For those weary of war and macro doomsaying, the week ahead will be an arduous affair.

In addition to hand-wringing over what’s expected to be another depressing US inflation report, market participants will be inundated with headlines from the first in-person World Bank-IMF meetings since the onset of the pandemic, held in Washington this week.

The IMF is poised to cut its growth outlook, according to Kristalina Georgieva, who last week suggested the global economy could be left staring at $4 trillion in lost output over the next several years, which she called a “massive setback.”

“Last October, we projected a strong recovery from the depths of the COVID crisis [a]nd most economists, including at the IMF, thought the recovery would continue, and inflation would quickly subside, largely because we expected vaccines would help tame supply side disruptions and allow production to rebound,” she said, in an address at Georgetown. “But this is not what happened. Multiple shocks, among them a senseless war, changed the economic picture completely. Far from being transitory, inflation has become more persistent.”

That’s the short version. You’ll be treated to the long version from the IMF on Tuesday. If the Fund’s new outlook doesn’t sate your appetite for dour prognosticating, don’t fret. Because for the next five days, markets will hear from anyone who’s anybody, and even a handful of relative nobodies, as officials gathered in the US capital (recently the site of a failed coup) ponder the most uncertain, perilous macro environment in living memory. In the same remarks mentioned above, Georgieva described a “fundamental shift in the global economy”:

From a world of relative predictability — with a rules-based framework for international economic cooperation, low interest rates and low inflation to a world with more fragility — greater uncertainty, higher economic volatility, geopolitical confrontations, and more frequent and devastating natural disasters — a world in which any country can be thrown off course more easily and more often.

What can you say? Buy a bunker, I guess. Policymakers, Georgieva suggested, need to “regroup and rethink.” That’s what they’ll try to do this week, only not in a bunker. Not yet. That comes three months from now, after Vladimir Putin deploys a tactical nuclear weapon near the frontlines in Ukraine, forcing NATO to chase 100,000 poorly-trained, underfed, thoroughly inebriated Russian conscripts back across the border. I’m just kidding. I hope.

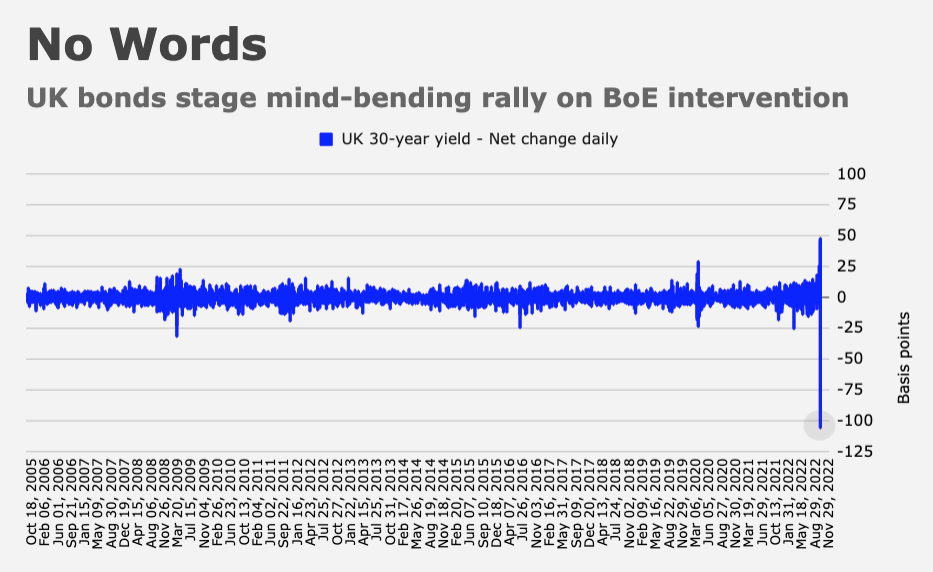

Some attendees in D.C. may lobby US officials for a reprieve from the mounting risks associated with ever higher US interest rates and an ever stronger dollar. If Fed officials’ public statements are to be believed, such pleas will fall on mostly deaf ears. I don’t believe Fed officials’ public statements, though. I think the Fed is brave now because nothing’s gone too terribly wrong, with the exception of the meltdown in the UK bond market, which the Bank of England managed to contain. But long-dated gilt yields rose every session except one following the historic rally triggered by the BoE’s intervention. On Wednesday, the bank’s Financial Policy Committee will release an account of an October meeting. I’ve argued the vigilantes will be back for gilts. It’s just a matter of time.

