Jerome Powell’s timeline for Fed confidence in the durability of the disinflation trajectory, and thereby for the onset of rate cuts, served as the title for the latest installment of BofA’s popular weekly “Flow Show” series.

“We’re not far from it,” Powell told the Senate this week. Those five words were rally fuel. To some (many), they were another example of the Fed’s incurable penchant for inflating bubbles.

“[The] Fed causes bubbles and the Fed pops bubbles,” Michael Hartnett wrote. “In 2024, the Fed’s determination to cut rates means ‘we’re not too far from it…'”

A week ago, I noted that the four-month rally in US equities was among the largest in a decade. Hartnett did the five-month lookback (figure below).

“Stocks’ ferocious +25% gain in five months has happened just 10 times since the 1930s,” he wrote, adding that typically, these kinds of upswells “occur from recession lows or at the start of bubbles.” He cited 1938, 1975, 1982, 2009 and 2020 as examples of the former. And January 1999 as an exemplar of the latter.

So, are we doomed? Condemned to look on helplessly as this castle in the sky disintegrates like so many other Fed-fueled delusions?

Yes. No. Maybe? Nobody knows. And remember: It’s not exactly as if this ostensible bubble has inflated on the back of easy monetary policy. Maybe Fed funds isn’t nearly as restrictive as policymakers believe (Loretta Mester reiterated this week that the neutral rate may well be higher), but amid the catcalls, we shouldn’t lose track of the fact that this is a Fed holding terminal north of 5%. Not a Fed cutting rates to the lower bound into a mania.

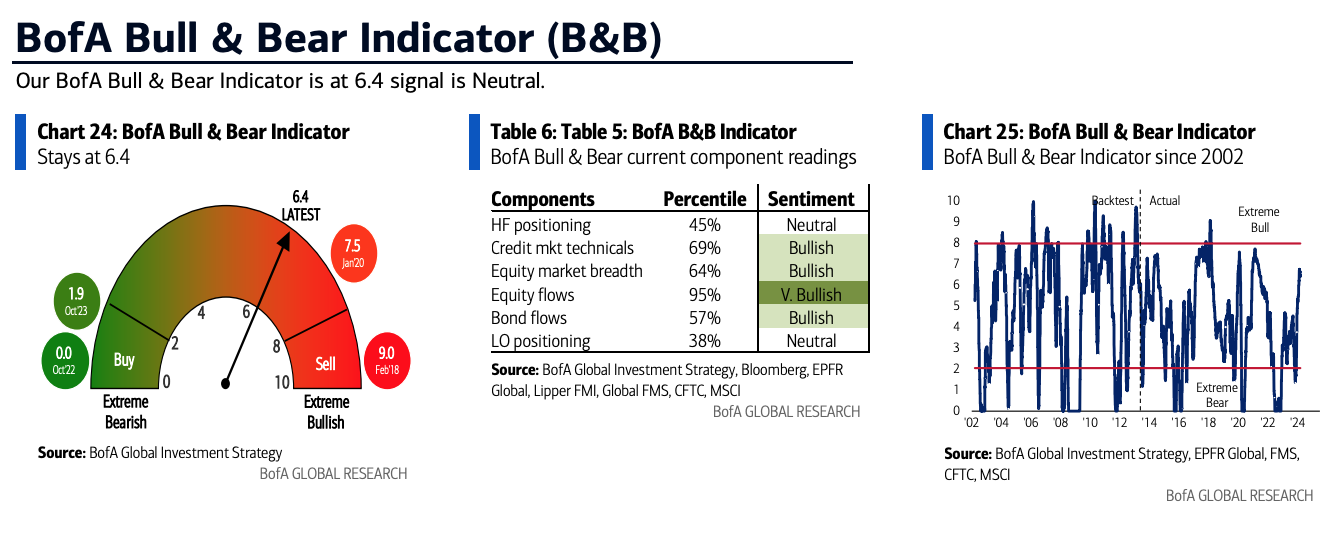

The figures below give you a clue as to what could curb the risk-asset frenzy.

Hartnett suggested a “combination” of a BofA Bull & Bear Indicator above 8, 10-year reals above 2.5% and a trailing multiple in excess of 25, could be a “run-for-the-hills” moment.

“Stretched and extended we are, but [the] history of bubbles shows it can go further,” he went on. 2024’s “cynical bulls” are “determined to stay long until the day before the Fed cuts.” Until then, Hartnett said, “only a negative payrolls print in the near-term is likely to melt [bulls’] determination.”

For what it’s worth, BofA’s Bull & Bear Indicator is at 6.4, well short of a contrarian “sell” signal. Savita Subramanian raised the bank’s official house S&P target to 5,400 late last week.

{kind=link}

Good info–thanks.

Harnett may be correct that “cynical bulls” will hang on until the day before first rate cut, but I doubt most wait until then.

The longer the Fed waits, the faster and harder they will have to cut….pay me now or pay me later….