Fed hikes made cash great again. (Please don’t send me any novelty red hats.)

From a fund flows perspective, cash is the story of 2023.

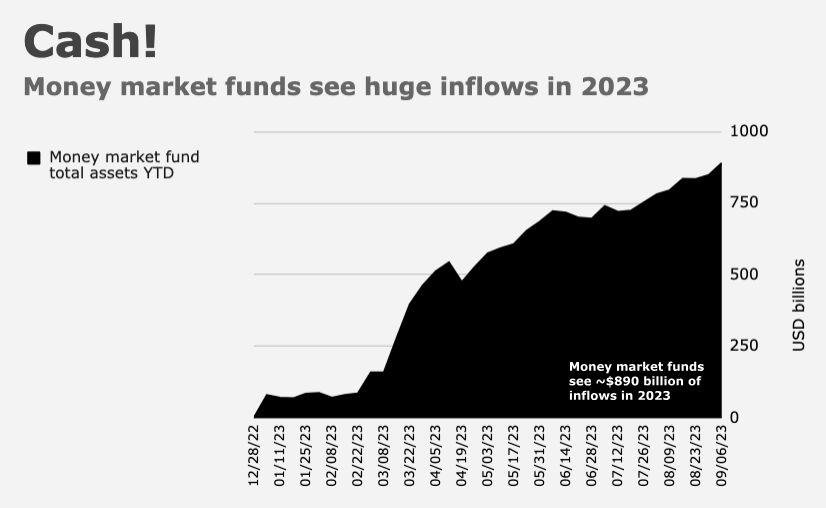

Globally, money market fund inflows now exceed $1 trillion, eclipsing 2020’s full-year haul, no small feat.

On ICI’s data, US money funds took in $890 billion for the year through last Wednesday.

To be sure, there’s a lot to be said for being able to sleep well at night. I speak from experience. From 2008 to 2016, most of my nights were more or less sleepless for different reasons. So, the premium I attach to safe-sleeping is probably higher than what most regular people would assign. But even for me, the disparity between equities’ performance in 2023 and sleep-safe cash yields is large enough to be irritating.

I don’t know how much safe sleep is worth to you, but with the Nasdaq 100 up ~40% in 2023 and government money funds yielding around 5.3%, sleeping has been an expensive proposition when denominated in opportunity costs. (Although after so many years in ZIRP limbo, I still occasionally do a double-take when I look at the line item on my monthly statements that corresponds to payouts from federal money market funds.)

“We all understand that in the post-2022 global tightening cycle world, cash is an asset class again [but] the trend in the equities space since SVB completely altered the vol regime has been ‘Fear Of Cash Underperforming Stocks,’ as investors who moved their money to the sidelines have witnessed their +4-5% returns being lapped by the S&P 500 Total Return’s +18.2% YTD, and Nasdaq 100 Total Return at +42.2%,” Nomura’s Charlie McElligott remarked on Tuesday.

None of this is lost on the marketing geniuses at ETF houses. They’ve “exploit[ed] this FOMO opportunity beautifully, sensing the investor demand for cash, income and capital appreciation,” Charlie wrote, flagging “big flows for yield enhancement and income strategies which sell vol to generate premium income, but against owning underlying stocks for the appreciation.”

That’s playing out alongside the vol risk premium-harvesting and systematic gamma selling documented by McElligott for months.

The result: “A non-stop index-level vol crush, with mass options / gamma supply being generated,” mostly since SVB and the attendant emergency actions, which were seen in many corners as tantamount to a policy “put,” even as Jerome Powell continued to hike rates.

Official intervention in March “has increased the perception that the ‘hawkish left-tail’ was removed at the same time that inflation began to soften [while] the US consumer remained insulated from [higher] rates with labor and wage growth remaining so robust,” McElligott went on. “[The] potent mix of persistent vol supply, alongside the culling of left-tail catalysts and re-pricing higher of ‘soft-landing’ odds has seen vol splattered.”

{kind=link}

Yeah, but trades like that have a habit of working until they don’t, “don’t” usually represents an explosive mean reversion that wipes out the bag holders.