Markets will also be keen on any remarks from Haruhiko Kuroda and Japanese Finance Minister Shunichi Suzuki, both of whom will be in attendance in Washington. It’s not clear what next steps are in the event the yen decides to stop behaving. It seems very likely that low-key intervention is ongoing.

It’s worth noting that the par value of Treasurys held in custody at the Fed dropped almost $70 billion over the past two weeks, and more than $80 billion over four weeks (figure below). It was the largest four-week drop since the panicked flight to cash in and around the worst weeks of the pandemic crash.

Wrightson ICAP’s Lou Crandall suggested central banks are selling Treasurys out of an abundance of caution. It’s a new “dash for USD cash,” he posited.

Meanwhile, Mohamed El-Erian made a cameo on CBS’s “Face The Nation” Sunday. He was — and I’m going to choose my words more generously when it comes to El-Erian going forward because as it turns out, he’s a nice enough guy — direct.

The Fed, El-Erian chided, has “made two big mistakes that are going to go down in the history books.” He continued:

One is mischaracterizing inflation as ‘transitory.’ By that, they meant it’s temporary, it’s reversible, don’t worry about it. That was mistake number one. And then mistake number two, when they finally recognized that inflation was persistent and high, they didn’t act. They didn’t act in a meaningful way. And as a result, we risk mistake number three, which is by not easing the foot of the accelerator last year, they are slamming on the brakes this year, which would tip us into recession. So, yes, unfortunately, this will go down as a big policy error by the Federal Reserve. That is the cost of a Federal Reserve being late. Not only does it have to overcome inflation, but it has to restore its credibility. So, yes, I fear that we risk a very high probability of a damaging recession that was totally avoidable.

El-Erian, like Larry Summers, has been mostly vindicated by this year’s unfortunate macro developments, although I’d argue luck played a role. The war in Ukraine unquestionably exacerbated and prolonged the inflation impulse, which in turn exacerbated and prolonged the Fed’s credibility crisis, necessitating Jerome Powell’s Volckerian pivot. The rapidity of subsequent and future Fed hikes risks a severe downturn, a financial “event” or both.

And that brings us full circle. Commenting last week on the risk of a market meltdown, the IMF’s Georgieva warned that financial stability risks are growing. “Rapid and disorderly repricing of assets could be amplified by pre-existing vulnerabilities, including high sovereign debt and concerns over liquidity in key segments of the financial markets,” she cautioned. “It is more likely to get worse than to get better.”

{kind=link}

This time next year we will be at the bottom looking up in my view. Central banks shouldn’t be killing the economy and russia/Ukraine will be in the rear view mirror. By late 2024 covid will also be in the past, and 2023 will see us better on covid. Even if congress flips donald trump is going to be old news and will be damaged goods.

I truly hope you are correct, but I can easily envision a world a year from now where excessive monetary tightening has resulted in a severe global recession or a depression, with no hope of help from fiscal in the US under a Republican controlled house, civil unrest increasingly common in both DM and EM, a continuous energy crisis and may be even a protracted war in Ukraine. In that reality Trump is not damaged goods, he would thrive and sell his bag of lies to enough Americans suffering from real economic hardship, to manage a second term and another chance at destroying this country.

Not to fear, the US is quite adept at running a deficit budget under any/all political party configuration:

https://www.usgovernmentspending.com/include/usgs_chart4p04.png

Hopefully I pasted this correctly- it is a chart of the annual US federal deficit as a percentage of GDP since 1900.

“What can you say? Buy a bunker, I guess.”

