On Friday morning, while documenting what was shaping up to be a rough session for Deutsche Bank, I wrote that, “sharp moves in the shares and CDS precipitated the usual social media cacophony and accompanying five-alarm coverage blaze at mainstream financial news outlets.”

Of course, it’s possible the causality runs the other way — that is, it’s possible the never-ending mainstream news coverage and accompanying social media frenzy are undermining confidence, and that’s feeding market moves which then feed on themselves, and then back into media stories, in a self-fulfilling prophecy.

Later, some suggested hedge funds were targeting Deutsche Bank, which is probably true, but it felt a bit like reporters were determined to find a neat explanation for chaotic trading. That’s a difficult task even in the best of circumstances. These aren’t the best of circumstances.

Whatever the case, confidence is fragile, and it’s now very difficult to disentangle various chicken-egg dilemmas like those inherent in the media-market nexus dynamics briefly outlined above. The Stoxx 600 Banks index has spent this month wiping out gains for the year.

The situation is obviously more acute in US bank stocks and particularly in shares of some regional banks.

I realize that every few years, a new batch of early-twentysomethings inadvertently stumbles into the financial agitprop echo chamber and discovers various standing doomsday narratives, so I want to emphasize: The dark fairy tale that says Deutsche Bank’s derivatives will one day blow up the world is the furthest thing from new. That’s one of the longest-running financial apocalypse memes of them all.

I’ve known former risk managers at Deutsche Bank, one of whom was an SEC whistleblower — that is to say, not the sort of person inclined to harbor a favorable view of the bank. Exactly none of them worried that the apocalypse for humanity (whenever it comes, and whatever brings it about) will have anything to do with Deutsche Bank, or at least not to do with Deutsche Bank’s balance sheet. (That latter bit is supposed to be funny.)

I think it’s imperative that we acknowledge the risk associated with deteriorating confidence and how “contagion” needn’t have anything to do with fundamentals. As Jane Fraser told David Rubenstein this week of SVB’s collapse, “There were a couple of tweets and then this thing went down much faster than has happened in history.” Fraser was prompted by Rubenstein, who wondered whether the fact that people can move their money out of a bank with their phones has increased the risk of bank runs. Fraser called mobile and online banking “A complete game changer.”

When you consider that in conjunction with hair-on-fire media coverage, you’re led to the inescapable conclusion that the risk of major institutions running into real trouble as a result of unfounded rumors and errant headlines is higher than it should be.

