Plainly, something was “amiss” in equities on Thursday, although I’m not sure “amiss” is the right word.

What should’ve been another downbeat day based on a hotter-than-expected September CPI report in the US morphed into a raucous affair on Wall Street, where stocks were sharply higher, up some 3% into the close.

The S&P enjoyed one of its best days of the year after staging a 194-point reversal from a fresh bear market low (figure below).

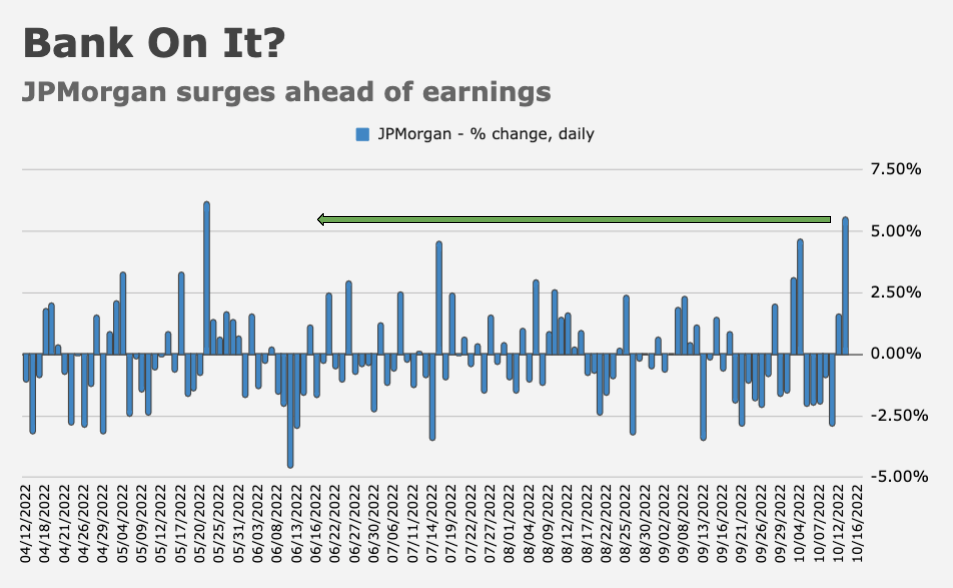

The Dow’s turnaround from the lows on Thursday was some 1,300 points. JPMorgan rose 6% ahead of earnings.

Global equities and rates were heavily shorted, and thus prime for a squeeze. There was some discussion of technical support and associated programmatic buying.

Profit-taking on downside expressions and an abundance of dry kindling certainly could’ve made for a combustible setup. Nomura’s Charlie McElligott on Wednesday called the market “ripe for painful rips higher” given “persistent short gamma with extreme negative delta” in US equities index and ETFs options positioning.

I’d note that any account of Thursday’s session that doesn’t mention the potential for a fiscal fold in the UK (i.e., a possible Liz Truss “blink”) is incomplete. Sterling surged 2% on the day (figure below).

That’s a big move. It was accompanied by a sharp reversal (lower) for the dollar, which in turn triggered large buy programs around the time the S&P retraced half the pandemic surge. According to traders who spoke to Bloomberg’s Vincent Cignarella, someone was “sitting on the bid in S&P futures in and around the 3,670 level with what looked like size.”

I’d emphasize that the rally in UK rates was important. Gilts are the current locus of concern vis-à-vis the global macro “breakage” narrative.

“The moderation of selling pressure on gilts and prospect for less aggressive deficit expansion in London help allay worries on the integrity of the UK financial system, although if we’ve learned anything since the initial mini-budget was announced, it’s that there’s certainly potential for a renewed period of bearishness in gilts,” BMO’s Ben Jeffery and Ian Lyngen wrote.

In equities, underpositioning is a big factor. “Low nets and high cash are de-facto ‘shorts’,” McElligott remarked earlier this week, in the course of suggesting that if there was a policy U-turn in the UK, “a relief rally on the potential ‘killing-off’ of the budget plan risks setting off substantial buy-to-cover flows in bond and rates shorts.” Certainly, there was some of that in play on Thursday.

One of the biggest risks going forward was ongoing margin calls and forced selling in the UK pension complex, where everything that isn’t tied down is at risk of being sold to raise cash, including stocks. A policy U-turn from Truss would help immensely to the extent it calms the UK rates complex and obviates the need for the market to speculate on whether the BoE “means it or not” (if you will) when it comes to ending the bank’s temporary emergency bond-buying.

It’s also possible that headlines suggesting the Kremlin may be open to “negotiations” with Ukraine helped risk assets. In remarks to Izvestia, Dmitry Peskov said that although Vladimir Putin’s “special military operation continues… we have repeatedly reiterated that we remain open to negotiations to achieve our objectives.” Still, Peskov called the West too “hostile,” and played down the idea of talks in the near future.

It’d be a mistake to read too much (or anything at all) into Thursday’s manic session. About all one can say is that those expecting fireworks on CPI day weren’t disappointed, even as those hoping for signs of inflation relief were.

“Thursday’s session lived up to the expectation that the September inflation data would provide ample tradable opportunities,” BMO’s Jeffery and Lyngen remarked, employing their signature understated cadence.

{kind=link}

{kind=link}

Thems with shorts is the ones got torched.

This all shows how fragile and illiquid the markets are at present. A further rally cannot be discounted. So far it still looks like a bear market rally though.

“This all shows how fragile…” – maybe also indicating that “future position and momentum can not be predicted by initial conditions”? 🙂

The more I travel, the less worried I become about “just staying long US equities” (even after living through 2022 YTD). Obviously, I am not a trader at heart.

A reworking of “the way the world works” that could potentially be a significant threat to US supremacy will likely not occur anytime soon- due to what is happening at individual country levels- where most developing countries will not be able to achieve their full potential due to a lethal and/or missing healthy combination of demographics, “rule of law” and property rights; combined with systemic and high levels of internal corruption (which make the level of existing level of corruption in the US seem relatively mild). Having said that: if I could make an immediate change in the US, it would be for the US to incorporate critical thinking and analysis into our K-12 curriculum (see Denmark),

+1 When did we decide to stop teaching critical thinking in US schools? We’re paying for it now with a large portion of the population unable to tell fact from fiction. God help us if they get their hands on the steering wheel again. They’ll take us right over the cliff believing Newton and Einstein were conspiracy actors.

To be fair, I doubt that the teaching of critical thinking skills were any better in the past. I think it has more to do with a lack of ability for people to understand the complexities of the modern world combined with much more powerful tools of manipulation as it is the teaching of critical thinking skills. You could have just as easily duped US citizens 100 years ago as you could today.

H-Man, The flip was due to the mother of all short squeezes. The Dow was up 200 to 300 going into the print, when it hit, the market flipped down to 400 or 500 but those losses were paring down going into the open. The market continued a slow slide down ending in positive territory but at the open every short was in the money. So God knows how much of this was short covering.

I thought in an article a couple of weeks ago when possible SP targets were discussed, depending on what price times earnings were, we could see 3700, 3500 or the most pessimistic was 3300. Well we blew by 3700 and hit 3500. I suppose we will see more downward revisions to the 3000 range. I was very disappointed that I was in a meeting so I couldn’t trade at the open.

Of the two ways to avert Gilt Armaggedon, Truss caving seems less “market friendly” than BOE caving. In a few weeks, investors will be glumly watching BOE hiking and selling.

I think a hot CPI was mostly expected after a hot PPI, and being heavily short into the start of earnings season is risky, since expectations are pretty negative there too, plus no imminent UK implosion, so lots of covering.

a day ago. this article was needed a day ago