Much of the debate around how the Fed should approach the tradeoff between the inflation fight and stress in the US banking sector seems to center on the merits of being proactive versus reactive.

It looks as though the swap line announcement+ was an example of the Fed preempting dollar-funding stress rather than addressing any that already existed, and you could argue that’s the best approach when it comes to these kinds of issues. It’s better to check and reinforce the scaffolding today than it is to repair it tomorrow after an accident.

The March FOMC would’ve been easier for officials if it weren’t an SEP meeting. The dot plot complicated things. The projections are always of questionable utility anyway, and in my estimation the press conferences are often counterproductive too. If the Fed hadn’t burdened itself with the SEP and the Q&A, the Committee could’ve simply keep rates unchanged with a simple statement acknowledging two-way risks, confident in the (I think reasonable) notion that victory (or defeat) in the inflation fight didn’t depend on this month’s 25bps hike.

As discussed here on Tuesday afternoon, the current state of affairs is characterized by an awkward juxtaposition between, on one hand, buoyant equities at the cap-weighted index level and the absence of anything like panic across a number of key stress metrics, and, on the other, record rates volatility, heavy discount window usage and a flood of FHLB issuance.

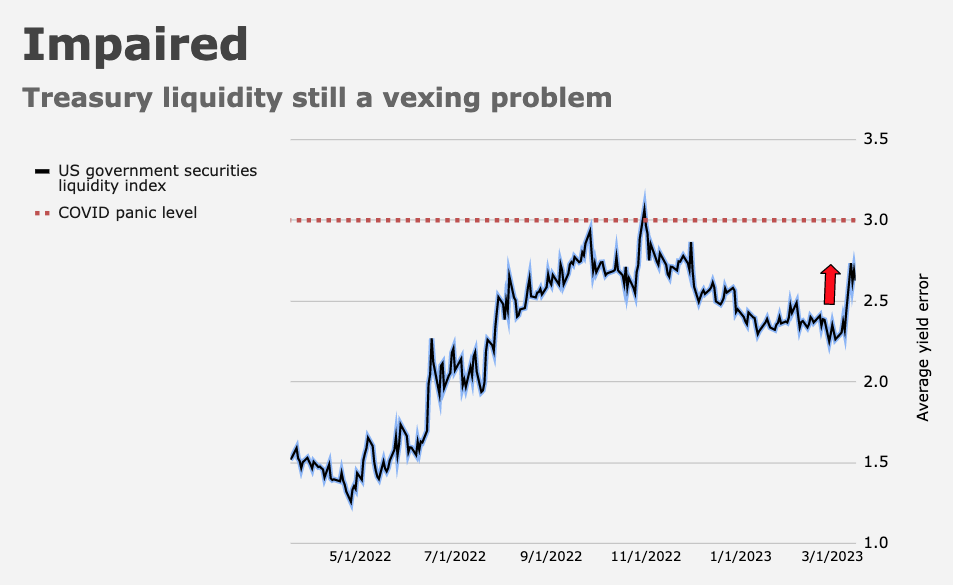

To be sure, market depth in Treasurys (i.e., liquidity) has deteriorated, but it’s an open question whether the situation warrants intervention. Bloomberg’s US government securities liquidity index is near COVID panic levels, but that’s been the case for months. Indeed, it was regularly higher (i.e., worse conditions) in September, October and November.

Still, volatility is off the charts in rates and a simple visual depicting the range for two-year US yields in March underscores the unprecedented nature of this month’s fireworks.

If you ask JPMorgan’s Jay Barry, though, the situation isn’t anomalously acute, or at least not from a liquidity perspective in the context of an already impaired market. “The footprint of each trade, as measured by price impact, has been elevated for the past year but has not risen appreciably in recent weeks and remains below crisis levels,” he said, adding that although dislocations are more prevalent, they’re not indicative of “distress.”

So, again, we’re effectively asking whether the Fed should be proactive in its approach to managing risk. Treasury liquidity and rates vol aren’t the only (or even the primary) concern in the near-term — banking sector stress is. I realize it can be challenging for laypeople to keep apprised of all the relevant developments, so below are a few bullet points from Goldman which summarize the various ways we have of monitoring and assessing stress on banks and deposit bases.

Via Goldman:

- Bank deposit rates have risen by up to 10bps at online banks and by a smaller amount at credit unions, but have not yet increased at the larger regional banks.

- Retail and institutional money market funds (Exhibit 2, left) — a likely destination for bank deposit outflows — saw large, accelerating inflows last week, suggesting some migration away from deposits as well as a broader flight to quality. Total money market fund inflows reached $121 billion last week, versus a weekly average of $23 billion year-to-date.

- Daily bond issuance by the Federal Home Loan Banks (FHLBs) — an indirect measure of the degree to which banks are turning to the wholesale funding markets to meet liquidity needs — rose to $300 billion last week (Exhibit 2, right). Some of this is likely defensive behavior by banks looking to shore up cash in anticipation of possible future deposit outflows, and some likely reflects a need to meet realized outflows.

