I doubt this needs further emphasis, but just in case: Rates are the sponsor of the ongoing cross-asset malaise in 2022, a year during which economists, traders and investors of all shapes and sizes, have been compelled to ponder the uncomfortable prospect that the vaunted “Great Moderation” and associated market dynamics were an accidental anomaly, not a new normal.

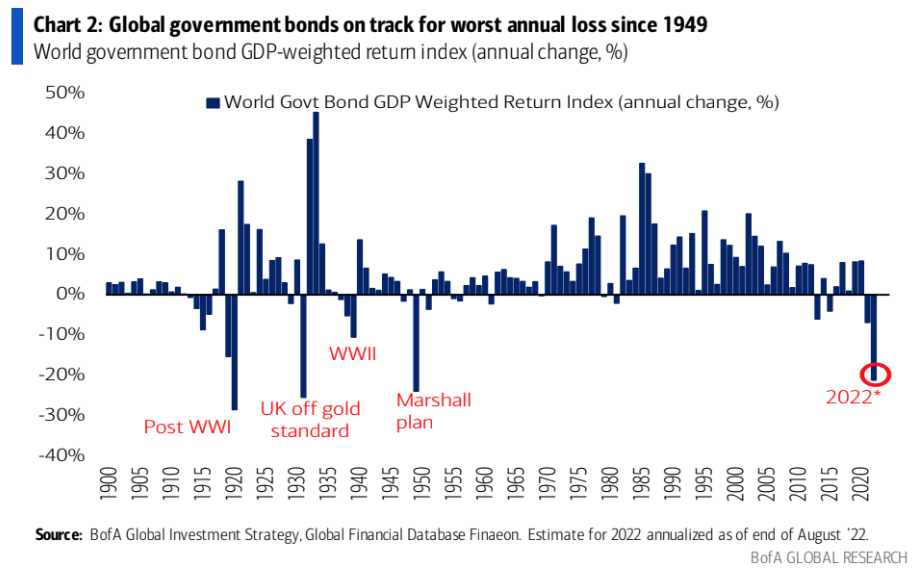

If that’s true, then much of what we thought we knew is false. For example, it wasn’t central bank independence and inflation-targeting which kept price growth predictable and staid in developed markets. Rather, it was fortuitous macro circumstances. When our luck ran out on the macro front beginning in 2020, inflation promptly rose, central banks were exposed as powerless to stop it and a four-decade-long bond bull market quickly gave way to what, on at least one index, is on track to be the fourth worst annual rout in more than 120 years.

Because markets as we’ve come to know them over the past two or more decades were constructed atop and around ever lower risk-free rates and artificially suppressed volatility, probability distributions reflect a constellation of outcomes which aren’t representative of free market dynamics. So, the normal distribution is even less reliable than it would be already, and as we saw with the UK pension debacle, the associated risk parameters are therefore vulnerable not just to being breached, but to being blown through entirely, which in turn risks systemic crises given the amount of leverage deployed.

In their Q4 volatility outlook, SocGen’s Vincent Cassot and Jitesh Kumar delivered a concise assessment of the situation, which I’ve been meaning to highlight.

“We think it would not be an exaggeration to say we are in a bond market crisis,” they wrote, noting that “mishaps are more likely when central banks are determined to fit in years of policy tightening within months.”

That would be true in any era, but it’s particularly important today given the length of time spent in what Deutsche Bank’s Aleksandar Kocic described as the “state of exception.” As I put it last week, the consequences of a hyperactive Fed go beyond what would normally be associated with tightening, not just because the pace of rate hikes exceeds previous cycles, but also because the prolonged period of inactivity encouraged and facilitated behavior conducive to ruin in the event a macro shift forced a policy regime change.

Cassot and Kumar underscored the point. “Financial markets are not meant to handle so much volatility in the risk-free rate, especially after more than a decade of relative stagnation and low-interest-rate policy, which has led to a build-up of leverage in unpredictable places.”

The figure on the left (below) is remarkable. 2022 is totally anomalous for the drawdown in bonds, and when considered with the simultaneous selloff in equities, the weekly outcomes trace an entirely new path.

The figure on the right (above) shows the extent of the rates vol deviation from what we came to regard as “normal” over the past decade.

Elaborating on the interplay between large amounts of embedded leverage and the fastest pace of rate hikes in modern history, Cassot and Kumar said, “This immediately calls to mind the Merton ‘distance to default,’ which narrows with higher leverage and higher volatility.”

“If leverage is water for the market, rates volatility is proving to be its ‘ice-nine,'” they added.

{kind=link}

Not hearing much about mmt these days….

I’m exhausted with this ostensible quip. Somebody uses it seemingly every other day. If we’re supposed to take it literally, then the rejoinder is “You’re not listening very hard.” The MMT discussion is everywhere, Stephanie Kelton has a record number of social media followers, her Substack seems to be thriving, you can find the debate going on all day, every day on Twitter and although Bloomberg’s story count feature and Google Trends probably show a decline in “MMT” interest over the last two years, that’s only because it was the hottest topic in the macro universe from mid-2020 to early 2021, which means it couldn’t possible have become any more ubiquitous.

