Traders, investors and Fed officials in their pre-meeting quiet period will all get a look at the first read on Q4 US GDP this week.

Spoiler alert: It won’t be indicative of a recession, although that doesn’t preclude efforts to spin it that way, belabored or otherwise.

Economists, famous for forecasting prowess, expect 2.7% from the headline. If you’re old enough (or young enough, as one reader recently put it, in a clever spin on my tired joke) to remember last month, you might recall that the final read on Q3 growth was accompanied by notable upward revisions that brought the headline to 3.2% from 2.6% as originally reported.

The numbers will be viewed as stale, even as the report incorporates some “new” information from December, which traders will get a more granular look at the following day.

Last week witnessed a rare “bad news is bad news” trade in and around lackluster readings on retail sales and industrial production, suggesting that the onset of recession, whenever it comes, won’t be greeted as warmly by risk assets as might be expected given the assumed read-through for monetary policy. (After all, the Committee continues to insist that rate cuts are basically out of the question in 2023.)

“The seemingly indefatigable US consumer is finally starting to tire out,” Wells Fargo said, of December’s retail sales stumble. “Some pullback in retail spending seemed inevitable after sales had surged more than 30% above early 2020 levels and the pandemic-induced shift to goods in lieu of services unwound [but] the details suggest the decline is more troubling than retail merely hitting an air pocket after demand for many items was pulled forward,” the bank cautioned. “Instead, the report hinted that consumers are retrenching more broadly.”

Consensus expects another healthy read on the personal consumption component in the GDP report. It too was revised up in the final read on Q3 growth, suggesting the US consumer wasn’t anywhere near tapped out headed into the holiday shopping season. Indeed, at 2.3%, the third read on spending for Q3 showed consumption was actually brisker in the third quarter than it was in the second. That made for a stark contrast with the initially reported pace, which was the second-slowest pace of the pandemic era.

My guess is that the risks are skewed to the downside given the apparent deceleration in nominal spending last month, but I’ve been wrong once or twice in my life (perhaps more, depending on who you ask).

“The growth outlook will be the most important driver of markets this year, and the retail sales miss last week fueled US recession fears,” SPI Asset Management’s Stephen Innes said over the weekend. “The sharp market response suggests the initial read was that this report could be the start of a very soft patch for US data and potentially the harbinger of recession,” he added, before suggesting it might not be wise to “read too much into that report as December has had a high seasonal hurdle in each of the last two years.”

Investors will parse December’s personal income and spending data on Friday. Its market-moving potential will be blunted by the GDP release the previous day, but economists will watch the details of the spending numbers in the context of the retail sales miss, and it goes without saying that any upside surprise on the core PCE price gauge would be unwelcome.

Consensus expects 0.3% from the MoM core print. That really needs to cooperate, although with another “cool” (and that’s an extremely relative term in this context) CPI report on the books, and a further step down to 25bps hike increments now fully socialized among traders, there’s no chance of this week’s data shifting the odds materially back in favor of a 50bps hike on February 1.

“Those on recession watch are far more focused on mid-2023 than the present and, therefore, we don’t anticipate an especially sharp response to Thursday’s [GDP] print in either direction,” BMO’s Ian Lyngen and Ben Jeffery said. “Within the details of the growth profile, the combination of GDP and Friday’s spending/income figures will give the market a better understanding of the trajectory of consumption, which could have a more material influence on both investor and Fed expectations [but] investors are content with the well-telegraphed intention to downshift to quarter-point hikes for the rest of the cycle.”

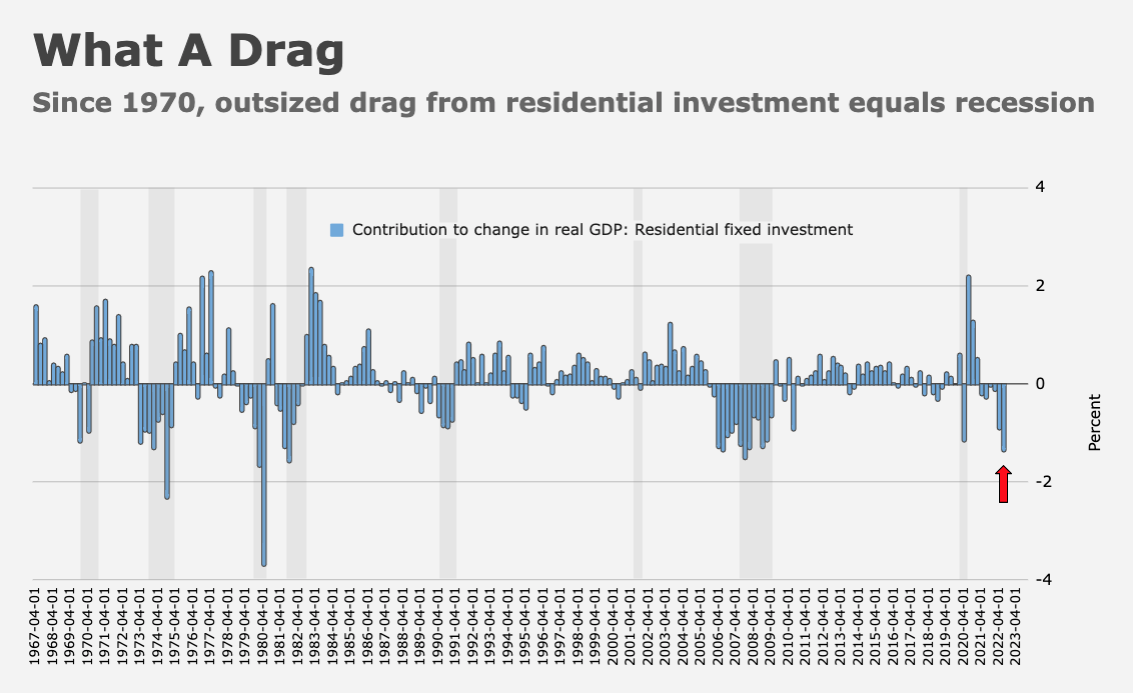

In addition to the above, this week’s data docket for the world’s largest economy includes flash prints on S&P Global’s PMIs, the final read on University of Michigan sentiment for January, as well as new home sales and pending home sales. Do note that according to the residential fixed investment component of GDP, the US is almost surely headed for recession.

{kind=link}