If you weren’t apprised, Morgan Stanley is a business that “facilitates capital for clients to reach their goals.”

That’s according to the latest edition of James Gorman’s annual strategic update slide deck, which was amusingly blunt for 2022 (he’d probably use a different adjective).

Gorman included a slide that categorized acquisitions and exits by way of “likes” and “dislikes.” Morgan Stanley, he said, likes to own wealth and investment management businesses, advisory, capital markets sales and trading operations, as well as “scale business” and major markets. By contrast, Morgan Stanley doesn’t like to own unsecured consumer credit, payments businesses, physical businesses, sub-scale businesses or any “fringe markets.”

I’m not sure whether Gorman was trying to draw a distinction between the firm and Goldman, where David Solomon is struggling with some businesses that would probably land in Morgan Stanley’s “don’t like” list, but he might’ve been.

Gorman’s traders fell short in Q4, or short of consensus anyway. FICC revenue of $1.42 billion was a nontrivial miss relative to the $1.7 billion the Street expected, and equities revenue of $2.18 billion didn’t quite measure up either.

IB revenue of $1.25 billion was obviously down sharply from the prior year’s quarter, consistent with the Street-wide trend, but it topped estimates.

The firm’s earnings releases are short on color, but the bank cited the same factors everyone else did in IB. Lower completed M&A, a “substantial” decline in equity underwriting volumes and a macro-related drop in bond and loan issuances.

None of that was great news, but if you looked past it, the firm’s results seemed ok. Wealth management revenue beat handily and at $6.63 billion, notched a record thanks to higher net interest income. “We don’t believe NII has peaked,” Sharon Yeshaya said Tuesday.

Excluding integration costs, the pre-tax margin in wealth management was 29.2%.

On the top and bottom lines, the firm beat estimates, even as revenue of $12.7 billion represented a 12% drop from the same period last year. Non-compensation expenses rose 2.5%. Comp costs were higher in Q4 versus Q4 2021, but fell for the full year.

Gorman called the results “solid amidst a difficult market environment.” Wealth management, he said, “provided stability” while investment management “benefited from diversification.” And so on. His commentary is infallibly dry which, frankly, I appreciate as a shareholder.

Oh, and I suppose I should note that the full-year results included an $876 million mark-to-market loss on corporate loans held for sale and loan hedges.

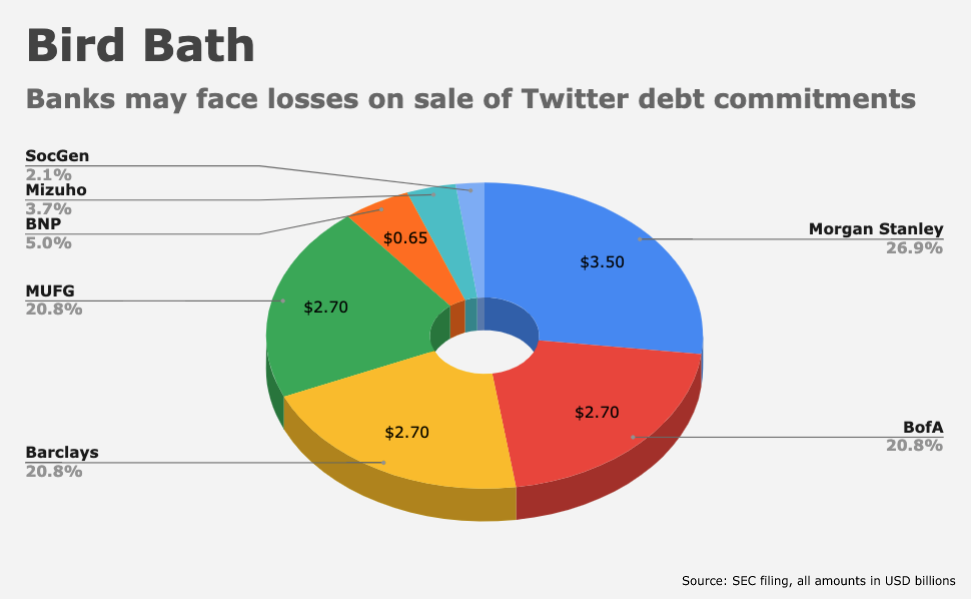

Morgan Stanley is, of course, the proud owner of the largest chunk of Elon Musk’s Twitter debt.

{kind=link}

Some years ago (for me it seems everything was “some years ago”) I was engaged to evaluate a privately-held wealth management firm the client wished to acquire for his bank. As I dug into the mechanics and economics of this business I made one major discovery: this business is egregiously profitable. Margins were in the range of 50%. How can you miss with that kind of profit? I guess it is a “stabilizing factor” for Morgan, and others of its ilk. I made one other discovery. Success in this business is totally dependent on the presence of quality people. As I looked over this target it was clear that after it was sold all the principals in this firm would take their cut and leave, making the firm into a Rolodex. I told my client the business was very profitable and valuable if nothing changed, but since I expected major change I told him to pass. He paid me but didn’t take my advice and got in a bidding war which led to a price at least double the firm’s value. Fortunately, my client lost the war. Two years later the firm had essentially dissolved and become worthless. I have always believed that when it comes to business, there are some customers you would rather your competitors took from you.

Mr. Lucky, right on – a money making machine. Get the asset mix right, 60/40 or 80/20 or whatever to fit the client profile and hammer it for 75 BPS of AUM. Then it becomes client relations and service which means quarterly reviews. Assume 5 or 10 BPS for over head; then the broker splits are another 15 to 25 BPS and you carry 30 to 45 BPS into your pocket. Broker/advisers are highly paid so no labor issues. Even if you juice broker payouts, at a minimum you make 20 BPS. It just becomes a game of AUM. Small AUM accounts you give to the bots to service.