Asked during Wednesday’s press conference whether easier financial conditions as a result of buoyant stock prices “make your job harder,” Jerome Powell resorted to a familiar rejoinder. The Fed is concerned about “overall financial conditions,” which should “reflect the policy stance,” he said.

It was a boilerplate response and to some, it seemed incongruous with the unusually explicit rebuke of markets and the read-through of higher stocks for financial conditions found in the December meeting minutes released early last month.

Powell doesn’t like to address stocks directly, which is understandable, and five months ago, during a terse Jackson Hole address, he proved he can get his point across if he really needs to. But in late November, during remarks for a Brookings event, he also proved he can inadvertently perpetuate rallies if he’s not careful.

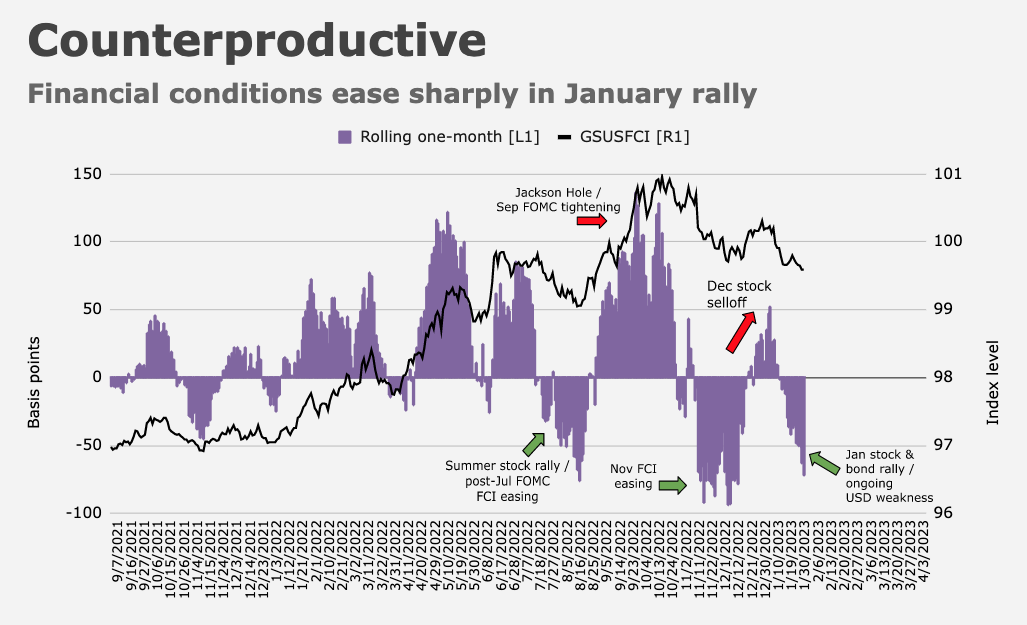

The problem currently is that financial conditions eased materially in anticipation of Wednesday’s step down to 25bps rate hike increments. December wasn’t kind to stocks, but January was, and December’s surprise gain in US pending home sales was a testament to the notion that 90bps off the 30-year fixed is more than enough to rouse the animal spirits on Main Street.

The Fed is concerned about services inflation excluding housing (shelter disinflation is assumed to be “in the pipeline”), but if long-end yields keep falling, the Committee may soon have to worry about house prices again too. Insult to injury for a panel of technocrats keen not to relinquish progress in the inflation fight is the link between long-end yields and the most speculative corners of the equity market. 10s were richer by almost 12bps on Wednesday following the Fed. It was no coincidence that the Nasdaq 100 surged more than 2%.

Everyone knew the odds of Powell browbeating markets into submission were low, but the fact that bonds rallied, stocks surged and the dollar dove despite no change to the critical “ongoing” language in the FOMC statement was very notable. “Everyone will still dissect the press conference, but it really doesn’t matter how Powell tries to explain any changes to this statement line,” Nomura’s Jack Hammond said, referencing the same passage prior to the decision. “They either leave it the same or change it and that is all you need to know.”

That one word (“ongoing”) confirmed the Committee’s intention to hike in March and May. If there was any lingering confusion, Powell effectively acknowledged that two more hikes are the base case during the press conference. But it didn’t matter. Five-year reals plunged 17bps. The dollar had one of its worst days this year. And Cathie Wood’s flagship, fresh off a near 30% gain in January, rose more than 4%.

Then, after the bell, Meta managed to impress. Between a top-line beat, convincing commentary on cost discipline and a buyback boost, investors were elated. Although revenue growth was negative again, $32.2 billion beat estimates, and more importantly, Meta tempered its expense outlook.

“There really isn’t anything bad about this report,” one analyst remarked. “Meta’s Q4 results did not disappoint,” said another. The shares soared almost 20% after hours.

Mark Zuckerberg said the company is “working on flattening our org structure and removing some layers of middle management.” That’s probably bad news for those middle managers, but it’s good news for shareholders to the extent it saves money.

Meta now sees full-year 2023 expenses in the range of $89-95 billion. That’s a lot, but down from the $94-100 billion the company projected previously. Meta cited “slower anticipated growth in payroll expenses,” and Zuckerberg dubbed 2023 a “Year of Efficiency” at the company.

Although Meta’s pretensions to frugality were welcome, they’re a bit difficult to square with the red ink in Reality Labs, which bled another $4.3 billion during the fourth quarter.

For the full year, Zuckerberg’s metaverse dream cost almost $14 billion.

On Wednesday, he said Meta would be “deploying AI tools to help engineers be more productive.” One wonders if that extra productivity will show up in engineers’ pay. If you’ve ever looked at a long-term chart of US labor productivity plotted with hourly compensation, you probably know what I’m driving at. Indexed to 1950, there’s now a ~120pp gap between the cumulative increase in productivity and the increase in compensation. I’ve long wondered whether that dynamic would accelerate in the era of AI. I suppose we’re about to find out.

In any event, assuming Meta’s gains hold on Thursday, the rally could juice US tech shares, potentially adding to the financial conditions easing impulse that paradoxically accompanied the Fed’s (attempted) hawkish step-down.

{kind=link}

AI is replacing ‘offshoring to China’ as the next significant deflationary tool.

Call centers can cut staff by as much as 40-50% as AI continues to improve. Case study/legal research/data handling can be done by AI in a small fraction of the time it takes entry level human researchers, lawyers and so on.

Almost any job that works (inefficiently) with large amounts of data will be targeted by AI.

“Almost any job that works (inefficiently) with large amounts of data will be targeted by AI.”

NOOOOOOOOOOOO 🙂

More seriously, I think that AI will have limited effect on portfolio management because there are already so many quant / algo / data mining technologies and strategies at work.

Other industries that to date have had less technological impact are likely to be shaken up harder. Commercial graphics and art, for example. An AI doesn’t need ADBE Photoshop or Illustrator to create imagery.

You didn’t even have time to qualify for long-term capital gains before it practically doubled!

Yeah, that was one of the better on-a-whim investments I’ve made in a long time.