Headline European inflation receded in June to the slowest 12-month pace since January of 2022, the month before Russian tanks rumbled across Ukraine’s borders.

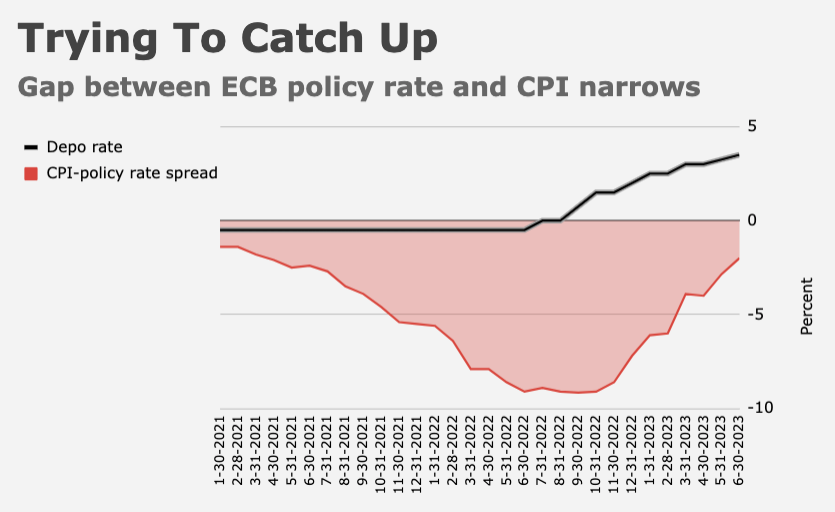

At 5.5%, price growth is now “just” two percentage points above the ECB’s policy rate following this month’s hike. The bank has all but pre-committed to another increase in July and may well keep raising rates in September. Next month marks the one-year anniversary of liftoff, which in the ECB’s case meant a climb out of negative territory.

Officials will take little, if any, comfort in the cooler headline reading. Core prices rose 5.4% YoY, slightly faster than the prior month’s annual pace and just short of record highs.

If you like, you can blame base effects and various “distortions” for the elevated core print, including the impact of Germany’s efforts last year to offset the shock from sharply rising energy costs. We’re now lapping comps from the €9 German train ticket months.

“This was mainly due to the effects on services inflation from German government support last year,” ING’s Bert Colijn said Friday. “Our own seasonal adjustment suggests that both eurozone goods and services inflation saw a modest decline in June, in line with the current disinflationary trend.”

Still, the optics are bad. Readily explainable or not, eurozone services sector inflation accelerated meaningfully this month, to 5.4%. The MoM increase was 0.6%, double the monthly rise on the headline and core gauges.

The bottom line for the ECB is the same: Inflation is now a services sector problem and it’s threatening to find its way into wage-setting, if it’s not already there.

Christine Lagarde this week said the bank doesn’t see a wage-price spiral “currently,” but conceded that “the longer inflation remains above target, the greater [the] risk become[s].”

Forgive me, but developed market central banks wouldn’t see a wage-price spiral if it was sitting at the table with them during policy meeting deliberations, and not because they’re blind. The problem is that they don’t want to see a wage-price spiral, so they pretend there’s no evidence of it. Which is fine… I guess. As long as core inflation does eventually moderate. Right now, the jury is still out.

Of course, this is a uniquely difficult task for the ECB, which is administering (or trying to administer) one monetary policy for disparate economies with no unified fiscal regime. It’s a miracle, frankly, that it works at all. The inflation numbers are starting to diverge materially, and one has to wonder how the ECB plans to deal with a situation where policy rates need to remain restrictive based on very high inflation in some locales, even as price growth recedes to target in others.

Food price inflation came down again in June, which was good news. In a testament to just how vexing this situation really is, the 11.7% YoY pace of price growth for food, alcohol and tobacco counted as the slowest since August.

{kind=link}