Americans were the proud owners of a record 564 million credit card accounts at the end of last year, according to the latest household debt report from the New York Fed, released on Thursday.

That was nine million more than the previous quarter, and up 6% from Q4 of 2021.

For reference, Americans had just 378 million accounts in Q3 of 2010, when the post-financial crisis de-leveraging troughed. Taken at face value, even that figure represented more than one credit card account for every man, woman and child in the country.

As of last quarter, there were more than two credit card accounts for every adult in the nation which, honestly, sounds about right, depending on your definition of “right.”

Macro watchers (which is everyone these days) are keen to parse revolving credit data for evidence of consumer retrenchment — or evidence of the opposite.

Although the pace of revolving credit growth receded in December+ according to separate Fed data, the NY Fed figures released Thursday showed a $61 billion increase in card balances for the fourth quarter.

That was the largest jump in history as far as I can tell. On a YoY basis, the percentage increase edged up to 15.2%, a new record.

Q4’s surge pushed America’s total balance to $986 billion, a milestone of the dubious variety. Despite more or less uninterrupted quarterly increases beginning with the onset of inflation early in 2021, the nation’s total credit card debt burden still stood below Q4 2019’s record as of September 2022. By the end of the year, though, the mountainous pile had easily surpassed the pre-pandemic peak.

It’s worth taking a step back to consider the juxtaposition with the rates backdrop. According to Bankrate, average credit card interest rates are now near 20%. So, Americans have nearly $1 trillion in variable rate debt to service, and rates are, on average, 1,991bps.

Do note as well that as of March 2021, the month before CPI began to accelerate in earnest, card balances were $770 billion, more than $200 billion below the current level.

The chart above is presented “as is,” so to speak. I make no claims to statistical rigor, let alone profundity. It just is what it is: The difference between the prevailing YoY growth rate in card balances as reported by the New York Fed and the YoY rate of CPI inflation measured on a quarterly average basis.

Although consumer spending decelerated in the final months of 2022, retail sales data released this week showed nominal spending in January was robust indeed.

According to the New York Fed report, Americans had $3.41 trillion in additional spending power on existing credit cards at the end of last year. I suppose those limits could always be lowered, depending on the circumstances.

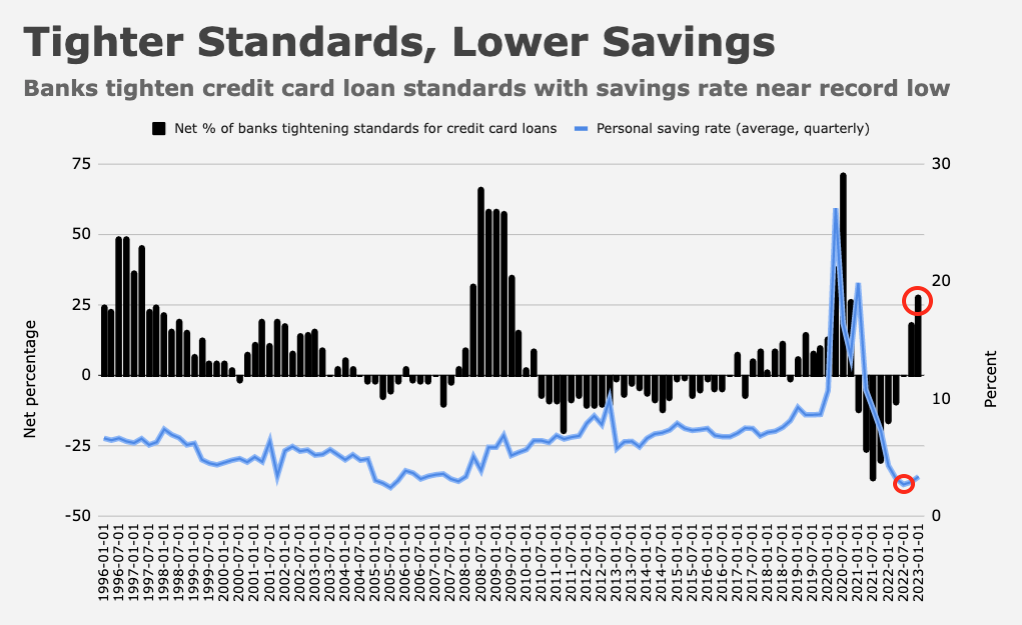

The most recent installment of the Fed’s Senior Loan Officer survey showed banks are aggressively tightening lending standards for cards. Nevertheless, aggregate limits were increased by $88 billion during the fourth quarter.

{kind=link}

The well seems to be running dry.

Until folks get nervous about their employment, I would not expect to see credit outstanding on cards to decline. Inflation alone would drive up nominal balances. And some are probably living off their credit lines.

I’d like to know how much of that nearly 1 trillion gets paid in full by credit card holders every month. These are people who have the money, but are using their CC as opposed to cash/debit cards because of points, miles, reporting, etc.

That’s the big question. I always pay my credit card in full on the payment day due. I even have one card with a 10K balance at 0% interest, no fees, good for 12 months. That is arbitrage money currently in T-Bills.

Plus whatever Americans have in home equity line balances, also variable rate although still single-digit.

Is there any data on how much of the credit card balance is paid off each month, rather than rolled over as interest-incurring debt?

On the positive side, high rates should suppress the BNPL model.

“So even as credit card balances outstanding have returned to pre-pandemic levels, as a reflection of spending, the number of accounts that carry interest-bearing balances has fallen by 10%, according to American Bankers Association data.”

https://wolfstreet.com/2023/02/16/where-households-ended-up-with-their-credit-in-q4-credit-card-balances-credit-limits-available-credit-delinquencies-collections/

Thank you for the link. Some interesting data in there.

The last data I saw was that many more folks pay in full every month than issuers would like. So, I just looked and data I found said 42% of CC users pay CC balances off every month. BTW Wisdom Tree has much data on CC behavior. Other data I saw said debit/cash card usage exceeds CC debt. Personally, although I have several debit cards, none has ever been used. My first CC was a BankAmericard (now Visa) sent to me unsolicited in the 1960s. I have only carried a CC balance three times for a month and none for over 40 years. I actually had two credit cards taken away from me for low usage and paying the balance when due (Gen Motors and Sears). I use my cards for everything except monthly bills and why not as it shifts paying bills for a month.