So far in 2023, US equities are up nearly 4%. At the same time, the most popular long-end US Treasury ETF is up more than 7%.

That’s a welcome reprieve after 2022, when both stocks and bonds fell together, in what counted as a singularly terrible year for a “traditional” balanced portfolio.

Note the scare quotes around the word “traditional.” If you’re younger than, say, 40, you were raised in the era of the 60/40 portfolio, and you were probably taught to regard the bedrock assumption behind such portfolios as sacrosanct. Diversification is crucial, and bonds cushion equity drawdowns. The correlation between stock and bond returns is generally and reliably negative (the correlation between equities and yields is generally and reliably positive).

In some important respects, the basic logic is enduring (you want safe assets to balance out your exposure to risky ones). And yet, the 60/40 religion is a fairly recent phenomenon. Like a lot of other things, the respect we accord to that simple asset allocation split is the product of recency bias. Embedded in that bias were assumptions about the supposed inviolability of certain macro dynamics which ceased to hold beginning in late 2020.

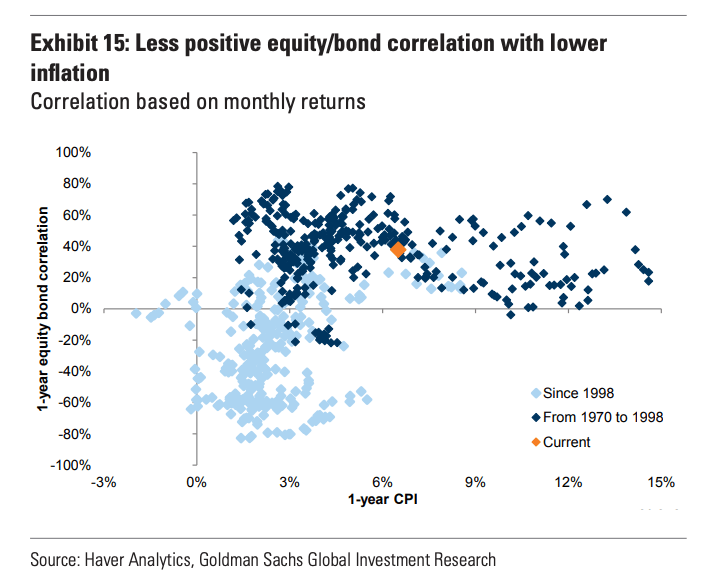

As Goldman reminded investors this week, negative stock-bond correlation regimes are actually the exception, not the rule. “Only during the 1920s, the 1950/60s and since the late 1990s were equity/bond correlations consistently negative as inflation was generally anchored,” the bank’s Christian Mueller-Glissmann wrote.

“In the 1970s and 1980s in particular, the equity bond/correlation was mostly positive — during the stagflation periods and the oil crisis, high inflation and higher bond yields often weighed on equities,” Mueller-Glissmann went on to say. “Since the COVID-19 crisis, 12-month rolling correlations have also turned positive and are above the levels reached around the US ‘taper tantrum’ in May 2013.”

When you ponder that chart (and the scatterplot shown below), it’s remarkable how naive we’ve been. Most obviously, we were quick to take for granted the sustainability of circumstances which, in the past, rarely held for very long. At the same time, we never stopped to consider the possibility that negatively correlated assets which, despite their tendency to move opposite one another, have nevertheless rallied simultaneously over a three-decade investment window, was a conjuncture too good to be true. It was made possible in no small part by structural disinflation, which perpetuated ever lower bond yields and, particularly after 2008, provided central banks in developed economies with plausible deniability to persist in a policy bent that buoyed financial assets of all sorts.

The linchpin was subdued inflation. As you might’ve heard, inflation made a comeback in 2021 before running amok in 2022. The result was a simultaneous drawdown in stocks and bonds, which compelled investors to confront a very uncomfortable reality: The correlation assumptions we took for granted while worshipping 60/40 were misguided. They depended for their legitimacy on a benign macro backdrop. When the macro regime shifted, the correlation broke down, we lost our religion and the rest is history.

Again, it’s important to acknowledge that what we’re experiencing in terms of stock-bond correlations and inflation is really just a reversion to the historical mean. And that’s a microcosm of a larger dynamic that’s dominated the macro discussion in these pages over the past 24 months.

We assumed The Great Moderation and Pax Americana were the new normal. Now, we’re learning that they might’ve been anomalous periods of calm destined for disruption. If that’s true, we need to unlearn much of what we thought we knew about portfolio construction to the extent that knowledge was based on faulty correlations predicated on a macro regime that no longer exists.

In that respect, my views overlap with Zoltan Pozsar’s, even as I’ve become (very) wary of his increasingly ambitious macro theorizing. Late last week, Pozsar warned that “60/40 won’t cut it anymore.” Instead, he said, the split should be 20/40/20/20 “with the weights representing cash, stocks, bonds and commodities.” The bullet points below are from the same note. They serve as a summary of Pozsar’s cross-asset view, and are lightly edited for clarity:

- Cash, while the curve remains inverted, is “king.” It provides a nice yield, has no duration risk and, as Warren Buffett said, it has an option value.

