Much has been made of the recent collapse in market breadth across US equities, and particularly of mega-cap tech outperformance.

Implicit (sometimes it’s explicit) is the notion that a narrow rally is an unsustainable rally — that an index relying on a tiny handful of names to rise is an index that’s poised to fall.

I wouldn’t necessarily dispute any of that, but as BofA’s Michael Hartnett put it last month, employing an imagined, but wholly plausible, quote that could’ve emanated from a trader or fund manager, “Under the surface it’s starting to get scary, but we all know what the Big Tech horsemen can do to P&L before we blow up.”

In a new note, Goldman’s David Kostin ran through a hodgepodge of numbers and statistics documenting mega-cap tech’s fundamentals, valuation premium and the above-mentioned performance disparity versus the rest of the market. Several things stand out. Most obviously, there’s no performance in 2023 without Apple, Microsoft, Alphabet, Amazon and Meta.

“The 5” are responsible for the entirety of this year’s gains for US equities, and as JonesTrading’s Mike O’Rourke noted recently, when you include Tesla and Nvidia, “The 7” are responsible for 110% of 2023’s gains.

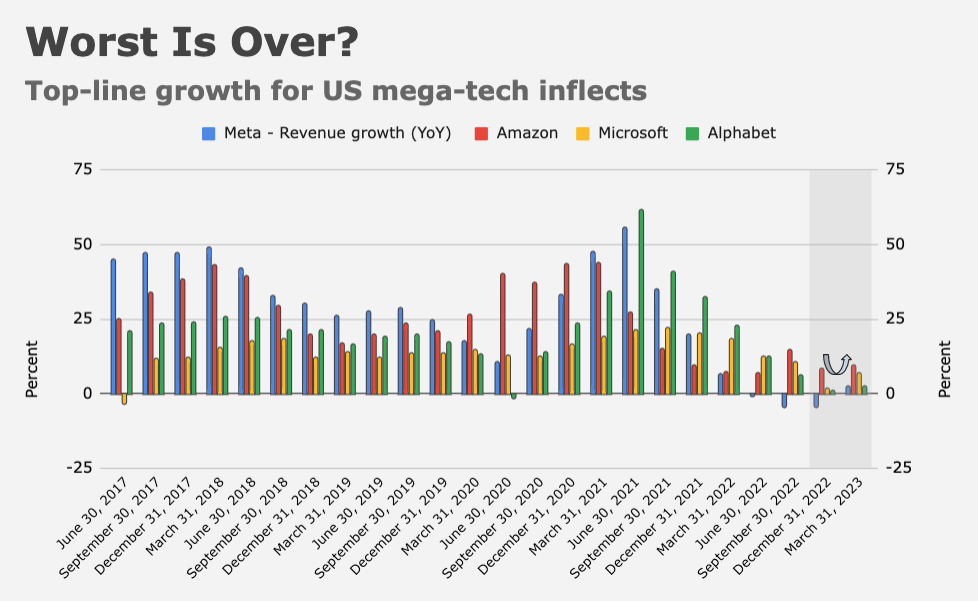

Quarterly results for the big names were broadly better than expected, and as the table shows, the outlook for top-line growth and profitability remains far superior to the rest of the market. In 2021 and 2022, top-line growth flatlined for the titans, but it inflected last quarter, except for Apple anyway.

There’s still an argument to be made that these stocks are more cyclical than most investors are willing to admit, but they retain a safe haven appeal, something Goldman’s Kostin underscored.

“The outperformance of mega-cap tech amid renewed recession fears has echoed conversations with investors who argued that the stocks should be viewed as economically defensive,” he wrote, noting that “the median mega-cap tech stock has a stronger balance sheet than the median S&P 500 stock (Altman Z-score of 7.7 vs 3.4).”

From a profitability standpoint, it really isn’t a contest. Over the last half decade, margins were nearly 1,000bps wider for mega-cap tech compared to the index on average, and although the near 600bps of margin contraction seen in 2022 was a wakeup call of sorts, the gap is expected to widen back out beyond 800bps going forward.

Bears will contend that tech firms aren’t especially adept at cost-cutting and that decelerating revenue growth in cloud and a still-challenging environment for ad spending may forestall a rebound. But… well, I’d just caution against assuming these behemoths won’t figure out a way to grow revenue and reclaim lost margin.

The best bear case for the mega-caps is, somewhat ironically, a soft landing where rates stay elevated, the Fed disappoints market expectations for cuts and true cyclicals are able to outperform. The current “muddle through” scenario where growth is below-trend and Fed cut pricing lingers alongside ongoing macro angst favors the giants.

In a real recession, mega-cap tech would likely succumb just like everything else, not just from fundamental pressure, but also from investors raising cash. “During risk-off events, funds often sell more popular and more liquid stocks first [and] all five mega-cap tech stocks rank in the top 10 of our Hedge Fund VIP basket,” Kostin went on to say, adding that “the popularity of mega-cap tech among hedge funds leaves it vulnerable in a major risk-off event.”

BofA’s Hartnett made the same point. In a “proper unwind of risk assets,” investors are forced to “sell what they love,” he remarked.

{kind=link}

For MSFT GOOG AMZN META estimates and expectations have come down to beatable, margins have largely bottomed, significant cost levers remain to be pulled, and revisions are as likely to be (slightly) positive as negative. For AAPL, I think margins and estimates still have room to decline, but perhaps not enough to alarm investors (Jun qtr estimates coming down didn’t seem to matter), cash flow is prodigious, and cost levers have yet to be seriously pulled. Current growth is scarce but that’s known, and the hope of future growth remains. Valuations look reasonably attractive for two, excessive for two (but negative catalysts seem scarce), who the heck knows for the fifth, and as long as the Fed stays on pause and revisions stay benign, the risk to their multiples seems modest. These are the best companies in the world, by many measures. In a recession, they certainly have downside but it’s not evident that it’s more than the S&P 500 overall, both because of their market position and because of their weight in the index. I don’t loooove these names here, but don’t hate them as I did in mid 2021. I started accumulating these in mid 2022 – incrementally in most cases, except for more decisive buying of META (good decision) and no buying of AAPL (bad decision). Funding from other names – not seeing much reason to increase overall equity exposure.