“I would not rule out the chance to preserve a nucleus of human specimens. It would be quite easy…heh, heh…at the bottom of ah…some of our deeper mine shafts. Radioactivity would never penetrate a mine some thousands of feet deep, and in a matter of weeks, sufficient improvements in dwelling space could easily be provided.”

“I think the Fed is brave now because nothing’s gone too terribly wrong, with the exception of the meltdown in the UK bond market, which the Bank of England managed to contain.”

Brexit is the primary underlying cause for the inflation, GBP/USD decline and other UK problems; “short bus Truss” and her errors were just a first trigger. Did the BOE really contain or just delay a gilt crisis? “It’s just a matter of time.” Okay. What about a (cost of) food crisis for ordinary UK citizens?

“I fear that we risk a very high probability of a damaging recession that was totally avoidable.”

Is it avoidable? Really? I do not agree.

El-Erian: “Not only does it have to overcome inflation, but it has to restore its credibility.”

Most seem to agree w/ El-Erian; the Fed needs to restore its credibility. But how does making a new, easily recognized mistake–by “slamming on the brakes”–restore credibility after screwing up so publicly twice (“transitory” and failing to act in a timely way)?

If I told my parents I’d regain their trust by doing something as dumb (or worse) than my first screw-up, they’d have accused me of being on drugs (even before those days began). Powell & Co are novice market traders trying to correct their first blunder by doing the opposite “harder.” When it’s dark and the roads are slick, slow down and don’t overcorrect a slide.

Competence should be the Fed’s #1 priority imho… confidence, ie public trust, and credibility, which has largely been a function of paid talking heads would then all fall in line…Competence…

Every time the word ‘pivot’ is uttered markets take off, commodities soar, financial conditions loosen. The Fed HAS to overshoot so that when they relent we aren’t dealing with $130 oil and renewed inflationary pressures.

Yes and no ; even the Fed has tools other than the interest rates.

They could enforce higher reserves or greater quality of capital controls i.e. forcing further deleveraging across financial actors. And, while that’s not exactly their purview, they could talk to the Treasury and the government about using fiscal tools i.e. higher taxes on the rich, as a way to cool off assets’ prices.

El-Erian was once a smart fellow making a fortune for the endowment he managed, and later getting a transitory result at Pimco. That’s all over so now he makes his living as a professional critic. It would be nice if he and Summers and their collective cronies would supply us with precise directions on how to remedy the big historical error they have found and what they are willing to put on the line in case they are also “wrong.” I would argue no one knows anything about this situation so maybe it’s time for the pundits to take a break. By the way, as someone noted today, the Fed might well have acted sooner if only the administration hadn’t screwed around with Powell’s reappointment.

Mr. Lucky — it wasn’t the “Administration” that delayed on Powell. The Republicans on the Senate Banking Committee boycotted the vote holding up several Fed nominations as they sweated out Sarah Bloom Raskin for several months.

The title of a Guardian opinion piece by John Harris is “Britain is slowly waking up to the truth: Brexit has left us poorer, adrift and alone.” John Harris is a Guardian columnist, who writes on politics and other topics. I suggest you read the article. Germany, Italy, France … and the UK will solve the energy problem in a few years. Nobody (in the West) can solve the Russia problem (which is larger than just Putin). When the energy and Russia problems are solved, the Brexit problem will remain if the UK refuses to change course. Keir Starmer says he can “make Brexit work” and that suggests that the UK will hit more icebergs. In the meantime, UK citizens will pay more for imports and the UK will sell fewer goods internationally, provide fewer financial and other services internationally, etc.

“The rapidity of subsequent and future Fed hikes risks a severe downturn, a financial “event” or both.”

The real issues are however is that no one really knows the severity of the downturn and its breadth, what that financial event (or events) may be and what cascade of events may follow !

If history is any guide, it will not be what is expected and it will not happen when and were anticipated.

But almost assuredly our leaders/regulators/agencies will be ill-prepared. The government in London and its handling of its recent crisis certainly does not inspire confidence. The performance and credibility of the Fed also leaves much to be desired.

Make sure your bunker is cleaned out and well stocked. Better safe than sorry as you just might be needing it soon!