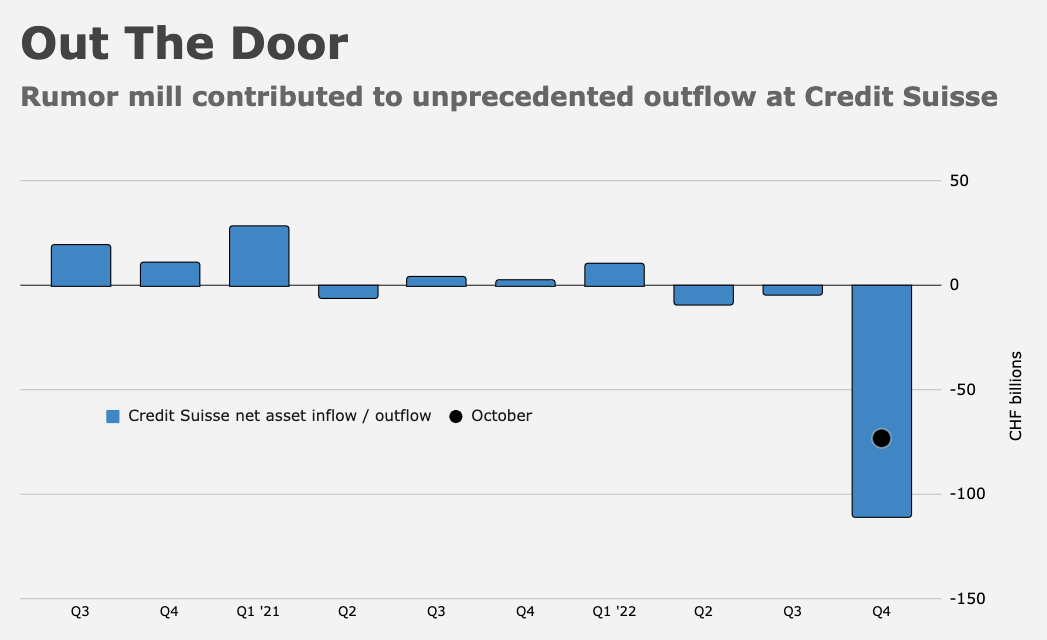

To be clear: It wasn’t surprising that Credit Suisse ultimately ended up merging with UBS. The bank was, after all, reeling from years of mini-crises, and Ulrich Koerner’s turnaround plan was as complex as the bank’s problems were myriad. The Swiss wanted a domestic solution. So, here we are. What was surprising, though, was the rapidity with which the last chapter of the bank’s near 167-year history was written. Two points on that:

- The bank suffered an estimated $80 billion in outflows in October as a result of wholly specious social media speculation. Those outflows eroded confidence, helping set the stage for last week’s spiral into oblivion.

- Last week’s spiral was precipitated, at least in part, by an on-air exchange between two people (a television anchor and the chief of Saudi National Bank, Credit Suisse’s largest shareholder) whose first language isn’t English. Both are fluent, an extremely so. But when you’re dealing with investor psychology at a delicate juncture, one “wrong” word is all it takes to tip the dominos.

This goes without saying (I hope), but that second point isn’t meant to be pejorative. I don’t even like English, and especially not the variant I speak. (As a quick aside, a senior editor for a mainstream financial media outlet once lampooned my speaking voice in a prominent article, which I really didn’t appreciate, and still don’t. But I take solace in knowing that if it were a writing contest… well, she wouldn’t measure up.)

My point about Credit Suisse is simple: You could very easily argue that the bank would still be independent today were it not for two people speaking to each other for the cameras in a second language about the bank’s liquidity, while markets were open, and at a time when sentiment around bank shares was dire. During that exchange, nobody should’ve used the word “assistance” (or any variant of it). If you doubt my assessment, just ask Ammar Al Khudairy, one of the participants in that exchange. He later told CNBC that he “didn’t even know where” the word “assistance” came from.

The bottom line is that between social media, modern banking, a sensationalist, 24-7 news industry and the wholly pernicious presence of finance-focused tabloid websites, the system is more vulnerable to overnight panics that it was in the past.

As one analyst put it, “The risk is if there is a knock-on impact from various media headlines on depositors psychologically, regardless of whether the initial reasoning behind this was correct or not.” That quote was featured Friday in a mainstream news article about bank turmoil. The irony was apparently lost on that outlet.

{kind=link}

it’s not only psychology. here in Germany the banks do not pay any interest on the money you hold with them. on the contrary, many of them actually charge you for holding the account. hence, there’s simply no reason to hold any substantial amount in the bank

Cue up the “pouring gasoline on a fire ” analogy. Perhaps this means that that panic will subside just as fast. Jim Bullard apparently thinks this is the likely outcome.

Beyond the press desperately trying to “explain” the turmoil and gain notoriety with their doomsday calls, there is some serious money betting on that things unwind further:

https://finance.yahoo.com/news/short-sellers-step-bets-against-145752244.html

I’d argue the trade you’re talking about is completely rational and fundamentals-based. I don’t see anything “wrong” with that at all. That trade has multiple fundamental pillars. Not saying I would or wouldn’t recommend it, just that I don’t think “mass bank runs” is going to decide whether it works or not. Regional bank stress certainly helps make the case and may well be the factor that makes it go from “good idea” to “slam dunk,” but I wouldn’t describe it as some opportunistic “jump on the bank stress” bandwagon trade. I just think it’s a thesis that makes sense to a lot of people

Agreed, sir.

