Policy pivot euphoria waned Wednesday, as investors and traders weighed persistent inflation and tough-talking central banks against decelerating growth.

One generic market recap said “a growing cohort of money managers is cautioning that expectations for a so-called Fed pivot are overdone and risk ignoring the economic pain that would underpin such a dovish tilt should policymakers opt for it.” The same wrap alluded to hawkish rhetoric from Fed officials.

At the risk of coming across as unduly acerbic, these are the same money managers, Fed officials and media outlets who loudly insisted inflation was “transitory.” If the tide’s turning, they’ll be the last people to notice.

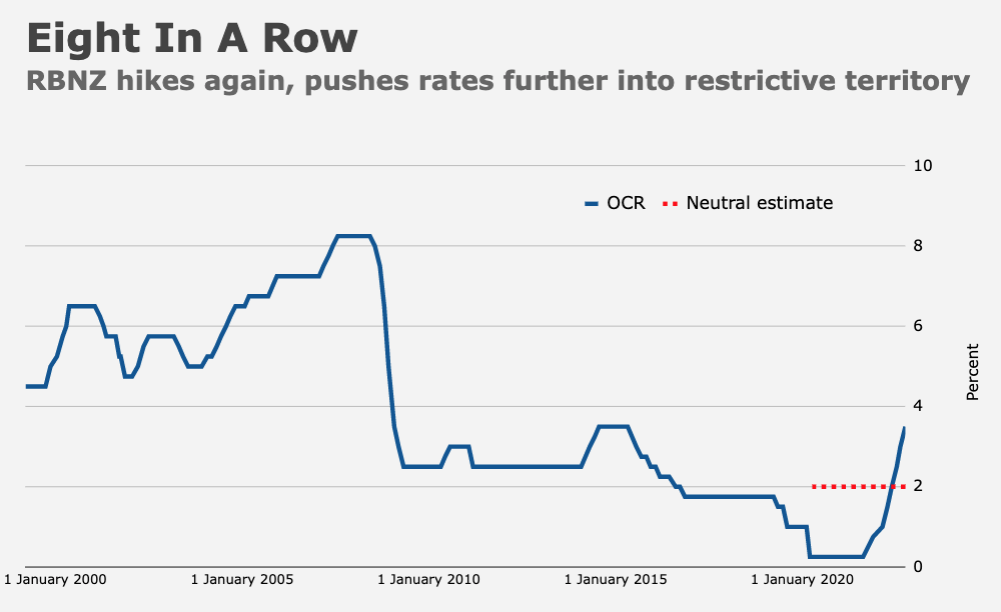

That’s not to say policymakers won’t try to hold the line. Apropos, New Zealand on Wednesday hiked 50bps for a fifth consecutive meeting (figure below), and considered a 75bps move. It made for a stark contrast with the RBA’s dovish 25bps hike from Tuesday.

The statement from RBNZ wasn’t conciliatory. “The Committee agreed it remains appropriate to continue to tighten monetary conditions at pace to maintain price stability and contribute to maximum sustainable employment,” it read. “Core consumer price inflation is too high and labor resources are scarce.”

Rates are well into restrictive territory in New Zealand. Wednesday’s hike was the eighth in a row overall. It’s not without risk. New Zealand has a very frothy housing market. “Household balance sheets remain resilient despite the fall in house prices,” officials said Wednesday. Famous last words.

Policymakers did allude to burgeoning risks to growth and financial stability around the world. “Some members believed that simultaneous and fast-paced monetary tightening in multiple countries was increasing downside risks to global growth,” the summary record of the gathering said. “Members noted that large movements in wholesale interest rates and exchange rates were causing a deterioration in financial market liquidity, which can exacerbate market volatility.” In the short paragraph detailing the debate over the proper size of Wednesday’s hike, there was mention of “lags in monetary policy transmission and a slow pass-through to retail interest rates.”

“The hawkish tone of today’s statement suggests RBNZ believes it has more tightening to deliver yet. We agree, in the short run at least,” HSBC said. Their base case calls for another 50bps hike in November before a “more marked slowing in domestic demand” sets in. HSBC has a recession penciled in for New Zealand starting in the fourth quarter.

That gets to the heart of the matter. At best, central banks are now tightening into recessions. They know that. It’s part of the demand destruction plan. At worst, central banks are risking financial stability. They may not know that — yet. Or, more likely, they know it, but don’t appreciate the scope of the risks, and don’t believe they have much choice in the matter.

Rather than walk though the standard commentary (which you could write yourself), I want to emphasize that as committed as everyone claims to be to the inflation fight, it will be subjugated to financial stability if push comes to shove. And there won’t be any discussion about it. It’ll happen overnight. Last week, traders went to bed with UK yields spiraling higher and woke up the next day to the Bank of England committing to unlimited long-dated gilt purchases. “Temporarily,” of course. The alternative, we learned over the ensuing 24 hours, was a total meltdown in the UK pension complex, not because there were long-term solvency issues, but because there was a rapidly unfolding, and extremely acute liquidity crisis. The UK came within hours (literally) of a mini-Lehman moment.

