“The bear market is not over, in our view.”

So said Goldman’s Peter Oppenheimer and Sharon Bell on Monday, in the bank’s year-ahead global equity outlook. The title was “Bear with it.”

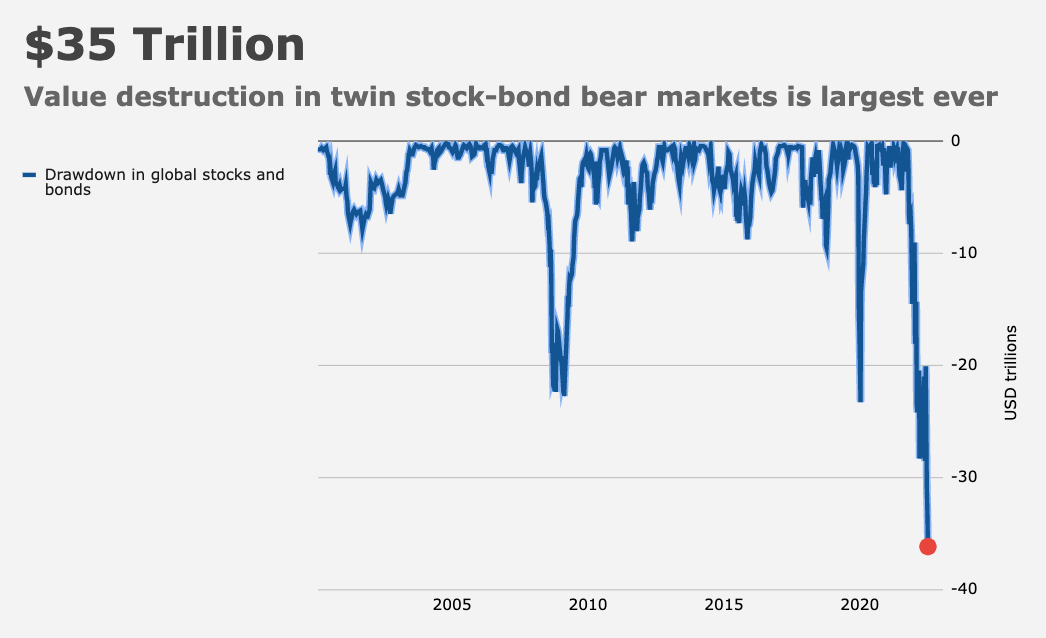

It’s safe to say investors are tired of “bearing with it” after suffering some $35 trillion in combined value destruction across equities and bonds during the first three quarters. Things recently took a turn for the better, culminating this month in a relatively favorable read on US inflation, and optimism (likely misplaced) about a relaxation of COVID controls in China.

If you ask Oppenheimer and Bell, we’re in a cyclical bear market, and that may suggest that the current rally in stocks is another false dawn.

“Renewed optimism about a slowdown in the pace of rate increases has triggered a rally that has pushed [global] equities up nearly 5% from their levels in June (prior to the last major rally), despite real interest rates in the US having increased by close to 85bps since then,” they wrote.

Goldman believes that’s incongruous. I’d generally agree, although it’s worth noting that US reals have come down ~30bps from the peaks.

For Oppenheimer and Bell, the speed of the increase in rates is more important than any specific level. I’ve emphasized that on too many occasions to count over the past year. The updated figure (above) illustrates the point. The blue shaded area is essentially the velocity of real rate rise. Again, I’d note that the impulse over the past month or so has been risk-friendly, consistent with the bounce in stocks.

In any case, Goldman frets this isn’t over. The rise in reals “has the potential to do more damage as investors are likely to increasingly focus on growth and earnings weakness,” the bank said, suggesting that the near-term path for global shares is likely to be “volatile and down before reaching a final trough in 2023.”

The figures (below) show the recent history of bear market rallies on the MSCI All-Country World gauge.

The problem with cyclical bear markets (which Goldman defines as those “driven predominately by the economic cycle and by rising interest rates”) is that although they aren’t typically as deep as “structural bear markets” (driven by the unwind of bubbles and too much private sector leverage), they tend to be annoyingly persistent, lasting longer than two years, and taking four years to fully resolve.

Such bear markets are “interspersed with rallies before they reach a final trough,” Goldman wrote, on the way to recapping the 2022 experience through the cyclical bear market lens:

Falls have come in phases interrupted by several sharp rallies. The first, in March, drove global equities up by 10% and lasted 21 days. The second was triggered by optimism of a ‘Fed pivot’ in July and pushed equities up around 13% over 30 days, and the current one has, so far, triggered a 13% rally. However, so far at least, these rallies have not lasted; more persistent inflation and hawkish central bank rhetoric, particularly in the aftermath of the Jackson Hole meetings in August, heralded another setback.

Oppenheimer and Bell went on to enumerate the factors which have driven a bullish reversal in sentiment over the past several weeks, including a downside surprise on the inflation front in the US, mild European weather and, of course, China reopening speculation.

Goldman doubts it’s sustainable. Their forecasts for US and European stocks in 2023 are less than jubilant (table below).

“We do not think the adjustment in equity markets is yet sufficient to account for the rise in interest rates and the cost of capital,” the bank said, on the way to reminding investors that headed into this year, market pricing reflected just two 25bps Fed hikes and no hikes at all from the ECB until next year. Something about the “best laid plans.”

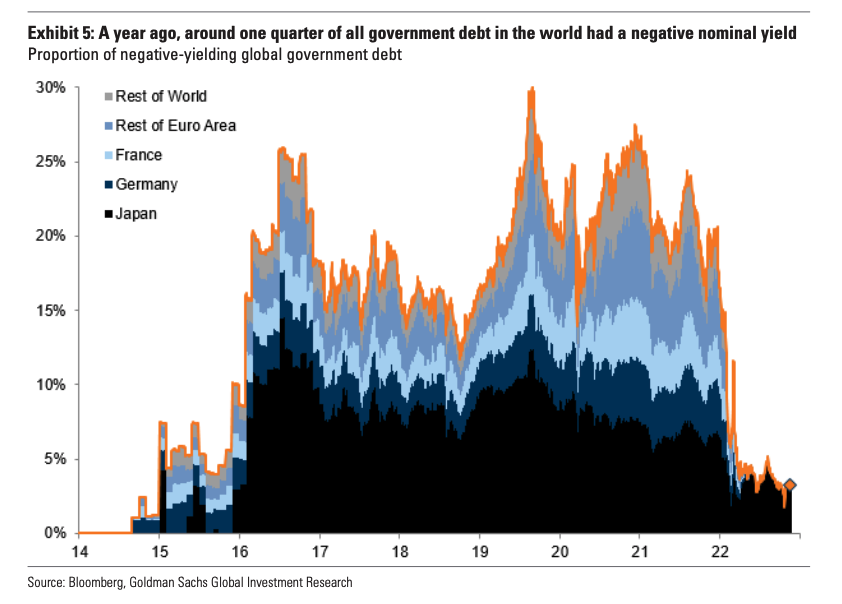

“The shift in the level of long-term interest rates is remarkable,” Oppenheimer and Bell said, flatly. This time last year, 25% of all government debt sported a negative nominal yield. Now, that figure is less than 5%.

“Even in the event there is a ‘soft landing’ in the economy interest rates may well stay higher for longer than the market is pricing,” they added. “The downside risks to equities may be moderate, but on a relative basis the hurdle rate suggests a high bar, leaving little room for a re-rating.”

{kind=link}

{kind=link}