There’s no shortage of US data for investors to ponder in the new week, but if Sunday’s headlines were any indication, it’ll all take a backseat to Sam Bankman-Fried news.

On a day when Democrats, against the odds, clinched control of the Senate, consigning the 2022 US midterm elections to a place in the history books, the top story on Bloomberg’s homepage was about Solana. If your reaction is “What’s Solana?” I’d say “Something that’s not as important as control of the US Senate.”

To be sure, I know what Solana is. In fact, I still own some Solana, a sad remnant of my jaunt through the cryptoverse earlier this year. Relatedly, I also own some Serum, a token that lives on the Solana blockchain.

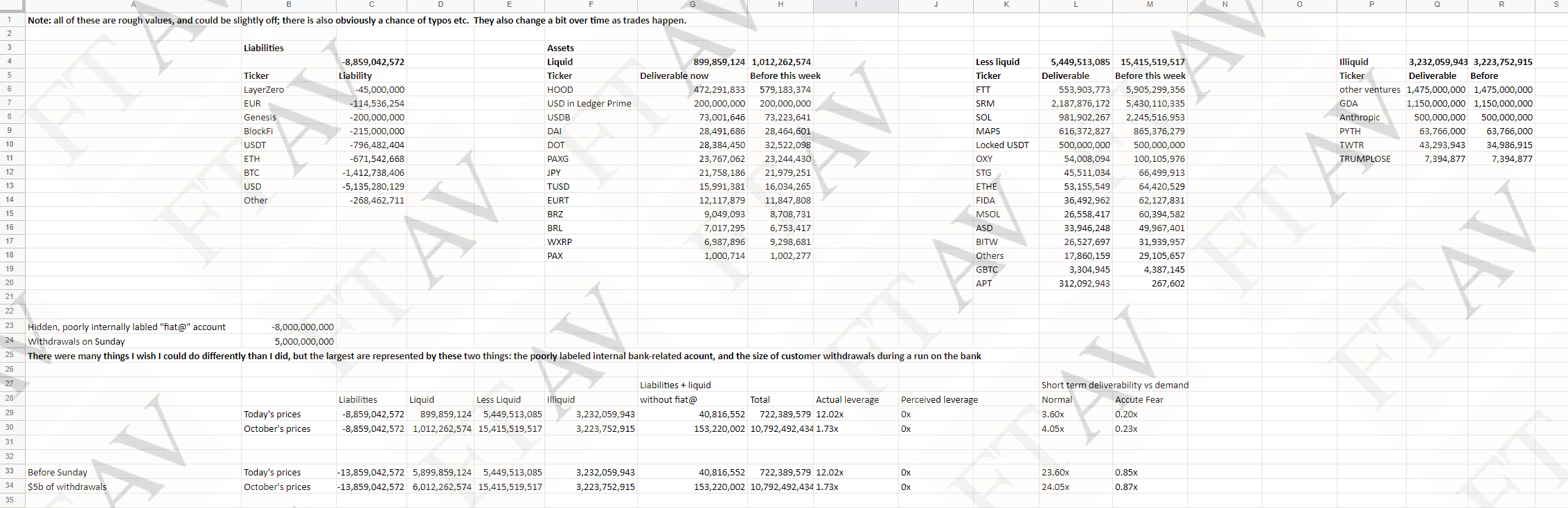

I mention that because, according to FT, Bankman-Fried’s FTX counted Serum as its most valuable asset on a very unbalanced balance sheet. FTX carried its Serum tokens at a ~$2.2 billion valuation, which struck some observers as odd considering the coin has never boasted a market cap above $1.2 billion, according to CoinMarketCap.com. As of Sunday, its market cap was around $67 million, with an “m.” FT Alphaville (which, based on my experience and conversations, professional investors haven’t enjoyed in at least a decade) weighed in, and much like a lot of what shows up on the blog, their description of Serum as “obscure” betrayed a lack of hands-on familiarity with the market about which they were pontificating. As a former friend once put it to me, of Alphaville, “none of those people have ever traded any of this stuff.” I don’t know whether that was strictly accurate when it comes to traditional markets, but I’m confident that nobody at FT Alphaville has much experience with Serum. Yes, it’s obscure to the masses. But it’s not obscure to anyone familiar with Solana, and Solana isn’t obscure to anyone who’s actually familiar with crypto.

