Let’s be clear: The Fed funds rate modern markets can tolerate is almost surely lower than the funds rate consistent with bringing down inflation from current levels based on classical models.

I don’t think that’s much of a debate. It might be an unpalatable situation, and thereby difficult for some observers to countenance, but fixing this (where “this” means generationally high inflation in the real economy) isn’t as simple as Jim Bullard made it sound on Thursday, when he used modified Taylor Rules to suggest rates may need to go as high as 7%.

Maybe markets can tolerate 7% if you give them a few more months to adjust. I have no idea, and neither does anyone else. What I do know, though, is that you can’t just say “Here’s this rule, and we’re going to apply it without taking into consideration the side effects of a decade spent experimenting with free money and large-scale asset purchases.” If you do that, you will collapse markets in an almost literal sense of the term “collapse,” at which point inflation won’t be your top concern anymore.

I mentioned this on Thursday, and when I did, I referred readers to an article published last month. Allow me to quote from that article:

[T]he torrid pace of rate hikes comes on the heels of a dozen years spent in a regime defined by the pervasive deployment of leverage, and the herding of investors out the risk curve and down the quality ladder, in an increasingly desperate, globalized hunt for yield. The viability (and stability) of that regime depended entirely on central banks operating in vol-suppression mode, mostly via forward guidance. Modern market structure was built around and atop the attendant low-vol regime. Loosing the ghost of Paul Volcker into that environment is extraordinarily dangerous. The implication is that the amount of Fed tightening markets can absorb without “some kind of financially traumatic event” (as Larry Summers put it) is probably much lower than what the real economy can take without rolling over.

Researchers from the New York Fed addressed that in a recent paper, and it was (however briefly) a mainstream discussion — or as mainstream as these sorts of discussions can be.

I bring this up again because BofA’s Michael Hartnett touched on it, tangentially, in his latest note. 2022’s rate shock has been “so damaging to Wall Street asset values,” he said, but noted that “there’s been no rates shock on Main Street.”

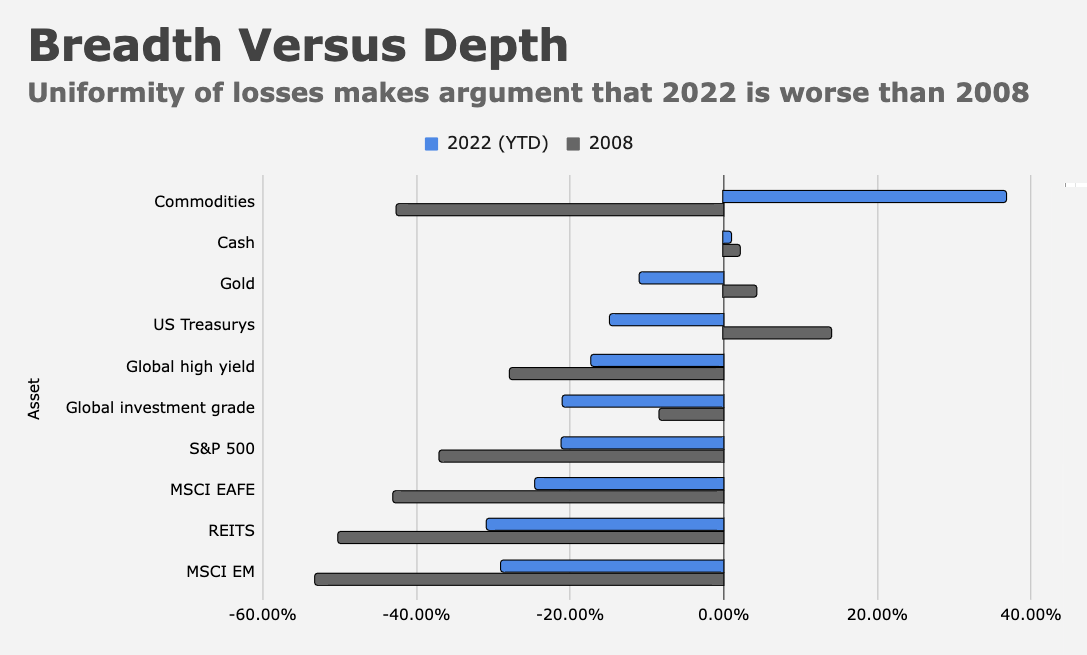

From a pure “panic” perspective, 2022 certainly doesn’t feel like 2008 on Wall Street, but the breadth of the cross-asset malaise is, for all intents and purposes, unprecedented. When you add up stocks and bonds, the depth is “impressive” too. Recall the simple figure (below).

By October, 2022 had witnessed more than $35 trillion in value destruction across global stocks and bonds. That dwarfed the losses seen in 2008.

And yet, on Main Street, the only place this is evident so far is the housing market. But even there, the huge home equity gains racked up during the pandemic bonanza afford homeowners a very large cushion against price declines.

