“We are skeptical about a durable rally,” JPMorgan analysts led by Marko Kolanovic said Monday.

They’re not alone. Seemingly everyone is skeptical which, ironically, can help to explain large upside moves on favorable macro catalysts, like that which played out following December’s “Goldilocks” US jobs report.

If you ask JPMorgan, any rebound in global economic activity may prove fleeting. “We are unlikely to end up with a soft landing and the market could soon start focusing on the eventual impact on earnings,” the bank said.

Earnings growth likely flatlined for corporate America in Q4, and the most bearish of strategists suspects markets might yet be surprised at the scope of any profit recession.

Kolanovic and co. noted that the latest JPMorgan PMI data suggested the global economy might’ve managed to skirt a recession last year despite the energy crisis, and downside momentum could’ve bottomed in November. Nevertheless, “the lagged effect of realized and prospective monetary tightening still lies ahead,” the bank warned, adding that even if a recession doesn’t materialize in the near-term, the odds of the global expansion ending over the next 24 months are very high.

“Inflation remains on a downward path, while cooling is becoming more evident also in labor markets,” the bank went on to say, while acknowledging that the jobs market in the US is still “on the strong side.”

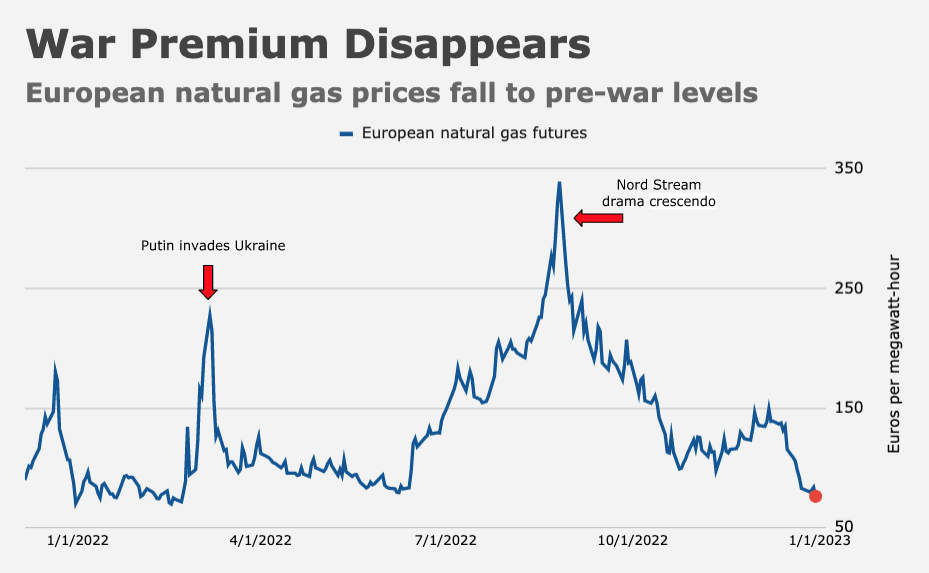

JPMorgan said the current “cocktail” of growth, inflation and labor market data favors fixed income, but “should eventually become more challenging” for stocks even if, in the near-term, equities react favorably to receding price growth, evidence of a cooler jobs market, China’s re-opening and the decline in European gas prices. “Bearish positioning/sentiment and thin liquidity make stocks reactive to these developments,” the bank remarked.

Ultimately, though, the odds of a soft landing are slim, and as the impact to earnings (e.g., from decelerating growth, margin compression and tighter monetary policy) becomes more clear, equities could shudder anew.

The bank also mentioned the December FOMC minutes, which contained an explicit reference to the counterproductive impact of market rallies on financial conditions in the context of the inflation fight. The following passage, from Michael Feroli, is worth quoting:

Minutes [from] the December FOMC meeting made sure to call out that nobody on the FOMC anticipated rate cuts in 2023. The tactical goal of this rhetoric seems clear enough: By leaning against rate cut expectations the Committee hopes to forestall any further easing in financial conditions. The broader communications strategy is less clear. Absent some more fundamental change, expectations for policy rates beyond six months are likely to keep rolling down the hill.

Key takeaways from JPMorgan’s outlook include a recommendation to take profits on European shares given the likelihood of ongoing rate hikes from the ECB (which became the most hawkish DM central bank last month), a reiteration of the bank’s Overweight in Chinese stocks and emphasis on the potential for credit to outperform equities in 2023 “given conservative balance sheet management and likely strong inflows,” even as spreads may move wider in any pronounced stock selloff.

{kind=link}

It’s been so long since corporate earnings drove stock prices. Yet we old-timers keep on believing, hoping to justify our employment.

Corporate earnings drive relative performance, so there is some use for us yet 🙂

Good point. They are useful in that context.

I’m just reacting to the price action we enjoyed over the past 25 years. Was it Goldman which pointed out that aggregate earnings in the US economy barely budged between 2010 through 2019? They concluded that something like 90% of the stock market appreciation was due to multiple expansion, aided and abetted by share buy-backs which were often funded by borrowing.

I like your idea, here, Derek. Expansion in the last 20 years has been monolithic. My underlying fear is that the war in Europe, changing international politics (especially in China), evolving and more severe climate change are building uncertainty around the world, especially in regard to food production. I’m concerned we will continue to see negative effects on the broader world economy (and certainly the US).

Innovations in alternative energy and food production are becoming necessary.

Does reality matter, not too sure anymore :-/