Seemingly everything is a double-edged sword these days from a macro perspective.

More to the point: Many outcomes we’d normally describe as “good” have the potential to stoke inflation or, at the least, to keep inflation elevated, which in turn raises the specter of tighter money in perpetuity as central banks attempt to reclaim lost credibility.

Of course, a prolonged period of relatively tight money may not be the worst thing in the world. Ostensibly, tight money will help restore price discovery, and correct myriad distortions brought about by a dozen years of martial-law-by-acronym (NIRP, ZIRP and LSAP) across markets. That won’t be painless, though. Unfettered price discovery is a wholly foreign concept to an entire generation of young traders.

Nowhere is the double-edged sword dynamic more apparent than in the outlook for real income growth in the US. Assuming goods inflation continues to abate (core goods inflation will probably turn negative) and services inflation doesn’t accelerate dramatically, it’s easy to imagine wage growth outstripping consumer price growth in 2023. If real disposable income is positive as a result, consumption across the world’s largest economy could be more resilient than anticipated.

“Real disposable income fell from the spring of 2021 through the summer of 2022 as inflation outran wage growth and special transfer payments included in pandemic relief packages expired,” Goldman wrote, in a note published this week. The bank sees real income turning positive in 2023, and ultimately rising 3.5%, “supported by positive real wage growth, large cost-of-living adjustments on transfer payments including Social Security and food stamps, a jump in interest income, and a decline in the effective tax rate as a spike driven by capital gains and bracket creep reverses,” as David Mericle and Alec Phillips explained.

Note that Goldman, in a helpful nod to the realities of income inequality in the US, differentiated between gains that are likely to accrue to the rich and those which should accrue to lower income brackets. The distinction is critical because, as discussed here on so many occasions that even I’m weary of debating the specifics, it’s consumers in lower income buckets who matter most for incremental growth, given their higher marginal propensity to consume, as mentioned in Goldman’s annotation.

“While gains from interest income and tax rate normalization will accrue mostly to high-income households and have less impact on spending, the turnaround in real income is nonetheless a key reason that we have a relatively optimistic 2023 consumer outlook,” the bank went on to say.

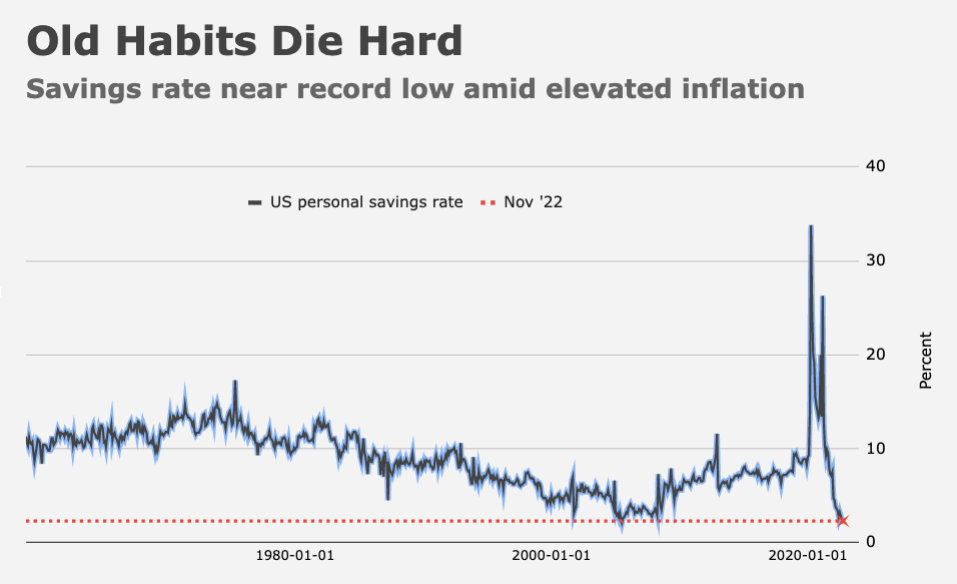

That brings us right back to the double-edged sword. An optimistic view on consumption, “relative” or otherwise, means harboring a hawkish view on the likely trajectory of monetary policy. However, Goldman expects some of the spending impulse to be restrained by a higher savings rate.

“Higher interest rates have reduced household wealth by lowering home and equity prices, and… the lower- and middle-income families that tapped excess savings to support their spending this year as transfer payments expired will have less to draw on next year,” Mericle and Phillips said.

As a quick aside, I’d point readers to the barely-visible green bars in the figure on the right above. That’s the projected drag on households from the crypto selloff. If you’re inclined to say you need a microscope to see it, I’d tell you that’s the whole point — as many headlines as the cryptoverse garnered this year, it’s virtually meaningless from a wealth effect perspective.

Recall that the savings rate has declined to near record lows in recent months, while revolving credit balances have ballooned. With the vaunted “wealth effect” now in reverse and the multi-trillion-dollar savings buffer dwindling, it’s likely that consumers will rediscover at least a semblance of discipline, or at least according to Goldman.

That said, betting on incorrigible American spendthrifts to stop spending is a tenuous proposition, but it’s certainly true that the juxtaposition between rising rates and ballooning card balances looks untenable.

I’ve mentioned this previously, but the pace at which revolving credit rose in recent quarters was brisker than headline inflation, which suggests higher card balances aren’t simply the product of higher prices.

At some point, the combination of swollen variable rate debt and higher rates will bite consumers, it’s just a matter of whether you believe that’ll be a minor inconvenience or a serious impediment to incremental spending.

Goldman was diplomatic on that point. “One important form that drawing on excess savings has taken is the rebound in consumer credit use, and while it remains below its pre-pandemic level as a share of income, its recent rapid growth rate is not sustainable and will have to slow next year,” the bank said.

All in all, Goldman expects consumption growth in the US to be around 1.5% in 2023, hardly giddy, but not exactly the stuff deep recessions are made of either. The more resilient the consumer, the more recalcitrant the Fed.

{kind=link}

If corporate profits get squeezed layoffs could start or hiring could fall off at the very least. The knock on effects would be an erosion of wage growth. That’s assuming labor hoarding goes away.

I don’t believe economists/banks have correctly measured the dynamic of prime age consumers that have over extended on recurring housing cost verse their income using “excess savings” to fill the gap. Now that their savings is running out credit balances are raising rapidly while they try to maintain their consumption lifestyle. Their credit will eventually tap out, then consumption crashes, then a relatively large number of consumers can’t afford their over priced mortgage/rent.

The present dynamic of income vs life affordability is way out of whack and small real income gains won’t save the day. The idea of a soft landing is and always was a fairytale.