The fact that I just inadvertently slipped down the Bankman-Fried rabbit hole speaks to how easy it is to get sidetracked by the spectacle of a five-alarm blaze at a casino that doubled as a fireworks warehouse and tripled as a storage facility for high explosives. And the fact that I simultaneously lapsed into a brief Solana tangent suggests I shouldn’t cast aspersions at Bloomberg for doing the same.

With that, let me steer us back onto the highway, lest we should become part of the accident we’re ogling. PPI is on deck this week stateside, and while my guess is that the monumental stock and bond rally triggered by October’s cooler-than-anticipated CPI report means incremental improvement in the inflation data is already in the price (and then some), it’s certainly possible that any indication from factory-gate prices that pipeline inflation is waning could bolster risk sentiment anew. But, again, I want to emphasize that after last week’s historic tech rally and concurrent dollar plunge, I’d be inclined to think this week will find traders adopting a more level-headed approach.

Consensus is looking for 0.5% from the MoM headline print (figure above). Core is seen at 0.4%.

On Wednesday, traders will get a look at retail sales for October. This is the same story month after month. The official talking point is that the Fed wants to “moderate demand” so that it “better aligns with supply.” The unofficial version goes something like this. The Fed wants Americans to stop burning through their pandemic savings cushions on superfluous discretionary expenditures so that companies stop believing they can readily pass along elevated wages as higher consumer prices. Once corporates are compelled to absorb the hit from higher input costs in the form of lower margins, they’ll scale back wage increases and hiring plans, short circuiting the wage-price spiral and closing the gap between labor supply and demand.

Any evidence that Americans are continuing to spend undeterred by inflation and inconsistent with what, according to the University of Michigan’s survey, are very poor attitudes about the economy, would argue for Fed obstinance. Of course, at this point, obstinance just means a determination to reach higher on the terminal rate and hold it longer once it’s achieved.

Consensus is looking for 0.9% from the headline retail sales print (figure above).

Obviously, October retail sales will be contextualized via the holiday shopping season and what many expect to be pervasive discounting to clear an inventory overhang at America’s largest retailers. In addition, analysts will view the data through the lens of Q4 GDP. That is: We know how the consumer said she was feeling last month and early this month (i.e., bad), but if somber responses to survey questions don’t translate into retrenchment, then estimates of the personal consumption impulse in this year’s final quarter will remain buoyant.

Also on the docket: Key housing data, including NAHB on Wednesday, starts on Thursday and existing home sales on Friday. Regular readers know how that’s likely to play out. NAHB will be lackluster, and I’ll join the nation’s homebuilders in lamenting the ongoing housing recession. Starts and permits will be mixed, and I’ll meander through a recap of the data doing my absolute best to find the bad news while confining any silver linings to footnotes. Then, existing home sales will offer a new opportunity to declare the US housing bubble burst. I’ll indulge accordingly. Some of you will agree, others will insist that a lack of inventory will keep home prices elevated irrespective of the slowdown. (Who’s excited?!)

Finally, the Empire and Philly Fed surveys will garner attention if, and only if, there’s a meaningful surprise, and Fed speakers are lined up around the corner. Traders will hear from Williams, Harker, Barr, Bullard, Mester, Jefferson and Kashkari.

{kind=link}

“Let me steer us back onto the highway…” Love it.

I am actually looking very forward to hearing what Bullard has to say and how he says it.

H-Man, Sam’s tale of woe is just unfolding, so this will take a while before it fades in mainstream media. But you already know that. The Binance role in this fiasco may be illuminating.

I met with a member of the Solana executive team in ~2018, when they had roughly 20 people. Its pretty funny looking back on our discussion and what they were working on at the time. “Throwing stuff at the wall” is one quote I recall.

I’m very interested in all of the housing data H, at some point in the relatively near future, I need to buy some real estate!