There was a time not so long ago — and by that I mean prior to December 20 — when Haruhiko Kuroda was prone to suggesting that any tweaks to the Bank of Japan’s easing regime would be akin to hiking rates.

The implication was that even if Japan’s policy settings were increasingly anachronistic given inflation realities and nascent evidence that wage pressures were building across the world’s third-largest economy, policy would remain unchanged for the remainder of Kuroda’s term, which ends in April.

As the yen weakened rapidly against the dollar last year, it felt increasingly like the BoJ and the Japanese government were tolerating Kuroda’s obstinance more out of respect for his “contributions” and service to the nation than out of any earnest belief that yield-curve control (for example) still served a purpose.

To be sure, officials weren’t under the impression that Japan had definitively escaped the quagmire. That is: No one suggested that 2022’s bout of inflation was enough to thaw the permafrost, dislodge the deflationary psychology among Japanese consumers and light a fire under stagnate wages. The issue, rather, was that Kuroda’s insistence on capping 10-year JGB yields no matter the cost meant that on days when yields across other developed economies were rising and JGB yields were near the upper-end of the YCC band, rate differentials moved against the yen by definition. With prices for energy and food soaring, the ever weaker yen meant a larger and larger import bill.

That was all inflationary, but it wasn’t necessarily conducive to the kind of virtuous dynamics policymakers always imagined would help free Japan from deflation. In short: Kuroda’s YCC regime was past its shelf life, at best. At worst, it had become unsustainable. For the first time, betting against Kuroda was something more than a quixotic lottery ticket.

Although currency interventions and a less onerous policy juxtaposition with the US (as the Fed dialed back the pace of rate hikes amid signs that inflation was set to moderate) helped pull the yen back from the brink, the yield cap under Kuroda’s YCC regime still looked woefully disconnected from reality as the curtain closed on 2022. And, so, the BoJ widened the band in a “shock” move late last month. Suddenly, tweaks weren’t akin to rate hikes anymore, according to Kuroda. Instead, they helped make YCC more sustainable. In the December statement, the bank unironically cited deteriorating market functioning in government bonds.

Predictably, yields moved almost immediately to the new ceiling, jumping the most in two decades that day. Late last week, when 10-year JGB yields breached the upper-end of the band, the BoJ bought a record JPY3.2 trillion in bonds to defend the cap.

Suffice to say this isn’t tenable. Perhaps not even for another three months, which is why markets are on edge about another potential surprise from the BoJ prior to Kuroda’s exit.

Indeed, there’s rampant speculation that another tweak could come as soon as the January meeting this week. Local press reports suggested the bank is in fact studying the “side effects” of its easing program, and not for the first time either.

I bring this up because although an overnight abandonment of YCC prior to Kuroda stepping down isn’t especially likely, it’s possible, and it’d make a lot of waves.

“We view the BOJ’s yield cap shift last month as the first of many. Pandora’s box has been opened, and it will be very difficult to contain at a time when the global backdrop has meaningfully shifted on a number of fronts,” TD analysts including Mazen Issa and Priya Misra wrote. “We think markets should potentially be prepared for a 1% 10-year yield cap by the time Kuroda exits and eventual call for a removal of YCC.” The bank expects another 25bps adjustment this week (i.e., the ceiling would be 75bps).

TD nodded to the subtle joke inherent in my characterization of the BoJ’s December statement language as “unironic.” “Since the December meeting, the BOJ has significantly upped its JGB purchases,” the bank said. “This is unsustainable and… also counterproductive to what Kuroda aimed to do by shifting YCC — improve bond market functioning, which has deteriorated to near its lowest point since the inception of the BOJ’s survey.” The message: You don’t fix a market function problem by taking additional steps to corner the market. That’s why the market is broken in the first place.

“Our economists’ baseline is for the BoJ to maintain YCC, while acknowledging the possibility of further tweaks [but] with the BoJ set to upgrade its inflation outlook and continued market pressure, a more concrete shift in policy (or setting of the stage for a future shift) remains a risk,” Goldman said late Friday, noting that markets “largely appear to be placing relatively high odds of at least another adjustment to, if not an outright exit from, YCC [with] 10-year JPY swap rates at 1%, and JGBs that the BoJ is not explicitly offering fixed-rate operations on trading above the upper-end of the tolerance band.”

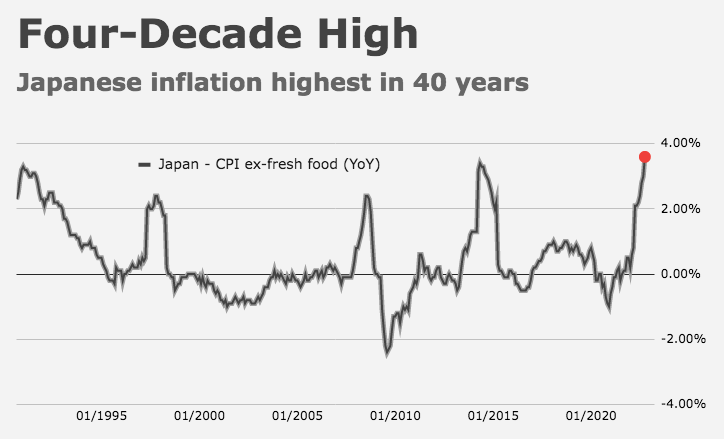

New economic projections from the BoJ will probably nod to higher inflation. After all, consumer price growth is the highest in decades. Fast Retailing’s decision to lift wages by as much as 40% suggested the BoJ is finally getting the pay growth it’s after, even as real earnings remain deeply negative thanks to what, in the Japanese context, counts as very high inflation. Upcoming wage negotiations are a focal point in the policy discussion.

Needless to say, a rollback of YCC, whatever form it takes, will spill over into other locales, and not just via the signaling effect. Although Japanese investors sold G7 (plus Aussie) bonds in 2022, potentially leaving less to sell as the BoJ pivots, higher yields at home and a stronger yen would, at the least, make domestic assets more attractive. That discussion is far too nuanced to be amenable to any sort of summary treatment, but it needed a mention.

Bottom line: Additional adjustments from the BoJ are almost surely coming, it’s just a matter of when and whether those adjustments take the form of tweaks or more substantial steps towards an exit from extreme accommodation. A major stride at the January meeting is merely a tail risk, but the gathering will be eyed very closely, and ears will likewise be open for any potential “creativity” in terms of rhetoric aimed at corners of the market where speculation on a policy shift is readily apparent. Oh, and Japanese inflation data for December is due Friday.

{kind=link}

Often the end of qe has counterintuitive effects after the very short term

BOJ adjustments higher leads to more funds coming home and higher treasury rates?

Bloomberg has a piece this morning on the BoJ with “Pandora’s Box” in the headline. Pure accident, no doubt.