Was America’s regional banking crisis a tempest in a teapot? (And yes, the Jamie Dimon joke is intentional.)

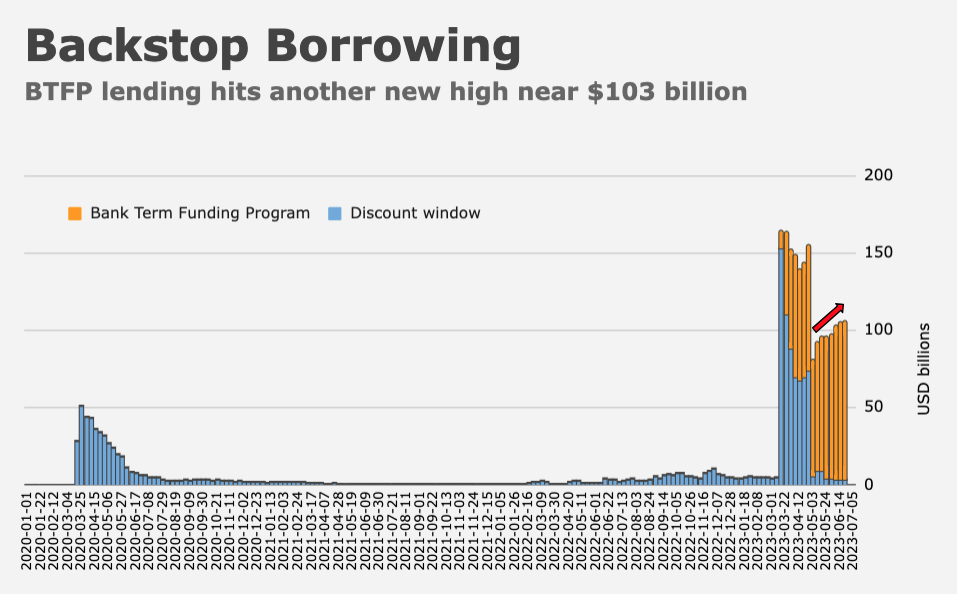

It depends on how you look at it. It’s certainly possible that lending standards could tighten further, tipping various dominoes in the process. CRE is the most obvious candidate. It’s also conceivable (indeed, it’s probable) that profitability will be constrained for small- and medium-sized lenders going forward. Usage of the Fed’s newly-created Bank Term Funding Program continues to hit new records week after week, a sign of lingering angst. And the allure of 5% yields on government money market funds is still problematic for any banks struggling to hang onto deposits.

In all of those respects (and I could name a few more), SVB’s collapse, and the bloodletting that ensued, left an indelible mark, and will forever live in some kind of infamy, at least through red annotations on various charts.

And yet, with sincere apologies to all parties impacted by the dramatics, and notwithstanding the fatal spillover to Credit Suisse, there’s a sense in which not a lot came out of March’s fireworks. Indeed, you could suggest that, unless and until something changes, SVB will be remembered as an event which ushered in a new equity rally by, among other things, facilitating various vol-dampening dynamics (including correlation-crushing dispersion) and reviving the perception of a policy put (there was, after all, a bailout, and a new Fed facility was created for the occasion).

“To the markets [the commencement of the US regional banks crisis] signaled the classic ‘Fed tightening cycle ends when they break something’ scenario, and elicited a de facto ‘resumption of Fed put’ shift in risk-seeking behavior and broad risk appetite,” Nomura’s Charlie McElligott wrote, in a Wednesday note, calling the risk-adjusted return of a hypothetical systematic short volatility strategy the “ultimate exemplification” of that dynamic.

A strategy which sold SPX daily 25 Delta puts would’ve produced a 10-day trailing Sharpe ratio “of an absurd +64 in the one-month period after the peak of the banks crisis [from] mid-March through mid-April,” Charlie wrote. As the figure shows, the 10-day trailing Sharpe was still 42 as recently as a couple of weeks ago.

“There currently is just no ability for the US equities market to ‘crash down,'” he went on.

There is, however, the ability for US equities to crash up, and that’s created “two totally different games” for selling calls versus selling puts for income.

“We are almost exclusively ‘crashing-up,’ yet perversely unable to sell-off,” McElligott said, updating and reiterating key points.

Through Tuesday, the hypothetical ATM daily put-seller was outperforming the call-seller by almost 13 percentage points. And those theoretical returns weren’t limited to the “super-charged dailies” or even to equity index products at all, Charlie showed, illustrating PNL for systematic vol-selling across all manner of exchange-traded products, including ETFs for credit, Treasurys and individual sectors of the US equity market.

He offered a word (or two) of caution, though: “Of course, short vol strats post exceptionally ridiculous Sharpes until they inevitably go ‘extinct’ on a vol event — the classic Taleb ‘life of a Thanksgiving turkey.'”

{kind=link}

Interesting, thanks. A nice quiet window-dressing rally into quarter end is just what our algorithmic friends will be happy to feast on.

I should ask Gary Numan to rewrite “Are Friends Electric?” to reflect the new backdrop!