Let the crocodile tears flow freely.

The macro regime has shifted in favor of everyday people, to the detriment of Wall Street.

That was one (admittedly sensationalized) takeaway from David Einhorn, who spoke to CNBC on Wednesday.

“I think we should be bearish on stocks and bullish on inflation,” he said. “We’re in a policy now which is probably pretty good for Main Street, but it’s going to be increasingly difficult for financial assets.”

He elaborated: “The Fed does want stock prices lower. They’ve made that clear.”

Not that anyone needs a reminder, but stocks are disproportionately concentrated in the hands of the rich. As a percentage of the total, lower-income households and the poor own basically no stocks (refer to the green area in the visual below, assuming you can see it).

From 1989 through 2022, only the Top 1% has seen its share of the equity market grow. The 10pp share gain for America’s richest has come at the expense of everyone else, including those in the 90th-99th%iles.

One of the key points from February’s monthly letter (incidentally, March’s letter is in the works, and will likely be published on the 11th) was that the period economists typically associate with low and stable inflation outcomes was cruel to Main Street.

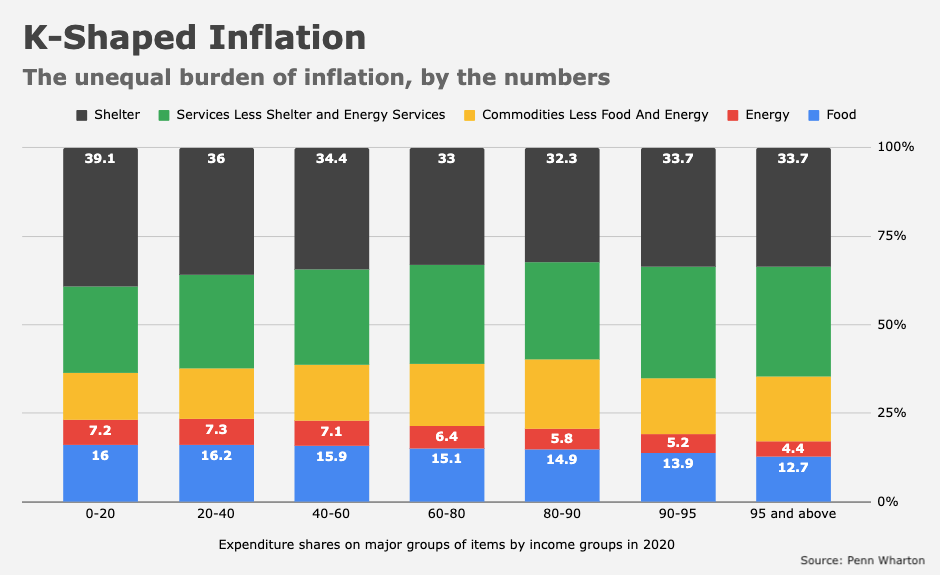

While it’s certainly true that everyday people suffer the most when inflation spirals (the so-called “K-shaped inflation” phenomenon illustrated here), some of the structural enablers which made The Great Moderation possible were responsible for hollowing out America’s industrial base, which in turn had dire societal consequences for the middle class, and served to worsen the trends documented by Robert Putnam in Bowling Alone and, two decades later, by Anne Case and Angus Deaton in Deaths of Despair.

That’s not to say inflation is good for Main Street. Or maybe it is. A little bit of it, anyway, at least to the extent it’s part and parcel of a macro conjuncture that includes more bargaining power for labor (as an economic actor, even if actual union membership never recovers its past glory) and better nominal growth outcomes. Recall the visual below from BofA.

I’ll repeat (verbatim) a few remarks from an article published here last week. Our deep-seated inclination to sing the praises of the post-80s/pre-2020s decades is in part attributable to the fact that the investor class was spared the domestic ills of globalization in developed economies, and benefited enormously from the rise of shareholder capitalism.

In a world defined by the juxtaposition between i) subdued growth rates on Main Street in developed markets and ii) elevated returns on capital from offshoring, buybacks and deregulation, the Piketty equation was skewed towards the perpetuation of inequality. Now, that’s changing. The majority is tired of it. Exhausted, in fact. 2020 was the tipping point.

American society is famously defined by dynamics which, when taken together, amount to “socialism for the rich.” If that stops for a while (or forever), the country will be a better place for it. If that means you and I have to put in a little more effort than we’re accustomed to in pursuit of double-digit returns on our portfolios, we’ll live. Who knows, we might even come away smarter.

{kind=link}