Wednesday brought more disquieting economic data and more rate hikes, underscoring the tenuous nature of any glass half-full assessments.

Europe is probably in a recession and New Zealand saw fit to step up the pace of policy tightening amid a stubbornly resilient domestic economy and fears of perniciously entrenched inflation.

Let’s start in Europe. “Business sentiment remained gloomy by historical standards, and demand continued to fall at a steep rate, leading to a pull-back in employment growth during the month,” S&P Global said Wednesday, editorializing around a fifth month of contraction in private sector business activity.

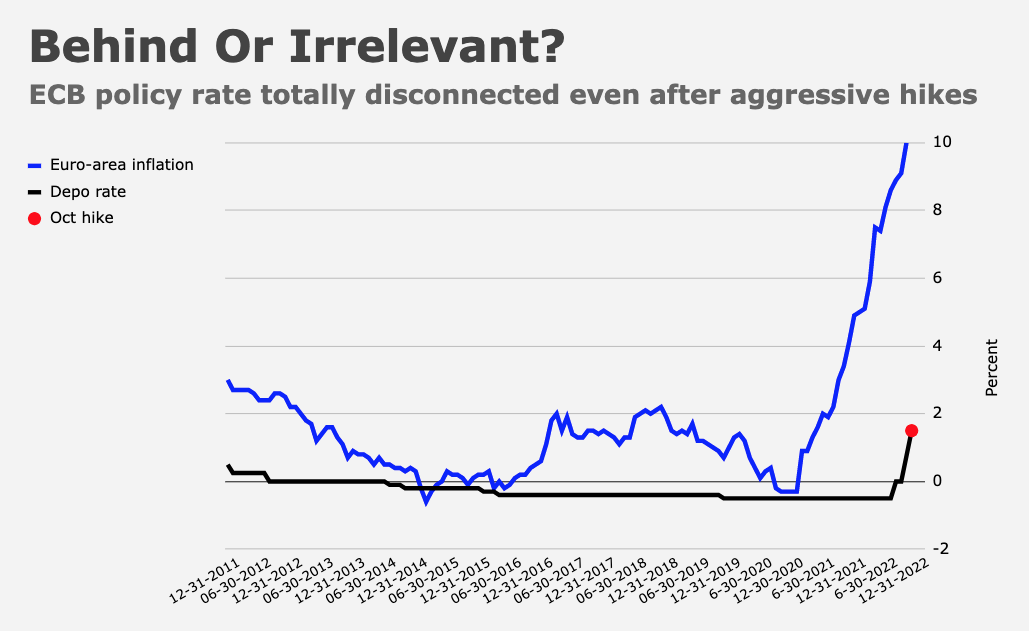

At 47.8, the flash read on the regional composite gauge improved marginally from October’s final print, and the same was true of the manufacturing PMI and the services index. But, as the figure (below) suggests, this is an inopportune time for the ECB to be hiking rates in large intervals.

Firms’ outlook improved “slightly,” but confidence was weighed down by growth concerns, the cost of living crisis, rising rates and, of course, the war in Ukraine.

The country-level composite gauges for Germany and France are both in contraction territory. For France, November’s flash reading marked the first sub-50 print since February 2021. “Although France’s manufacturing sector has been in a downturn since the start of the second half of 2022, overall economic activity levels throughout this period had been propped up by continued growth in services,” Joe Hayes, a senior economist at S&P Global Market Intelligence remarked. “This vital support for the economy looks to have ended as service sector output fell for the first time in just over a year-and-a-half in November.”

Thus far, the European economy has avoided a recession — at least officially (figure below). But it’s just a matter of time. “Robert Solow famously said that the computer age was everywhere but in the productivity statistics. At the moment, we can say that the recession is everywhere except for in the GDP statistics,” ING’s Bert Colijn said Wednesday.

“While the eurozone economy still eked out positive growth in the third quarter, it seems inevitable that a recession has started in the current quarter and today’s PMI figures confirm that,” Colijn added.

It wasn’t all bad news. With moribund activity comes slower price growth or, if that’s too deterministic, we can say that a deceleration sows the seeds for disinflation. “Supply constraints are showing signs of easing, with supplier performance even improving in the region’s manufacturing heartland of Germany,” Chris Williamson, S&P Global Market Intelligence’s Chief Business Economist wrote. “Price pressures, the recent surge of which has prompted further policy tightening from the ECB, are also now showing signs of cooling, most noticeably in the manufacturing sector,” he added, before venturing a bit of optimism: “Not only should this help contain the cost of living crisis to some extent, but the brighter inflation outlook should take some pressure off the need for further aggressive policy tightening.”

Maybe. Hopefully. Because, as I’ve endeavored to make clear over the past several months, the inflation impulse in Europe is mostly beyond the ECB’s capacity to control, and even if it weren’t, they started so late that catching up is an exercise in abject futility.

By contrast, RBNZ got a relatively early start in the inflation fight. Last month was the one-year anniversary of New Zealand’s first rate hike of the current cycle, which took a turn for the aggressive Wednesday.

“Demand in the New Zealand economy has been resilient to global and domestic headwinds,” the bank said, explaining a record-large 75bps hike (figure below).

It was the ninth increase in a row. “Household spending has stayed elevated, despite high inflation, rising interest rates, falling house prices and uncertainty about the global outlook,” the bank added.

I’m not sure what a good proxy for the neutral rate in New Zealand is. I think it’s reasonable to suggest that at 4.25%, rates are restrictive (figure below), but, given inflation realities, not “sufficiently restrictive” (to employ the Fed’s new favorite talking point).

Inflation is running above 7% in New Zealand and at this point, it’s pretty obvious RBNZ intends to force a recession. They were very blunt. “The Committee agreed that the OCR needs to reach a higher level, and sooner than previously indicated, to ensure inflation returns to within its target range over the medium term,” the bank said Wednesday. There was some discussion of a full-point move at this meeting.

The new rate path is steep. RBNZ now sees rates rising to 5.5% by Q3 2023. Today’s decision stood in stark contrast to “step-downs” in Australia and Canada, although you could argue that with a record hike now on the books, and RBNZ having resigned itself to an even more strident stance, today marked “peak hawkishness.”

“Coupled with the projection of a decent chance of negative GDP in the future, the market seems willing to believe RBNZ will do whatever it takes to get inflation back to target,” SPI Asset Management’s Stephen Innes said. “Even if it means weakening the economy.”

Suffice to say our collective, shared macro nightmare isn’t over.

{kind=link}