Most readers are familiar, but just in case, don’t forget that property values in the US increased by $1 trillion or more per quarter for almost two straight years (figure below).

Even if prices start falling (and they have), there’s virtually no chance of all that being wiped away in any housing downturn. Property isn’t like stocks.

The point is: Even in the sector where 2022’s rate shock has manifested most acutely, the read-through for Main Street is primarily confined to would-be buyers and, increasingly, builders. If you own a home, and you’re not trying to sell it, you’re in good shape.

At the same time, I’d be remiss not to mention that mortgage rates fell the most since 1981 last week (figure below) amid a bond rally inspired by the cooler-than-expected October US CPI report.

That’s what I meant Thursday when I wrote that, “It’ll be interesting to see if the recent decline in yields and any attendant drop in mortgage rates helps bring buyers back to the market or whether disenchantment has thoroughly set in — my guess would be that any meaningful drop in financing costs will create a sense of FOMO among would-be buyers.”

At the same time, Americans are running up credit card debt (at twice the pace of headline inflation, by the way), but so far, delinquencies are very low, even as APRs are now near record highs. If you didn’t read “Americans Have Some Credit Card Debt,” you should. The title was deliberately understated — it was dry humor, which I should know doesn’t work in a world that struggles with nuance.

The Fed plainly doesn’t understand the extent to which market structure optimized around the acronyms (i.e., NIRP, ZIRP and LSAP) and “solved” for the dearth of yield by deploying leverage over the past decade. Note the emphasis on “the extent.” Contrary to popular belief, Fed officials aren’t bereft in the intellect department. They do get it. All of it, I’d argue. The problem isn’t that a panel of highly educated, highly accomplished people are incapable of grasping fairly simple concepts. Sure, some of the math around modern market structure might be challenging, but remember what econometricians do: They bend math for a purpose it wasn’t intended. They force math to accommodate a soft science (economics). That’s a dubious exercise, but it’s no small feat. It’s hard, mostly because it’s impossible. (That’s supposed to be funny. Laugh.)

So, no, the issue isn’t intelligence at the Fed. Rather, the issue appears to be an (admittedly inexcusable) reluctance to accept the consequences of their own actions and incorporate that acceptance into their decision making process in anything like real-time. In this case, that might go as follows. “We spent a decade in a regime that forced every steward of capital on Earth to choose between harvesting carry or going out of business, and because that’s not really a choice, everyone ended up short vol, so now that we’ve raised rates 375bps in 10 months, we have to be cognizant of the potential for market events as rates rise further.” And then, relatedly, “That’s particularly true considering that quantitative models of all kinds also optimized around a decade of artificial vol suppression, which means that if we push the envelope too far, every day will be a multi-sigma day because the distributions (and thereby the risk parameters) were constructed (and set ) based on outcomes that weren’t the result of actual price discovery.”

The Fed understands that at a conceptual level, but 8% CPI isn’t something any of them have ever had to cope with as policymakers. So, they’re going to fall back, terrified, on relatively simplistic models that say, stylized, “Inflation is ABC, so rates need to be XYZ.” The consequences of that for markets are unknowable past a certain point. We haven’t reached that point yet, but nobody knows quite where it is.

What we do know (and this is where the risk comes in) is that Fed funds at 3.75% isn’t “sufficiently restrictive” (to employ the Fed’s new favorite phrase) to bring real-economy inflation rapidly back towards target, even if raising rates that far, that fast has done wonders to crimp some asset price inflation. The Fed is scared for their credibility, and although they hear the likes of Elizabeth Warren warning on the risks of job losses, they’re more concerned, in my opinion, about the shrill cacophony of market observers and brand name pundits screaming at them to, “Forget stocks! Bludgeon inflation before it becomes entrenched in expectations and wage-setting!”

That’s probably the correct way to think about. Until it’s not. The key is to take rates as high as absolutely possible in an effort to vanquish real-economy inflation without accidentally cutting the wrong wire, where that means raising rates so far, so fast that you trigger a real credit event (as opposed to a crypto credit event) with the potential to destabilize the whole system.

Having thoroughly buried the lede, I’ll get back to Hartnett’s allusion to all of this. “Wall Street belie[ves] the ‘Fed always blinks,’ ‘stocks always go up,’ and ‘tech always leads stocks up,'” he said, before suggesting that while those deeply held convictions were “challenged” in 2022, they were “by no means vanquished.” So, with markets still inclined to doubt the Fed’s resolve, and Main Street yet to feel the brunt of the rate hikes already delivered, a pivot at the February FOMC meeting or even the May gathering, would be a “big mistake,” according to Hartnett.

Instead, the Fed could thread the needle by pivoting in June or July, “just before $1.6 trillion of US corporate refi begins” and just “after rates bite Main Street.” Around the same time, earnings will be cracking “ironically because inflation falls” and the unemployment rate will be “up big,” Hartnett went on to suggest. “That’s your credible big bull trade,” he added. BofA says “bonds for the first half of 2023 and stocks for the back half.”

