It’s fair to say markets are obsessed with the idea that the last Fed hike of the current cycle — so, the hike that precedes the long-awaited “pause” — will be a green light for risk assets.

That may not be a viable strategy in 2023, though. Or at least not according to BofA’s Michael Hartnett, who, in the latest installment of his popular weekly “Flow Show” series, suggested that a “buy the last hike” mentality is yet another example of recency bias, and thus can’t necessarily be trusted following this year’s epochal macro regime shift.

Losses on Wall Street in 2022 were “driven by huge monetary tightening” and the Fed will likely hike for the last time in late March of 2023, he wrote, before adopting a cautionary cadence. “Recent disinflationary stock market history says ‘buy the last hike,’ but ‘sell the last hike’ was the correct strategy in the inflationary ’70s/’80s.”

The table (below) shows you the cross-asset breakdown of returns by regime, three and six months after 10 “last hikes” going back 50 years.

In inflationary regimes, you “sell the last hike” in stocks, which “fell after every last hike in the ’70s and ’80s as punishing Fed funds levels plunged the economy into recession,” Hartnett wrote. By contrast, you bought the last hike in the disinflationary era (basically The Great Moderation) “every time.”

As for Treasurys and IG credit, you buy them “always,” Hartnett said, noting that Treasury and high-grade bond returns were positive 9/10 times after a last hike.

Note that Treasurys are almost guaranteed to post a positive return in 2023 coming off a year so bad that no one would’ve believed you had you suggested the scope of this year’s bond market malaise ahead of time (figure below).

It’s impossible to overstate the shock value of that drawdown, particularly coming as it did alongside a bear market in stocks. 2022 was a veritable Chicxulub impactor for 60/40 portfolios.

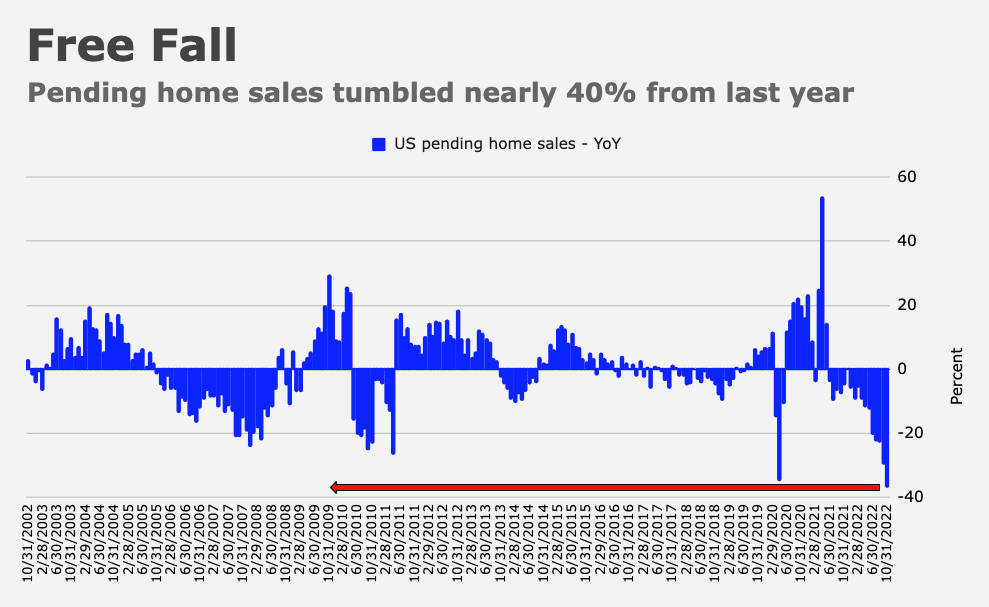

Hartnett also explained “why [a US] recession starts in the next 10-12 weeks.” The curve inversion is the deepest since 1981, oil is down 40% in six months despite ostensibly bullish catalysts including China’s reopening, bank stocks fell 10% in four days, ISM manufacturing new orders are down three consecutive months amid high inventories and on the housing front, US pending home sales fell -37% YoY in October, while house prices are down 13% in Sweden, 11% in New Zealand, 10% in Canada and 5% in Sydney from the highs.

Hartnett wasn’t actually predicting the onset of recession as soon as March. Rather, he was just laying out the case for those who might be inclined to make such a prediction. He also set out reasons why the onset of a downturn could wait until the back half of next year. Copper is up 25% from the lows, for example, while US gas prices are down sharply (which bodes well for consumption), the US services sector remains resilient, nominal wages are still rising rapidly (note that a decline in goods prices could improve real wage growth too) and unemployment rates are still “remarkably low,” not just in the US, but “everywhere.”

For what it’s worth, BofA’s pseudo-famous Bull & Bear Indicator rose to 2.6 this week, officially ending the contrarian “buy signal” for risk assets.

{kind=link}

As a small business owner who employs a fair amount of low-skilled, low wage employees (and one who strives hard to pay above average and take care of employees in ways that should be mandatory, frankly), I’ve been feeling squeezed by the wage inflation spiral in 2022. Now I’m struck with the realization that a planned minimum wage increase in my state (NJ) is going to increase that pressure to start the new year.

A solid 25 states (plus some municipalities across the US) have minimum wage increases coming in 2023. How this ultimately affects the indices that the Fed and the markets watch, I couldn’t say, but I think it will absolutely, at the least, add to the perception that wages are still rising faster then the Fed needs right now.

I admire your attitude towards the treatment of your employees. I trust that the higher minimum wage will help you in competing with rivals that are less concerned with paying a living wage.