- Balances in the Fed’s Reverse Repo Facility (RRP) fell by $125 billion last week, versus an average $19 billion decline in securities from QT so far this year. This suggests that banks’ funding needs were large enough to drive FHLB issuance rates above what could be earned at the RRP. Money market fund investors may have rotated assets out of the RRP and into FHLB debt, which means that this liquidity entered the banking system.

- The geographic breakdown of [borrowing at the discount window and the BTFP] reflects the headquarters of the banks currently seeing the most stress: 18% occurred at the New York Fed and 78% at the San Francisco Fed, much of which was done by First Republic, which has disclosed that it borrowed between $20 billion to $109 billion from the Fed from March 10-15.

- Borrowing costs in US money markets have risen, but the system’s overall functioning remains smooth. In the overnight repo market, the costliest transactions continue to occur at a normal spread to the fed funds rate, despite rising by 8bps last week. (Exhibit 4, left). More stress has been apparent in the commercial paper market (Exhibit 4, right). Financial companies have largely stepped back from issuing commercial paper, with only one new issue over the past 10 days. However, we would view this mainly as a sign that alternative funding sources for banks are attractive options rather than as a sign that money markets have broken.

One more time: It’s the juxtaposition between the readily apparent demand / need for liquidity and little in the way of stress elsewhere that sticks out.

The problem is the confidence element. Banks are everywhere and always a confidence game. Once confidence evaporates, the situation can (and usually does) spiral rapidly.

It’s now obvious (to this observer, anyway) that some kind of enhanced deposit insurance is a foregone conclusion+, and in the very near-term, it’s clear Treasury and the FDIC would likely view any bank failure as a “systemic risk” given shaky confidence and the high potential for contagion.

But it’s important to remember that the whole system is built on confidence. In the final analysis, it rests on a pledge: The “full faith and credit” promise. “Faith” and “credit” are confidence-based concepts. (You don’t have “faith” in God because you’ve seen him or her. Credit isn’t extended based on anything gleaned from crystal balls or tasseography.)

The argument for a Fed that acts preemptively to forestall additional banking stress is simple: The situation may be “contained” currently, but at the end of the day, there’s nothing tangible behind any of this. The closest thing to a “foundation” it has is the lack of alternatives to the dollar which, ultimately, is itself just “a project,” as Zoltan Pozsar put it last year. “Projects” fail all the time.

Policymakers should be cognizant of all that, and perhaps even hypersensitive to it right now, considering that the debt ceiling stalemate poses a direct threat to the underlying “full faith and credit” pledge.

If a technical US default this year were to collide with renewed stress in the US banking sector, that’d be a crisis of historic proportions, and of all the adjectives bandied about to describe it, “contained” wouldn’t be in the mix.

{kind=link}

Life is a confidence game. From determinism to meritocracy to free will to who will get the investment, job or be entrusted with capital. It’s why sociopaths excel they see it all as a game to be crafted in their favor.

Hello, Walt. Much appreciate your perspective of the current circumstances faced by the Fed. Your finger on the pulse view is right-on in my opinion. Thanks!

I’d like to see Powell express an assessment of the veracity of steps taken so far. Bank runs evidence the effects of rate increases already in the system. Because they were quick, diligent, substantial, and hard-hitting, I believe the current state merits a pause to allow those rate increases to wash through the system. The system needs to stabilize. Words about the hard work already done and impacts yet to be seen can be useful.

I reckon your view is realistic. But the chairman is dealing the cards.

The “backstop” is just getting started. There is an article in the Real Estate section of the WSJ today discussing the fact that smaller banks own about $2.3T of commercial real estate debt (estimated to be 80% of total commercial real estate debt) with about $270B set to expire in 2023. If borrowers can not repay at face, this is yet another massive, “too big to fail” problem that will likely result in bank failures unless the government backs these loans.

The only other option is continuation of “extend and pretend” ( extend the repayment date and pretend the loan value is still equal to the face value). However, higher interest rates might make this a non-starter for borrowers.

Japan, here we come!

I think CRE is such a diverse range of property types that the impact on regionals will be equally diverse. For those unfortunate enough to be concentrated in, say, San Francisco office, I don’t know how the US govt can backstop those CRE loans. The Fed can’t buy or lend against those loans, and certainly not when they become NPL.

https://wallstreetonparade.com/wp-content/uploads/2023/03/Loan-Advances-Outstanding-at-Federal-Home-Loan-Bank-of-San-Francisco-December-31-2022.jpg

I wonder if CitiBank has a lot of this commercial exposure

Hope and Denial.

The ancient Greeks thought that Hope got snuck into Pandora’s box, but Denial is the only way that hope is viable.

I sold my banks and Reits last year.

Pride goeth before a fall….