But far more importantly, MMT isn’t a “theory” or a “concept” or an “idea” or really a discussion. It just is. Governments in advanced economies spend first and then pretend to pay for (some of it) later by taxing and borrowing. The spending comes first. All spending is unfunded in terms of sequencing. Period. Anybody who tells you different is either lying or doesn’t know what they’re talking about.

Beyond that, I’m tired of pretending there’s anything “new” or “modern” about MMT. I’ve avoided saying this for the longest time because Kelton seems like a very genuine, well-meaning, kind individual (which is a lot more than I can say for myself at certain points in my life), but the fact is, the exorcism of the taboo around deficit spending (and fiscal stimulus when the government is in the proverbial red) dates back to the New Economics, as does the idea of fiscal-monetary partnerships, employment targeting and the explicit repudiation of the purported link between deficits and inflation. Around the same time, economists began to dispense with the idea that government debt is a “burden” on future generations. Kelton was born in 1969. These revelations are (at least) 8 years older than she is. That’s of course not to say that there’s broad-based buy-in for all of those ideas, but really there is. If there wasn’t, then you wouldn’t see both political parties in the US summarily dismissing budget concerns at the first opportunity whenever it’s politically convenient for them. No Republican would seriously consider turning down money for their constituents let alone jeopardizing their own position and power out of respect for the deficit or the nation’s “grandchildren.” Nobody has actually believed any of those canards since Eisenhower.

All of that to say that 1) there’s no shortage of MMT discussions, 2) MMT isn’t a “theory,” it just is and 3) the last time the basic underlying tenets could be aptly described as “new” or “modern” was when Kennedy was still alive.

The questions we should be asking right now are: What does the UK’s recent crisis say about the limits of MMT frameworks for developed nations which issue reserve currencies, but not the reserve currency (Tangentially: What did we learn about how the unwind of leveraged positions that depend on low bond yields can torpedo DM fiscal agendas and how can we address that so that fiscal policy isn’t beholden to unrelated financial engineering?) And how should the US be leveraging its status as the reserve currency issuer to increase productive capacity and implement industrial policy to help alleviate domestic inflation and win what increasingly looks like an economic war between the West and a coalition of autocratic nations bent on establishing an alternative system?

Furthermore, Kelton has always made it abundantly clear that the constrained variable in MMT is inflation. The theory doesn’t say inflation never goes up no matter how much you spend. That would be ridiculous on its face. It says you can spend as long as there’s unutilized capacity in the system with inflation as the primary constraint.

For someone like Larry Summers to come out in early 2021 and say we have to stop spending or it will drive inflation is not at all inconsistent with MMT. You can even say he was arguing that from within a fully embraced MMT framework. (I’m not saying he embraces MMT, just that it would not be inconsistent).

Fantastic way to describe what so many others have failed to grasp, how to define MMT. I’ve more less said the same thing when discussing such (with less succinct eloquence). I once debated a pompous PhD Prof who also authors on SA. He’s old. He thinks Reaganomics is economics, meaning the only viable version of economics. I had to explain to him that Reaganomics is a version of MMT, it’s just that instead of disturbing the benefits of MMT to as many as possible (as most current adherents support) Reaganomics is designed to see the benefit goes to as few economic participants as possible. His cognitive dissonance kicked in and he got cranky.

That last sentence could be paired and distributed with: make the national debt a matter of national security. Defeat the commies etc… Then again, we are probably some possible distance away from some type of autocracy and civil war attempt that might collapse our reserve status altogether.

Real enabler of DM’s fiscal “largesse” is that of the current American power hegemony, which is backed up ultimately by the American military.

Got you going huh? I was attempting to highlight the fact that markets eventually make hash out of almost any economic model or paradigm. It happens over time, as economic models describe human behavior in groups which adapt and change. Sometimes the models even make a comeback, such as keynesian theory in 2007-13. It isn’t that mmt is a bad model. It is just that it can be overtaken by change or events. But models/paradigms are always an approximation or description of the real world. Sometimes they fall short.

Also, Kelton is pretty damn sharp. Here’s a great example from Friday morning: https://twitter.com/StephanieKelton/status/1583443368251510785

That packs a lot into a single tweet. And she didn’t even have to write anything. She did it all with a meme, a CNBC screenshot and a smirk emoji.

There is no question about kelton’s intelligence. It’s just about the model working now.

“How should the US be leveraging its status as the reserve currency issuer to increase productive capacity and implement industrial policy to help alleviate domestic inflation and win what increasingly looks like an economic war between the West and a coalition of autocratic nations bent on establishing an alternative system?”

Those are the right questions. And the GOP’s answer, should the midterms give it control of Congress, is: Cut taxes on the wealthy; shrink the social safety net.

I’d like to personally thank RIA for inspiring “H” (scare quotes are there for a reason) to write one of his best articles…..in a comment!

love the ice 9 reference! apropos

Credit to SocGen’s derivatives team on that. I was impressed myself.

Ice Nine is the contagion. Confidence is the ingredient.