Lost in the euphoria around the slowdown in consumer price growth and apparently imminent producer price deflation in America was the downside of disinflation.

Well, it wasn’t completely lost. At least one reader joked about Pepsi rushing to get one more price hike in before the music stops. But for the most part, it was all smiles as both CPI and PPI figures for the world’s largest economy undershot expectations.

Once the sugar high wanes (if it wanes), market participants may remember that the so-called “price over volume” strategy corporates have pursued to boost bottom lines in the pandemic-war era doesn’t work so well when inflation starts to recede. Put differently, “excuseflation” needs an excuse.

If, instead of lamenting the highest inflation in 40 years, national headlines are touting a rapid decline in price growth, consumers won’t be as amenable to price hikes. That’s especially true given how weary some consumer demographics probably are after two years of opportunistic price increases.

This’ll come up on earnings calls this reporting season. Goldman discussed it at some length in a second half asset allocation update. “Weaker global PMIs in aggregate could start to weigh on earnings revisions, especially as inflation normalizes at the same time,” the bank’s Christian Mueller-Glissmann wrote.

Note from the figure on the left below that earnings revisions are moving in the opposite direction of PMIs now, and could well turn lower (i.e., stay negative) if the growth impulse wanes.

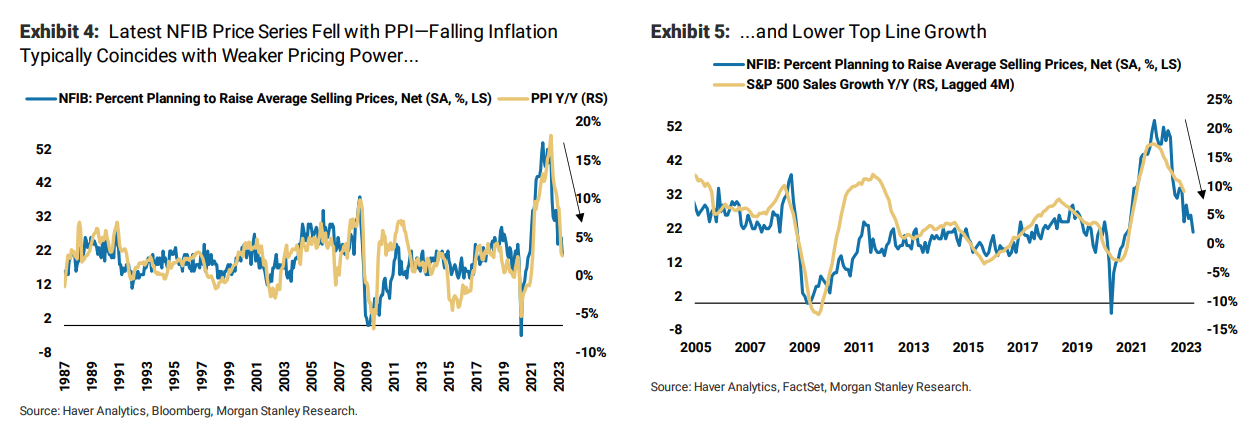

The figure on the right is self-explanatory, and I’d note that other visual representations of the same dynamic look even more poignant. For example, plotting NFIB price hike intentions with PPI is telling, and so is the same NFIB series plotted with S&P 500 YoY revenue growth (click here to pull up those charts).

Mueller-Glissmann elaborated. “While higher inflation has likely weighed on equity valuations, it also supported profit margins, especially for companies with pricing power,” he said, adding that although Goldman’s equities team does think the worst of the profit contraction is over in America, “continued declines in inflation, especially in PPI, could start to weigh more on margins” and in any case, “substantial near-term margin expansion is unlikely.”

That’s the downside of disinflation. Expect to hear more about it in the weeks and months ahead.

{kind=link}

Is there a segmentation of who was able to raise prices well above cost inflation? ie. what’s the profit margin picture once you look at sectors and/or size?

Thanks for a great bit of synthesis. It’s pretty clear that simply calling out/shaming companies will have a limited impact on their pricing.

What you point out is that perhaps old-fashioned market forces will discourage more rapacious price hikes, albeit at a lag.

Poster Child #1 PepsiCo did mange to raise prices 15% in the second quarter, following up on the twin 16% hikes in the previous two quarters. CFO Hugh Johnson said the latest price hikes were merely following commodity prices higher.

As per your thesis, how will he justify more eyeball-gouging if it became widely known that commodity prices are actually falling? He did note, however, that lower income shoppers have been looking for better deals (WSJ 07/14/2023)