Thanks to a multi-week decline in mortgage rates which helped catalyze a surprise increase in US pending home sales last month, “fresh” reads on the national home price indexes felt even more stale than usual on Tuesday.

Nevertheless, it’s worth noting that annual price growth on the closely-watched S&P CoreLogic Case-Shiller gauges ran at the slowest pace in more than two years in November.

The 20-city index rose 6.8% from the same month in 2021, while the national gauge posted a 7.69% YoY gain.

Both counted as especially “cool” in the pandemic era context and were just a bit above growth rates observed from 2013 through 2019.

“As the Federal Reserve moves interest rates higher, mortgage financing continues to be a headwind for home prices,” Craig Lazzara, managing director at S&P Dow Jones Indices, said Tuesday.

I’d gently note that any price appreciation is too much for scores of Americans priced out during the COVID bonanza, which is why it’s helpful that both the 20-city and national indexes dropped on a MoM basis in November, the former by 0.54% and the latter by 0.26%. November’s monthly decline on the 20-city index counted as the fifth straight.

Note that the pace of deceleration in the annual rate of price growth picked back up again in November (or down again, depending on how you want to think about it).

For clarity: That’s the month-to-month change in the YoY pace of price growth on the national gauge.

Meanwhile, FHFA prices fell 0.1% in November from October, separate data released Tuesday showed. Economists expected a 0.5% decline.

Although monthly price growth has effectively flatlined, prices remain supported by familiar pillars. “US house prices were largely unchanged in the last four months and remained near the peak levels reached over the summer of 2022,” Nataliya Polkovnichenko, the supervisory economist in the FHFA’s research division remarked.

Polkovnichenko continued: “While higher mortgage rates have suppressed demand, low inventories of homes for sale have helped maintain relatively flat house prices.”

Commenting further on Tuesday, S&P’s Lazzara said that, “Economic weakness, including the possibility of a recession, [could] constrain potential buyers.” Elevated odds of a “challenging macroeconomic environment,” might lead to additional declines in home prices, he suggested.

