Year-ahead outlook pieces from Wall Street are replete with references to a navigable but narrow path to a benign macroeconomic outcome following the most significant coordinated monetary tightening in modern history.

You can pick your metaphor. “Threading the needle” will work. So will “sticking the landing.” Morgan Stanley’s cross-asset strategy team employed both in one section of a six-dozen page 2024 global strategy outlook.

“For investors, 2024 should be all about threading the needle,” analysts including Serena Tang and Vishwanath Tirupattur wrote. In the bank’s baseline, growth slows, inflation falls and the door opens to easier monetary policy.

“We’d need to see the macro outlook sticking the landing across all of these to justify current valuations,” the bank said, adding that “many assets are already fairly priced for this benign environment.” The emphasis is in the original. The implication is that because markets have already priced a threaded needle, valuations across some asset classes, particularly US stocks, are vulnerable in the event the landing is rough.

“The eye of the needle is smaller and narrower than usual,” the bank went on. Here are the late-cycle risks, as enumerated by Morgan Stanley:

- Financial conditions are tight.

- Rate cuts generally aren’t expected until later in 2024.

- Downside risks to global growth are high.

- An earnings recession is still in train.

- Bond supply continues to be a market concern.

- EM fundamentals face headwinds.

- Cross-asset correlations have not budged from extremes.

- Finesse will be needed to find openings in markets which can generate positive returns.

“Finesse.” I like that. In order to successfully navigate these potentially treacherous waters, investors will need to employ finesse. “Feel the market!” as one former US president famously shouted, during the worst December for US stocks since the Great Depression.

Fortunately, Morgan Stanley likes the odds of threading this needle — sticking this landing. “Consensus now has consolidated around the narrative of a ‘soft landing,’ and we agree,” the bank said.

The economics team expects below-trend growth eventually, but the expansion should nevertheless remain healthy, where that means 2.8% global growth. US core inflation should recede to 2.6% by year-end 2024.

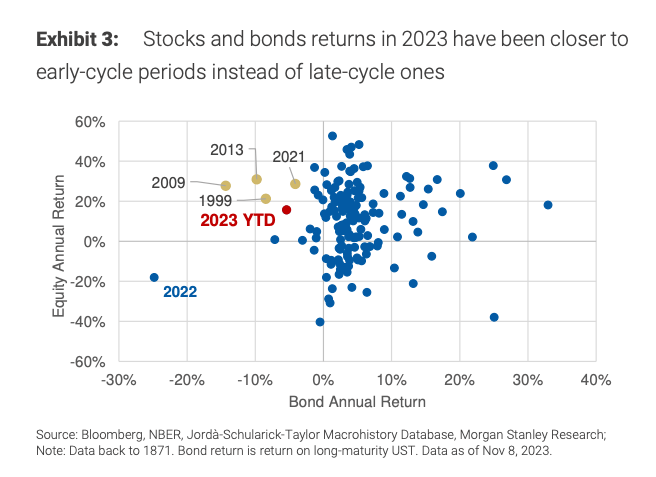

That’s the good news. The less good (but not necessarily ominous) news is that “most of this benign scenario… is already reflected in valuations, especially after the recent rally,” the bank said, adding that stock and bond performance in 2023 was mirrored in just a handful of other years, namely 1999, 2009, 2013 and 2021.

“In every single one of these episodes, US PMIs rebounded rapidly from troughs and marked the start of a new market cycle,” Morgan Stanley’s strategists wrote, before spelling out the (potential) problem: “In other words, markets seem to already assume that central banks can stick the landing. There is little room for error as far as valuations are concerned.”

Notably, references to valuations having already priced a benign macro outcome (a “threaded needle”) seem to mostly reference US equities. On a 10-year lookback (which admittedly may be insufficient if we’ve reverted to a pre-Great Moderation macro regime), only US stocks look rich.

In any case, Morgan Stanley proceeded to detail their expectations for monetary policy, credit risk, the Chinese economy, earnings and the dollar. In every case, they’re cautiously optimistic. To wit:

- Central banks will have to get the balance correct between tightening just enough and easing quickly enough. DM policymakers should largely succeed, and we expect the Fed and ECB to both make their first rate cut in June, helping to manage a glide lower in growth and inflation.

- We are also encouraged by corporates’ ability to push out maturity walls, as capital markets have stayed open for refinancing, and private credit markets provide a release valve for lower-quality names. There is a tail of names who may find addressing the maturity wall next year difficult… but high-quality credit should fare well, supporting valuations.

- A key risk identified by our China economists and strategists is that China could fall into a structural debt-deflation loop, dragging down earnings and growth. This is not our base case for China and we think that the economy can find its balance.

- Our N12M expected returns across the major equity markets are comfortably positive. However, to justify [current] levels of equity risk premiums and to achieve these levels of expected returns requires stocks to overcome an earnings recession in the US — we see earnings troughing in early 2024 and staging a durable recovery thereafter.

- The story for 2024 will likely be a tale of two halves, especially for USD: With US growth still relatively strong in H1 and the risk-off environment from stocks and earnings troughing early next year, we forecast the DXY to rise to 111 by the spring. From Q2 onwards, with US growth softening and cuts being priced in, USD can weaken slightly to end the year at 107.

So, everything is generally expected to resolve in reasonably benign fashion.

Again, this is all predicated on what the Fed’s Austan Goolsbee last week described as “the golden path” — inflation that returns near target with no severe downturn.

Valuations in some assets, Morgan Stanley reiterated, “reflect the expectation that all of the above happens just right and that macro and markets normalize without a hitch in 2024.” “Such a perfect landing is hard to pull off,” they added.

I’ve read a few items this morning that brought up stress in some originators of Freddie and Fannie mortgages, suggesting there is stress brewing there that so far is “below the fold” of awareness but may be a rising concern as QT etc continues to pinch some of these companies.

Meridian Capital Group has been the No 1 originator so far in various mortgages. Something to keep at eye on while “threading the needle.”