The US probably isn’t headed for a recession anymore.

That’s according to BofA, which this week became the first major Wall Street bank (that I’m aware of, anyway) to switch their base case for the world’s largest economy to soft landing from mild downturn. I could be wrong (i.e., maybe someone else already adopted a soft landing house view), but it’s a notable call regardless.

“Recent incoming data has made us reassess our prior view that a mild recession in 2024 is the most likely outcome,” analysts including Michael Gapen said, in the course of lifting their forecast for personal consumption, and pushing back their call for a spending slowdown to Q3 2024. Previously, the bank saw a contraction in spending during the first half of next year.

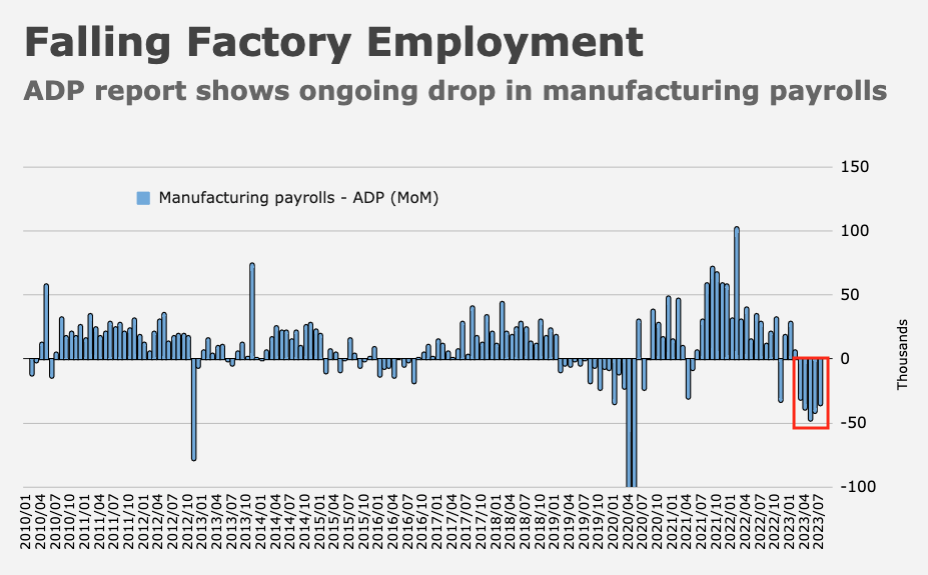

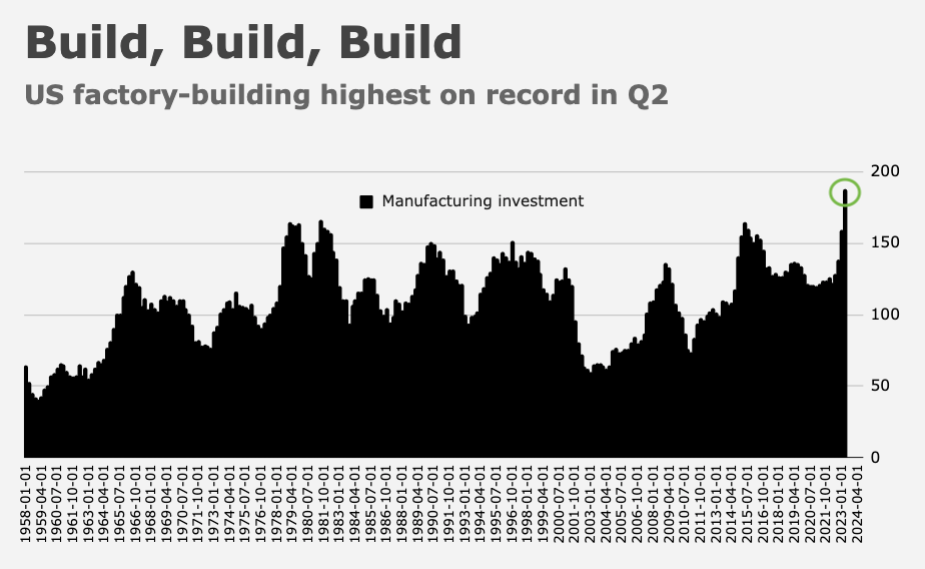

They also “carried forward” the momentum in nonresidential fixed investment evidenced by the advance read on Q2 GDP. Note that America’s manufacturing malaise and an attendant multi-month slide in factory employment belie record factory building. BofA also expects continued abatement in the drag from residential investment. The housing sector, the bank said, “is finding a bottom.”

Although Gapen also revised the bank’s projected inflation path (higher), it was a benign revision — “a longer glide path,” as he put it, with slightly higher price growth persisting into 2024 and 2025, when core PCE will be 2.8 and 2.2%, respectively. The outlook for inflation in the near- to medium-term has improved, and that, in part anyway, informed BofA’s soft landing call. “[The] resiliency in activity and labor markets has not prevented softening in inflation and wages,” Gapen wrote.

The upshot: A soft landing is now more likely than even a mild recession. To wit, from BofA:

We take on board the signal from the incoming data and we revise our outlook in the direction of a “soft landing” in the US economy. By soft landing we mean growth that dips temporarily below trend without turning negative. In contrast, our prior outlook had a shallow decline in activity in the first half of 2024, with growth in GDP falling by 1.0% and 0.5% QoQ SAAR in Q1 and Q2, respectively. In short, our revisions imply we no longer expect a mild recession and, instead, think the economy may be able to skirt one.

There were caveats, of course, the most obvious of which is just that a mild recession is still eminently possible. The US economy, BofA emphasized, “is not entirely out of the woods.”

The other caveat is also a corollary — a resilient economy and above-target inflation mean the Fed will have a hard time justifying aggressive rate cuts.

“In a soft landing, the Fed will be a ‘cautious cutter,'” Gapen wrote. He now sees the first cut in June of next year compared to May previously.

“We think there are less obvious reasons for the Fed to move to rate cuts quickly in our new outlook [as] positive growth and low unemployment may mean the Fed needs more evidence inflation is indeed moving toward its target to cut,” BofA went on, adding that Jerome Powell “may be reluctant to declare victory in the face of still-tight labor markets.”

Why June for the first cut and not later in the year? Well, because Powell may want to avoid the appearance of politicized monetary policy. As Gapen put it, “2024 is an election year and we think it would be easier for the Fed to start any easing cycle earlier than later.” BofA expects 75bps of cuts in 2024, 100bps in 2025 and “normalization” in 2026.

I’d gently suggest that no matter how hard Powell tries, he won’t likely be able to avoid accusations of politicization. Quarterly cuts next year commencing in June would mean 50bps by election day. If inflation isn’t back to target by then, or the economy isn’t in recession, some Republicans on the Hill will insist that Powell (who’s a Republican) is working to undermine Donald Trump, assuming he’s still on the ballot by then.

Although it’d be a mistake of put too much emphasis on one bank’s call, it’s difficult to overstate how long the odds were (and, many would argue, still are) on the Fed landing this particular plane with casualties limited to SVB, Signature and Silvergate. We’re talking about 525bps of rate hikes in 16 months off the lower bound, and after a dozen years spent in a regime where price discovery was de facto illegal.

It’s a small miracle there’s anything left of markets.

{kind=link}

{kind=link}