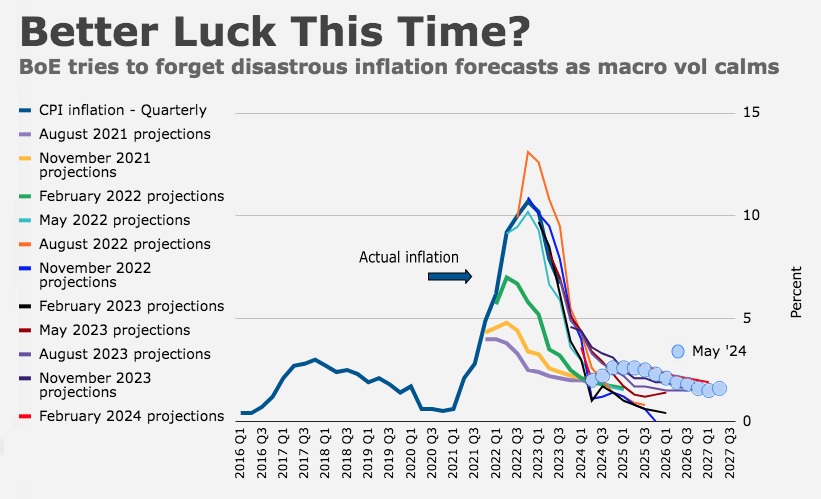

Across the pond, the Bank of England will likely hold rates on Thursday. The optics of delivering the first cut of the cycle with just two weeks to go before an election would be challenging, to put it politely. Not that it matters: The Tories are set for an epic wipeout regardless. The BoE can argue the August MPC makes a better venue given it’ll feature new forecasts (because we all know how accurate those tend to be).

A day earlier, a fresh read on inflation may well show headline CPI in the UK receded to target last month. If that comes to pass, it’d be the first on-target print in three years.

Core price growth’s still running above 3% in the UK, though, and services inflation’s double that.

Elsewhere, the SNB could conceivably cut for a second straight meeting (remember, they only meet once per quarter). Norway and Australia will probably keep rates on hold.

Finally, China will release activity data for May. The focus there will be on the so-called “two-speed” recovery, where that means market participants will be keen for any evidence that Chinese consumers are feeling marginally better about the outlook. The juxtaposition between moribund retail sales and accelerating industrial production is a source of consternation for politicians in Western capitals to the extent it points to an overcapacity problem that’ll eventually be exported to the rest of the world at the expense of local industries.

Coming full circle, BMO’s US rates team wrote that Wednesday’s market holiday “has effectively split the week ahead into two 2-day workweeks, the first containing the May retail sales data, and the second offering the five-year TIPS auction and the next (now very topical) update on the employment market in the form of initial jobless claims for NFP-survey week.” “Both of these ‘weeks,'” the bank’s Ian Lyngen went on to say, “are prime candidates to be converted into a five-day weekend — the truest sign that summer trading conditions are rapidly approaching on the macro horizon.”

{kind=link}

So if you were actually to take a vacation, what would you do with yourself?

It’s Disney Land, isn’t it? You’d totally go to Disney Land.

Not in a men’s drum circle around a vortex generator in Sedona, AZ??

Why settle for just one when you can have both?

‘Ti’s the American way. Debit, Credit or Affirm for those sir?

I almost choked on my coffee laughing….. I just returned from Sedona yesterday, though no drum circle at a vortex for me. Fantastic hiking though! I highly recommend for anyone who loves to hike but doesn’t mind dry, dusty heat.

“Still others will show up Monday, work two days, then take Thursday and Friday off making next weekend a five-day recess. Anyone who’s around post-Wednesday will be tuned out even if they’re clocked in.”

I don’t understand this comment from a work ethic standpoint. These people are well-compensated, financial professionals. If they are clocked in, why wouldn’t they be putting in an honest day’s work irrespective of the holiday week?