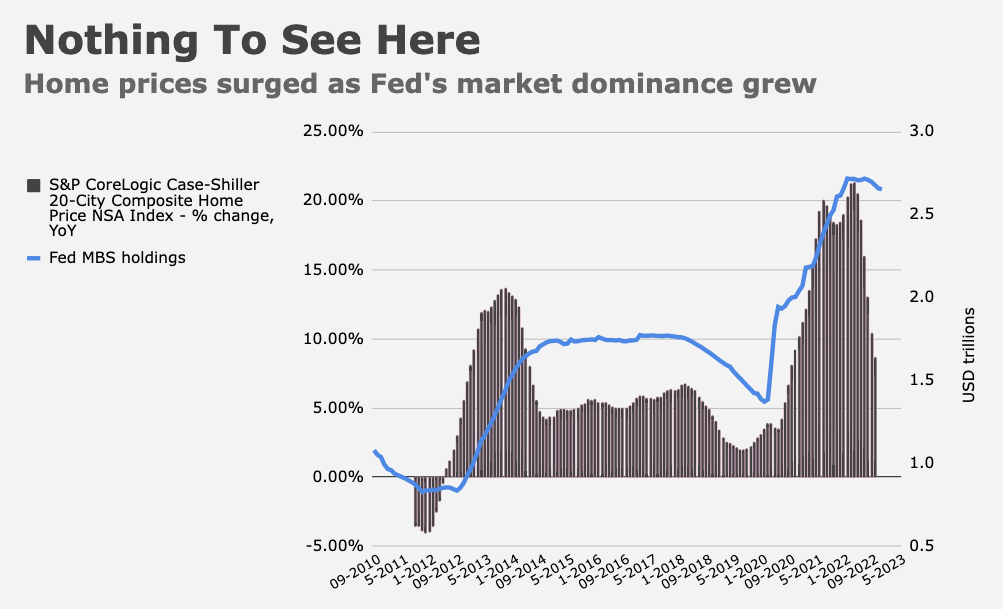

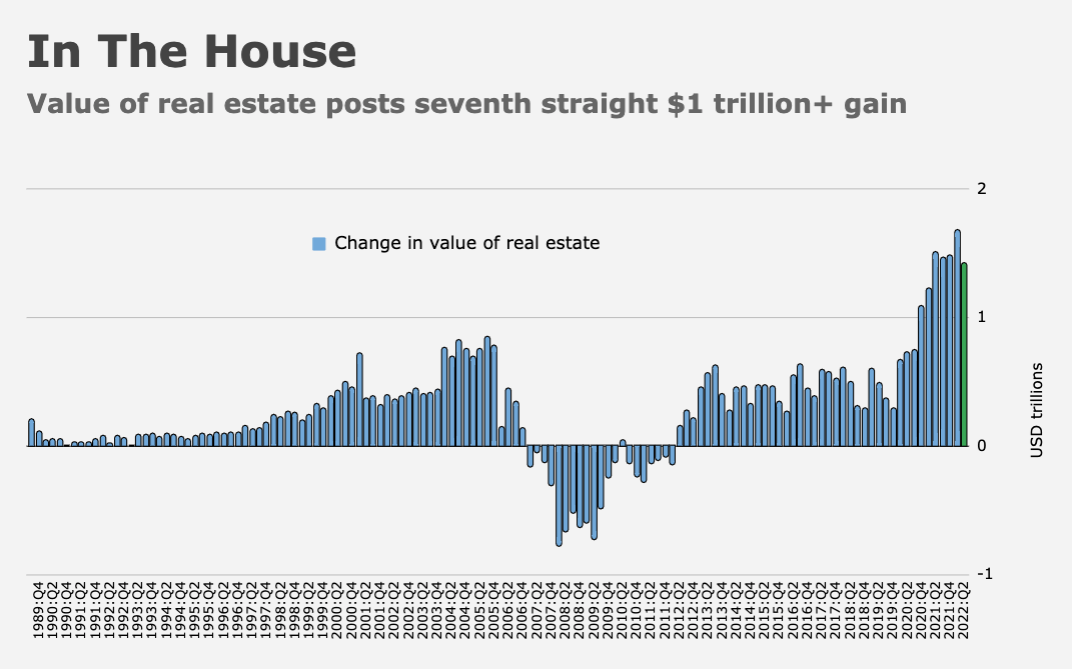

The problem for (too) many Americans is that rising rates were insult to injury. For them, it’s small comfort that the Fed, whose MBS-buying turbocharged the boom, is now attempting to correct the situation by squeezing the property market. Real estate, you’re reminded, racked up quarter after quarter of $1 trillion+ gains during the pandemic.

The property boom helped drive up services sector inflation, which in true “K-shaped” fashion, weighed most heavily on the same middle- and lower-income Americans who might struggle to afford a home. Now, they can’t even afford rent.

As the familiar chart above (updated with today’s Case-Shiller figures) suggests, shelter inflation is about to recede materially, which is obviously good news for the Fed.

But look, we shouldn’t lose track of the harsh reality: This is all too little, too late for Main Street. I’m weary of this discussion as it’s currently playing out among well-meaning pundits, economists and analysts, all of whom insist that shelter inflation is in fact already tamed. It’s not that I don’t believe the math (you can see it in a variety of more timely indicators). The issue is that the discussion is only relevant for people who don’t have to worry about paying rent and/or who already own a home.

For someone who’s currently apartment shopping, it’s irrelevant if the lease is 10% lower than what it would’ve been last year. Spoiler alert for every pundit, economist and analyst out there: $2,000/month is a helluva lot of money for regular people. The fact that it would’ve been $2,300 last year is meaningless. If you’re inclined to say that’s not meaningless at all because every penny counts on Main Street, I’d suggest that in itself is a damning indictment of American capitalism. The US is the richest country in the history of the world. No one should be in a situation where they have to “find” $300.

The bottom line on Main Street is that the rent is too high in no small part because of the pandemic property boom which the Fed knowingly facilitated, and the same property boom put home-buying out of reach for many renters. Home prices aren’t going to reset to pre-pandemic levels, or at least not across-the-board, nationally. From the perspective of many everyday people, all Powell’s rate hikes are doing is piling onerous financing costs atop sky-high prices.

Importantly, that’s certainly not to say the Fed should go right back to bubble policies in the interest of ensuring that at least the cost of borrowing is low for anyone brave enough to finance a half-million-dollar asset on a $75,000/year salary. Rather, the point is to say that some mistakes you just can’t fix. And when you try, you invariably make things worse.

{kind=link}

{kind=link}

In some places, apartment rents are dropping sharply, something likely to continue with typical developers’ overshoot momentum:

https://www.denverpost.com/2023/01/25/apartments-metro-denver-vacancy-rate-falling-rents

Are these declines for new renters or do they included legacy tenants? I doubt the latter.

The solution will end up being prices being pretty much flat over a long period of time as incomes grow. There is little doubt that real prices of shelter will drop- asking them to drop rapidly would probably make the cure worse than the disease (2008-9 was a good demonstration of that). There is a fallacy that homeownership should be a goal for all. That is a policy error born out of the propaganda from the GOP and real estate lobbies. Once you push ownership rates into the high 60s or 70% you get some folks who are probably not great candidates for home ownership. There is nothing wrong per se with helping folks live in decent rental housing via a subsidy or by reforming zoning and encouraging construction of rental units for low and moderate income folks. The focus of policy should be helping folks live better not pushing people to buy real estate who may not be good candidates to do so.

“The US is the richest country in the history of the world. No one should be in a situation where they have to “find” $300.”

Can’t they just tap their “excess savings” for that $300?

Perhaps they could open “shell” entities in the names of family members and tap it that way?

Did you learn that technique at Trump University’s George Santos College of Business?

“As the familiar chart above (updated with today’s Case-Shiller figures) suggests, shelter inflation is about to recede materially, which is obviously good news for the Fed.”

Any chance Case-Schiller explained WHY they think this precipitous drop of 10% over a period of 8 months is going to occur?

okay i somehow doubt that “The US is the richest country in the history of the world”