Among the languages I have learned, English is better sounding than most, though there are too many “r”s and “t”s. The English do not pronounce the “r”s, and swallow some of the “t”s. I think it sounds better than the US version. On the other hand, my very own mother tounge just sounds much more horrible to me after 50+ years, with too many “sch” “ch” “t” sounds and words that stop suddenly with “k”. German is also not very nice to the ear. I like Spanish (Castillian). Just enough “h” (as in “high” to give it some ruggedness, and in Latam they don’t even have that.

Well said Mr H. Cable News/Financial Media sells hype and humans crave an emotional charge. The political views on cable news are supercharged with indignant emotions also regardless of where they are on the political spectrum.

The playbook for speculators appears to be short the stock of a marquis SIFI bank that has a chequered reputation, and then bid up their CDS in a fairly illiquid CDS market on a Friday, when investors are more likely to sell going into the weekend and ask questions later. The financial media builds the negative momentum.

Yes. The issue is that the financial media jumps on these stories immediately, to “capture the move,” as it were, and then maybe/sometimes gets around to explaining the “why” later, assuming they can figure it out.

I added three short sentences to this article to account for subsequent reporting that suggested hedge funds were targeting DB, but the thing is, the media didn’t get around to reporting that until after European markets were closed. At that point, it was too late.

I’m not “implicating” the media. Obviously, you have to report the news if you’re… well, if you’re the news. That’s kinda the whole thing. If you’re a news outlet and you don’t report news, then what are you doing all day, right?

My point is just that in my opinion, there needs to be a little bit more in the way of rigor to be sure you’re not, as a media outlet, creating the news — to be sure you’re not looking at yourself in the mirror, as it were.

Your point about dysfunctional mainstram media is well taken and my understanding is The Donald leverages heavily the media’s “dog sees squirrel” inability to think before rebroadcasting (which is not the definition of reporting/journalism).

Mainstream media is in the business of selling soap powder by capturing eyeballs. One captures eyeballs more readily by lighting hair on fire than by trying to split it, so from my perspective what mainstream media is doing is totally functional given their business model.

What would be dysfunction is if Walt started lighting HIS on fire because he is in the business of selling thoughtful balanced analysis. If hair is involved, its about parting it, not splitting it. That’s why we pay him a few bucks a month. Just like our barbers.

What is also dysfunctional, in my opinion, is the vast number of people who think they are getting a barber, when what they are getting is an endless supply of gas and a match.

Very human though…

H, if you’re ever bored and want to get a comedian’s take on this subject, check out The Day Today, and specifically an episode called Magnifievent where the presenter incites a war between HK and Australia. British comedy at its best.

https://www.federalreserve.gov/releases/h8/current/

Fed’s def’n of “large” (top 25 by domestic assets) reaches all the way down to regionals with with $70BN ish assets. So it is the SIFIs plus the larger regionals.

Half of net deposit outflow in two weeks of Mar 8 and Mar 15 was foreign-related (CS?), and all of net outflow in one week of Mar 15 was. In the two weeks, large banks took in net $65BN, +0.6% of deposit base, probably almost all went to the majors. Small lost net -$113BN, which is only 2% of deposit base. Unless outflow really accelerated last week, I don’t really see a general bank run here. Too copacetic? Regionals were almost all up today, ahead of the weekend. Still some names down -30% or more L1M.

I remember in 2007/8 thinking that a few chancers taking out liar loans to build gaudy second homes in Florida was not a plausible doomsday scenario. In the IB where I worked, that was the consensus view right up until we were all working weekends trying to save our skins. The stakes are much higher now but the same complacency is there for all too see. This time the prevailing view is that ‘banks are much better capitalised’. QT is a far, far bigger catalyst than sub-prime ever was. I’m jumping on the doomsday train, at least in my head.

I went through similar at a hedge fund. I also remember the summer of ltc sitting on a bond desk and listening to the overhead when markets shut down, but things worked out quickly. It can go either way, but it is foolish to think it could not be a big deal.

Wasn’t it Deutsche Bank that lent Donald Trump something like $18 billion? (Asking for a friend.)