Of course, needles are rarely threaded by policymakers. This does seem doable. But it’s not immediately obvious where the individual land mines are (again, other than crypto). Yes, the entire post-financial crisis market structure is one big powder keg, but it’ll adjust over time, as price discovery reasserts itself gradually, and market participants become accustomed to volatility again. The caveat is that a dearth of cross-asset liquidity is a big risk to that adjustment process. If you’re wondering “What could go wrong?”, so to speak, the near implosion of the UK LDI complex last month was the quintessential example. Just as the price insensitive buyer for gilts (the Bank of England) was poised to become an active seller, the government delivered a fiscal plan that sparked a selloff into an illiquid market. The attendant yield spike blew through risk thresholds, triggering collateral calls and a liquidity crisis. That’s how quickly it can go off the rails.

Notwithstanding many (generally viable) arguments about pipeline disinflation (based on leading indicators), it’s still difficult from a kind of finger-in-the-air perspective, to countenance the idea that 3.75% Fed funds is sufficient to durably suppress inflation in the US economy given lingering pent-up demand, a still acute labor shortage and, more anecdotally, the simple fact that it’s the US economy, which means it’s pretty hard to kill once it’s juiced up and running.

Still, as I suggested in a comment Thursday, I don’t think Fed funds 8% (or 7%) is the answer. It’s probably more akin to what Howard Marks said this week, when he told investors in Singapore (and, later, Bloomberg, in an interview) that rates may stay near 5% for the next five to 10 years.

If that’s the case, the bigger question going forward isn’t “Where’s the financial stability real interest rate?” or “How large is the gap between the natural real interest rate and the financial stability real interest rate?”, but rather “Can the financial system cope with a prolonged normalization of policy rates?”

{kind=link}

Your dry humor is appreciated here, H.

Was it my imagination or was there originally a picture of an unlabeled wire. Systems are reliable, the wires that might blow things up are labelled. Jalopies on the other hand get patched until death and they do die eventually. Yet a jalopy can run for a long long time. Can this financial jalopy cope with a new minimum speed limit? Hell if i know i am still trying to label the components under the hood.

There was. I’m very obsessive about the banner images, though. If I don’t like the way it looks or the way it fits with the others or even the proportions, I’ll stop what I’m doing and make a new one.

unlabeled wires to rumors of wires.

It’s ‘hot off the wire’!

Bullard already knows what he wants to break…….labor. Simple. In tandem with Usery interest rates he may get more than he bargains for.

Canadian (Toronto/Vancouver) home owners are in shocked. With average home price north of 1 million, and mortgage at 600K, what used to be $500 per month of interest expense at 1% is fast becoming $3000 per month at 6% interest rate. This is average, not even including paying down the principle, while some in even more distress with 1M+ mortgage or multiple properties with negative cash flow.

“Housing price always goes up, don’t worry about negative cash flow!” So they say.

We need a bigger housing bubble to bail them out.

Professor Taylor himself has cautioned that his model assumes some degree of economic stability. It can be disrupted by an outside shock. That’s from the author of the model.

Don’t Covid and Ukraine qualify as exogenous shocks? If so, why is the model even being cited as the basis for determining policies which can have such an impact on all but the top 2%?

Many of these models look good in the ivory tower but fall way short in real life. EMH, Taylor rule, Phillips curve, perfect competition model to name a few are plain bunk in anything but the most ideal circumstances. Life in the real world is a lot messier….

I’d be shocked if we get 5% rates for anything like 5 to 10 years unless Marks expects frequent ups and downs. As you’ve said repeatedly, the current market is built around the acronyms you listed. Something will almost certainly break in the next year or two that’ll impact main street. I think what’s more likely is that we get whiplash from rates rapidly rising and falling as the Fed tries to manage both the downside risks to the economy due to shocks vs downside risks due to inflation.

Although I’m bullish on big tech, small tech will need to be opportunistic about when they raise money. A lot of smaller tech companies are still burning a lot of cash and their runway won’t last forever. The tide is going out on the so-called unicorns.

He expects just that. Look what business he’s in. 🙂

Ha, guess I should’ve clicked the link.

In a CNBC article from Oct. 2021, the wealthiest 10% of American households own 89% of all US stocks and which underlines the market’s role in wealth inequality.

So while the likes of Jeff Bezos, Bill Gates and Elon Musk have seen their net worth drop dramatically, they are not worried about paying 10% more for goods and services. While 2022 has been painful, they (and all us other smaller investors who rode out the COVID storm) have not lost all the major gains in the stock market since March 2020.

These factors may explain in part why the stock market remains so resilient in face of such heavy losses in 2022. This may (or may not) change quickly however in 2023 with a recession. Wish i had that crystal ball !

Another question is, will divided government result in inaction or brinksmanship that accelerates a crisis already in motion?