One, among many, criticisms bears level against 2023’s equity rally centers on the notion that stocks are untethered from real yields — that equities are ignoring gravity.

It’s a compelling argument, but then again, so are quite a few of the other complaints bears keep on their “let me count the ways” list of reasons for despising a melt-up which has the S&P within ~250 points of January 2022’s record.

As a reminder that no one needs, real yields can be kryptonite for risk assets. When they rise, financial conditions generally tighten and vice versa.

From 2015 through late last year, the inverse relationship between reals and equity valuations was incredibly tight. Then, in 2023, it broke down. The two diverged, as illustrated above in the figure from Goldman.

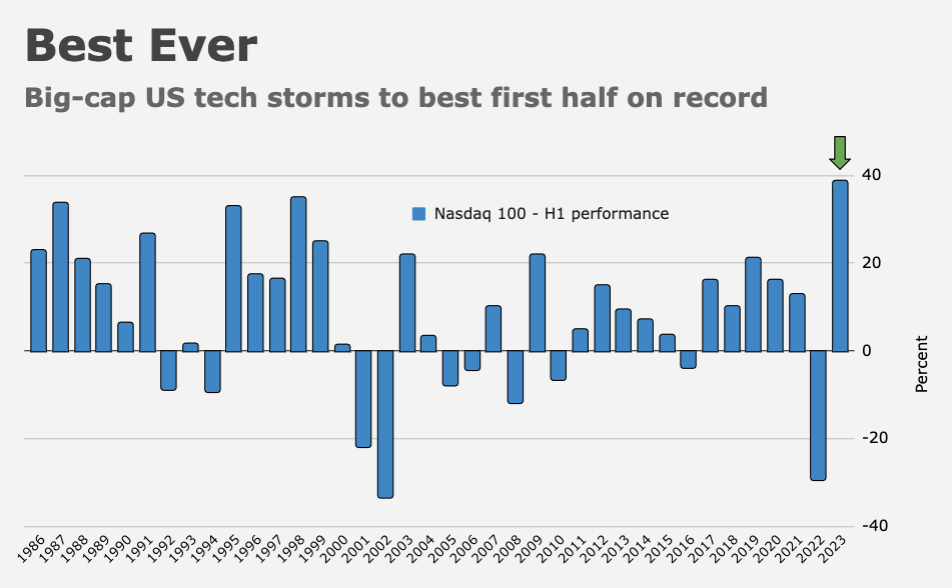

What accounts for that? Well, A.I. optimism for one thing. 2023’s H1 US equity rally was a re-rating story, and a tale of tech dominance. The Nasdaq 100 famously notched its best first half to a calendar year in history. Together, the so-called “Magnificent 7” re-rated by two turns in the past two and a half months alone. Ironically, Nvidia’s multiple actually plunged — the company’s guidance and expectations for surging A.I. spend doubled the denominator in NTM P/E equation.

At the index level, pretty much all of the S&P’s gains this year are attributable to multiple expansion. At 20x, the world’s benchmark risk asset par excellence is rich indeed. As Goldman’s David Kostin noted, US equities now trade in the 87%ile on a forward multiple basis. “During the last 40 years, the current P/E multiple has only been surpassed during the Tech Bubble (a peak of 25x) and COVID (a peak of 23x),” Kostin wrote, on the way to offering a variety of explanations for the apparent disconnect between multiples and real yields illustrated above.

Obviously, stocks can’t be explained entirely by reals. Profits matter, for example, and in equal measure. “Declining profitability helped explain some of the P/E compression in 2022 [but] in recent quarters, S&P 500 earnings appear to have bottomed, and we expect an acceleration to 5% EPS growth in 2024,” Kostin remarked.

In addition, the reason for rising reals matters. Policy-induced increases with no concurrent reset in growth expectations are challenging for stocks. By contrast, increases in real yields predicated on assumptions about better growth outcomes are easier to reconcile with equity rallies. As Kostin put it, “equity valuations are generally negatively correlated with the market’s pricing of Fed hikes and positively correlated with the pricing of growth.”

Lately, the US economy appears to have reaccelerated, and banks are beginning to question the notion that a recession is on the horizon. Goldman looked at weekly moves in reals and valuations back to 2021 and found that during weeks when reals rose and cyclicals outperformed (suggesting investors’ growth outlook had improved), multiples expanded slightly.

By contrast, when reals rose and cyclicals underperformed, multiples contracted. “Intuitively, multiples rose the most when growth expectations improved and yields declined,” Kostin observed.

That latter point is important, as it speaks to the power of falling reals in an environment where investors are generally constructive about the outlook for the economy. When growth prospects are improving (or steady) and reals are falling, risk assets have an unequivocal green light.

So, where to from here? Goldman’s baseline calls for a slight equity de-rating into year-end, but Kostin conceded two “upside risks,” one of which is a scenario in which the S&P 493 (so to speak) re-rates in a “catch up” move with the “Magnificent 7.”

It’s unlikely, Goldman suggested, that multiples for America’s mega-cap behemoths will compress materially if growth stays resilient and inflation continues to moderate. That makes a “catch down” scenario less likely. In a hypothetical situation where the rest of the market re-rates from 17x to 19x and the “Magnificent 7” multiple is unchanged, the index multiple would be 21x, implying SPX 4825, a new all-time high.

It’s also possible that rates fall given expectations for cooler core CPI prints (even if downward progress for headline price growth stalls or inflects as favorable base effects drop out and/or commodities rally). In a scenario where 10-year US reals fall 50bps to 1%, and assuming a constant yield gap, the S&P could re-rate to 21.6x, implying SPX 4975.

Do note: It wouldn’t be unprecedented for multiples to detach themselves from reals entirely. At the height of the dot-com bubble, for example, the S&P traded above 24x with US reals at 4.5%. Of course, that didn’t end well.

{kind=link}

Full employment, happy investors…. I like this view. Tomorrow is another day, and as we know, nothing happens till something happens.

Inflation was never gonna go away overnight. For markets and politics, inflation was hyper-relevant .

I hope there is a long run of a slow news days.

Your Keen eyes , Mr. H, will find something interesting to write about and be plagiarized.

I’ve seen a very similar chart showing how S&P 500 has detached from total liquidity, after tracking it very closely for some years.

Did anyone else think the end of grain and fertilizer shipments from Ukraine through the Black Sea would have rattled world markets much more than it did?