Over the past six months, nonfarm payroll growth in the US overshot the typical pre-COVID pace by an average of 150,000. Discretionary consumer services hiring accounted for half of that overshoot.

That’s a significant data point on its own, and I could editorialize around it all day from various vantage points. It speaks, for example, directly to some of the dynamics discussed here on Tuesday in “Layoffs Won’t Solve This Inflation Problem.”

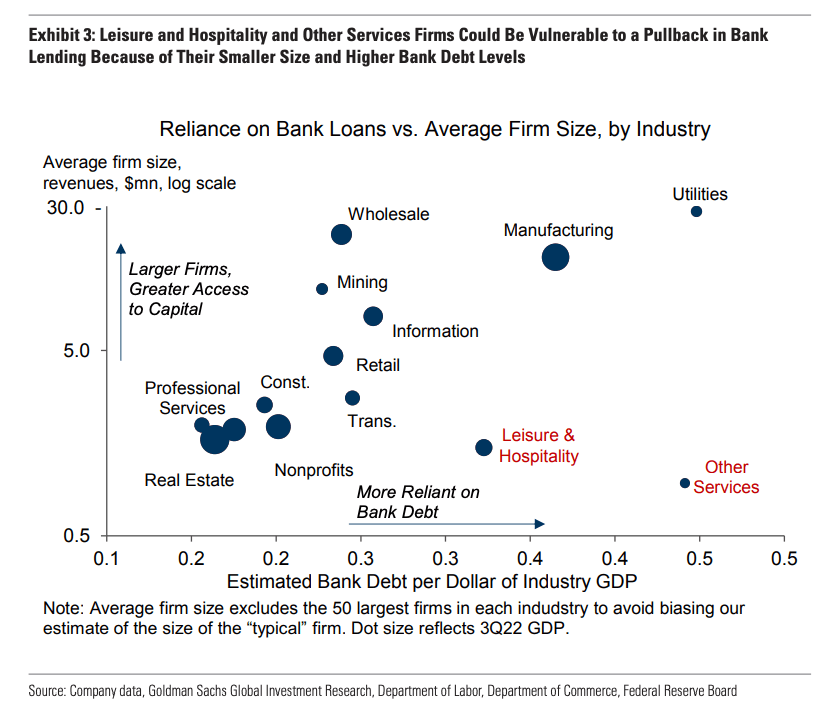

But it’s particularly notable in the context of recent regional bank stress.

Your local dive bar can’t generally call up Wall Street for a junk bond offering, nor can the hair salon operating out of the local strip mall (which may itself be in dire financial straits soon) avail itself of a secondary to raise capital in a pinch. It’s bank loans, or it’s nothing.

The scatterplot below from Goldman shows that discretionary consumer services firms are in a doubly perilous position. They’re generally small, which means they can’t access capital markets easily (or in any case at affordable rates) and they’re heavy reliant on banks. Those two things (being small and relying on bank loans) go hand in hand.

Self-evidently, small, consumer services businesses aren’t critical to the capex outlook — they only comprise 3% of US investment spending, according to Goldman’s estimates. But they sure do hire a lot of people, and, as noted above, they’re responsible for a disproportionate share of “excess” hiring in the pandemic era.

“To the extent tighter bank credit affects discretionary consumer services industries, its macroeconomic effects could be more visible in employment than capex data,” analysts led by Jan Hatzius said, in a note dated March 28. “Looking ahead, we expect slowing job growth in this sector as diminished loan availability dissuades restaurant operators and other smaller businesses from hiring new workers and opening new establishments.”

If the services sector is the epicenter of the inflation impulse in the world’s largest economy, and if that impulse is tied to an acute mismatch between demand for labor in discretionary consumer services industries and the supply of it, you could argue that tighter bank credit is exactly what the doctor ordered.

Add real estate development and construction. Smaller banks are particularly active in that area, as well as related CRE. There will be a lag to employment, as financed projects launch and complete.