If you don’t think there are countless other such land mines buried out there, you should be a central banker. Those of us who are older than, say, 35, tend to think about the post-Lehman world as an aberration. But for quite a few market participants (many of whom operate in various professional risk-management capacities) it’s not just “the new normal,” it’s the only environment they know. Modern market structure in all its various manifestations is built on and around the assumption of subdued macro volatility, stable correlations and dovish forward guidance. Leverage was (and is still) deployed based on those assumptions. And those assumptions no longer hold.

BofA’s Benjamin Bowler captured it well. “The fact that the BoE needed to intervene in the gilt market to stave off bond market turmoil ahead of potentially forced selling highlights the consequences of putting a levered financial system through one of the fastest and most coordinated series of rate hikes in history,” he wrote Tuesday, adding that “markets are full of hidden risks and non-linearities that only reveal themselves in times of stress.”

If G10 central banks keep hiking rates, these shocks will proliferate. When they come calling, central banks will step in. It’s just that simple. And, again, I’d remind readers that it’s already happened. Last week.

On August 17, when RBNZ delivered its fourth straight upsized rate hike (so, the policy meeting before today’s gathering), I wrote that “however close we may be to turning any corners, the ‘now’ zeitgeist, if you will, remains inflation and policy tightening.” That was the correct assessment then. Stocks, which were enjoying the last vestiges of a summer rally, quickly faded and expectations for Fed tightening ratcheted higher into an extremely hawkish September FOMC meeting.

As things stand at the beginning of Q4, though, the new “now zeitgeist” is financial stability and all the “hidden risks and non-linearities” that are exposed when you put a levered financial system through a rates shock, as BofA put it.

I may be early, but sooner or later (and my guess is sooner), you’re going to see bull steepening and overnight capitulations from central bankers who, just days previous, were still doing their best Volcker impressions.

{kind=link}

I found this nugget reassuring.

“The BOE bought very little over the first three days of the program (Sep 28, 29, and 30), averaging only £1.21 billion per day, instead of £5 billion per day, according the BOE’s daily disclosures of gilt purchases under this program. It bought almost nothing on Monday (Oct 3), just £22 million with an M; and it bought £0 – meaning exactly “zero” – today (Oct 4)”

agree yield curve will likely steepen, however i think more likely a bear steepener (due to other CB dumping USTs) rather than bull steepener.

CBs will step in if they break something, but will that step be to end rate hikes and QT? BOE didn’t end rate hikes and may have only briefly delayed QT to do a very small amount of QE. Maybe that is just applying bandaids while continuing to beat the victim, but CBs are under considerable pressure to continue the beatings and they have just started to use their supply of bandaids.

JYL – now that global economies are showing signs of weakness, how strong will that “considerable pressure” remain in play?

This headline from the UK may be giving us an early glimpse of the future in terms of questioning the mandates underpinning central bank authority: “British Prime Minister Liz Truss backed the Bank of England’s authority to set interest rates independently, dropping previous mentions of a review into the central bank’s policy-making.”

If the CBs continue to stubbornly hike rates, the era of absolute power in the hands of unaccountable faceless ivory tower bureaucrats may be coming to an end. Especially with populism on the rise across the globe.

There is, certainly, a level of economic weakness that will force CBs to stop tightening. We are not even close to there in the US, where the Fed is willing to accept (trying to achieve) employment, wage growth, asset prices, demand, etc meaningfully lower than current. Mere “signs of” weakness are not enough.

The Fed spent months getting this message across, after Jackson Hole everyone professed to understand it. Now we think the US economy has deteriorated so much in a month that the Fed is going to volte-face and abandon an inflation both existential and barely starting to show progress?

Maybe BOE is in a pickle, maybe Truss has to fall on her sword, how that farcical imbroglio works out I don’t know. I don’t think the Federal Reserve is inclined to let itself be wagged by someone else’s tail.

I realize many commentators think Fed should stop tightening. I think the more relevant question is what does the Fed think.

If the thesis is Powell is thinking “I better give in to 8% CPI, eat all the words I’ve said all year, go into history as the weakest Chair ever, because [reason]” then to identify that reason, and to bailout PM Truss or because Wall Street wrote fearful notes is not enough.

All rational points, though an orthodox lens. But the authority of central banks around the world are not immutable. Political pressure to reign them in will grow the longer they drive their economies over a cliff in order to defend their reputations and historical legacies. It may end up that their legacies will end up being that they triggered the demise of central bank independence.

That said, they probably can skate by until an even more populist wave sweeps the world. So you may well be right, in the short term.