- Commodities should include three types of gold: Yellow, black and white. Yellow gold is gold bars. Black gold is oil. White gold is lithium for EVs.

- Commodities should also include a range of other stuff like copper, cobalt, etc., and the general theme driving commodities is that after years of underinvestment, supply became extraordinarily tight, just as we re-arm, re-shore, re-stock and re-wire the grid.

- The US dollar won’t be dethroned overnight but on the margin, de-dollarization and digitization (CBDCs) by BRICS+ central banks will reduce dollar dominance and demand for Treasurys.

- The dollar’s strength or weakness should be thought of in the context of the four prices of money (that is, par, interest, FX and the price level: The US dollar will remain ‘FX’ strong versus other DM currencies but will be become ‘price level’ weak (that is, outright devalue) versus commodities and ‘FX’ weak versus most BRICs currencies.

Those passages from Zoltan run the gamut from consensus to… well, something other than consensus. Take them for what they’re worth, but do remember that just because something sounds smart doesn’t mean it is. Everything Pozsar says tends to sound smart on a quick read.

Coming back to Goldman, Mueller-Glissmann suggested that although the equity/bond correlation is likely to become less positive this year, a quick return to the negative regime investors grew accustomed to over the past two or more decades isn’t guaranteed.

“Inflation above 3-4% has usually resulted in a more positive correlation due to higher rates volatility, with supply-side shocks dominating relative to demand shocks,” he wrote. “Elevated inflation moves the ‘central bank put’ further ‘out of the money,’ requiring a larger ‘growth shock’ for central banks to ease,” he added. “On the flip side, inflation above central bank targets means risk of further hawkish surprises near-term, especially in the event of too much easing of financial conditions.”

Goldman’s economists see US inflation running between 5% and 6% this year.

While I have no reliable answers or insights, I do feel like I have never known more or been smarter about markets, or had easier and more timely access to comparatively top notch data, analysis and commentary than I do now. I have evolved into an instinctive contrarian but have guiltily participated in my generation’s bubbles. My religion used to be reading Barrons cover to cover each week, excepting the weekly 45 pages of price quotes. I recall a seminal point where the publication bowed to the bifurcated demands of its readers to cleanly segregate the quotes into their own pull out section that could either be stored for eternal reference in a pile on some bookcase, or quickly disposed of in order to reduce the volume and packing weight of each issue by about 2/3rds. I was in the latter camp, thanks to my $0.49 per minute dial-up Telescan service that made printed stock quotes my generation’s OK boomer symbol.

And that is all just a lot of verbiage to say there is a real risk in accumulating knowledge and experience and having access to information in that you are inclined to think you’ve seen this before or know what it means and know what to do. I remember your post(s) that old school analysts were being put out to pasture in our QE regime because they couldn’t get comfortable paying 35x sales, were consistently lagging their “peers,” and just couldn’t be reprogrammed at this point They lacked courage. (And then energy rallied and FAANG reverted).

It is popular to declare that these are unprecedented times in the face of uncertainty, but for once in my life I feel like this may actually be true. For me, my lifetime-honed contrarian bend has sort of fattened and softened with age to a more flabby, anti-conviction stance. Do your homework. Move in and out in increments not big swings. Manage position sizing. Harvest better than expected cap gains and don’t let losses run. Write more calls and puts. In the end, my life’s education and experience in the markets seem well biased on the side of the unexpected thing happening. Or, to compound that, when the response to the unexpected thing happening was no where near what would have been expected in advance. The age old complaint — “even when I’m right, I lose money.”

But while we may be fooling ourselves by not fooling ourselves (getting smarter), this is already another really solid post to start the first couple of weeks of this year. As confused as I may sound, I give this blog a lot of credit for keeping me in touch with my (actual) reality. And if that’s not clear, it is intended as high praise. My only conviction is to have no conviction.

ditto. Thank you

I agree with much that you are saying, although as an options trader I tend to buy or sell premium based on price rather than inclination. I do try to screen out even excellent commentary, such as that sold by this site, when it comes to trading decisions. In my opinion, price is, in the end , the only thing that really matters.

“My only conviction is to have no conviction.” Perhaps we are saying the same thing?

That’s what successful flow traders (Folks in a pit, market makers & such) do. Approach every day as a blank slate.

I did that for a number of years but it’s really not applicable to investment management with a longer-term horizon.

Good observation. In financial theory every day is a clean slate but if you have a diversified portfolio with a large number of holdings, that slate is almost impossible to evaluate. And, as you so aptly observe, all those daily changes make one a trader not a long-term investor. (I’d never looked at this as a paradox before. Thanks.)

BTW, I really like your comments on this site.

I return the sentiment regarding your posts. Thanks!

Sorry to jam up the comments section on this topic.

But Mr. Lucky I once worked on a trading desk where the boss recognized the distinction. He said he wanted three or four flow traders/market makers to bring in a steady monthly income to provide a cushion for the big prop traders on the desk.

I was lucky enough to do both at times. A pinnacle was in 1979 when I quoted 45-52 and the counterparty replied “thanks for the nice price but nothing.” You see. Everyone else was quoting 45-55. That was $45.00/$55.00. A bit of a bid-offer spread eh?