Those of you old enough to remember three weeks ago will recall that Jerome Powell and his colleagues at the Fed leaned marginally more hawkish than expected in the economic projections that accompanied December’s 50bps rate hike.

Despite two consecutive downside surprises in the incoming inflation data, the median forecasts for price growth in 2023 were revised up, to the consternation of at least some market participants.

Of course, you could easily suggest the Fed was just being prudent — finally. They’ve spent the past year playing catch up to the hottest inflation in a generation, and although their forecasts didn’t prove to be quite as embarrassingly misguided as the Bank of England’s, that’s a pretty low bar. I, for one, didn’t blame the Committee for collectively suggesting that core PCE may still be lingering well above 3% by the end of 2023. That didn’t (and still doesn’t) seem far-fetched.

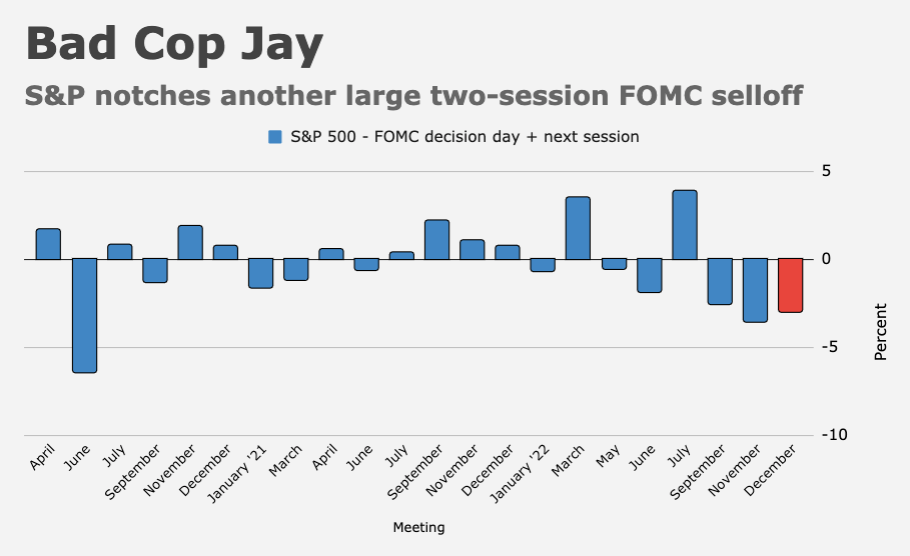

Markets, though, wanted a dovish outcome consistent with the benign monthly CPI prints from October and November. Instead, they got upward PCE revisions and a dot plot that tipped a terminal rate above 5%. Stocks weren’t amused. The S&P logged a third consecutive two-day FOMC selloff.

Discouraged equities subsequently trundled lower on the way to a very poor December showing which served to erase nearly half the rousing rally seen during October and November.

Minutes from the Fed’s December gathering released on Wednesday seemed to validate the market’s hawkish interpretation. “Participants noted that, in the latest inflation data, the pace of increase for prices of core services excluding shelter — which represents the largest component of core PCE price inflation — was high,” began one key passage. And then:

They also remarked that this component of inflation has tended to be closely linked to nominal wage growth and therefore would likely remain persistently elevated if the labor market remained very tight. Consequently, while there were few signs of adverse wage-price dynamics at present, they assessed that bringing down this component of inflation to mandate-consistent levels would require some softening in the growth of labor demand to bring the labor market back into better balance.

That’s hawkish, and although the Fed continues to avoid conceding that a wage-price spiral is afoot, policymakers are plainly concerned.

The minutes reiterated that longer-term price growth expectations remain well-behaved, but even that came with a caveat: “However, participants stressed that the Committee’s ongoing monetary policy tightening to achieve a stance that will be sufficiently restrictive to return inflation to 2% is essential for ensuring that longer-term expectations remain well anchored.” That was followed by familiar language emphasizing the perils of allowing expectations to become unmoored.

One passage was overtly foreboding. “Participants cited the possibility that price pressures could prove to be more persistent than anticipated, due to, for example, the labor market staying tight for longer than anticipated,” it began, before continuing as follows,

Participants saw a number of uncertainties surrounding the outlook for inflation stemming from factors abroad, such as China’s relaxation of its zero-COVID policies, Russia’s continuing war against Ukraine, and effects of synchronous policy firming by major central banks. A number of participants judged that the risks to the outlook for economic activity were weighted to the downside. They noted that sources of such risks included the potential for more persistent inflation inducing more restrictive policy responses, the prospect of unexpected negative shocks tipping the economy into a recession in an environment of subdued growth, and the possibility of households’ and businesses’ concerns about the outlook restraining their spending sufficiently to reduce aggregate output.

That read quite a bit like a bullet point list of macro risk factors from a sell-side note.

There were, of course, nods to long and variable lags, rampant uncertainty and the benefits of slowing the pace of rate hikes as policy approached sufficiently restrictive settings.

But on a quick read at least, it was (very) difficult to come away from the account of last month’s meeting with anything other than a hawkish interpretation. Indeed, the minutes explicitly cautioned on the risks associated with easier financial conditions brought about by “misperceptions” of the Fed’s intentions.

“A number of participants emphasized that it would be important to clearly communicate that a slowing in the pace of rate increases was not an indication of any weakening of the Committee’s resolve to achieve its price stability goal or a judgment that inflation was already on a persistent downward path,” the minutes said, adding that “because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.”

Recall that between cooler inflation data and expectations for a step-down from 75bps hike increments, stocks rallied, bond yields fell, mortgage rates receded and the dollar weakened headed into the final month of 2022, thereby easing financial conditions materially. That worked at cross purposes with the Fed’s goals, but when given the opportunity to chide markets during remarks for a Brookings event in late November, Powell didn’t appear eager to spoil the party.

The account of the December meeting suggested some of Powell’s colleagues (and quite possibly Powell himself) weren’t enamored with the market reaction to the Chair’s Brookings speech, which traders generally viewed as a green light for the rally. The December SEP and, now, minutes from last month’s policy gathering, suggest that wasn’t his intent.

{kind=link}

{kind=link}

They are taking a prudent course, at least in their opinion which is all that matters. The shenanigans in the House suggest another possible source of shock. They will keep going until the punchbowl is nowhere to be seen let alone empty. At this point does it really matter if a recession is called or if we get 3% inflation and 3.5% nominal growth for an extended period? It will feel really ugly in that case or an outright recession. A short soft landing at this point looks impossible.

“Those of you old enough to remember three weeks ago will recall that…”

Here is another possibility: “Those of you not too old to remember three weeks ago will recall that….”

🙂

Comment of the year so far. There’s a long way to go, though.

Three weeks is setting the bar mighty high.

I do wonder, Mr. H., if you’re chuckling when you’re typing these little sarcastic quips?

I must admit, my favorites are those referencing economists. The one about “throwing darts while blindfolded” is up there with some of the best Mark Twain aphorisms.

Three or four Fed governors on tap today. Including their Ron DeSantis clone at 1:20. Do they reinforce the message or undercut the chairman, once again?