Back in July, when the Bank of Canada aimed a 100bps rocket-propelled grenade at the country’s inflation problem, market participants were quick to suggest the odds of a full-point move from the Fed were higher as a result.

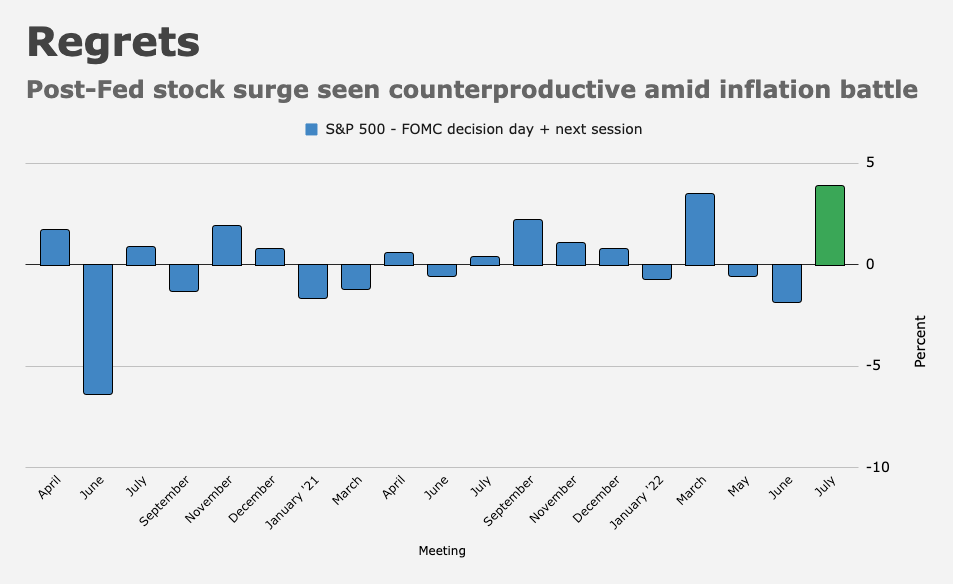

The BoC’s broadside came on the heels of another distressing US CPI report (June’s figures), but despite plenty in the way of data cover and the example set by Tiff Macklem, the FOMC ultimately opted for a second consecutive 75bps hike. They might’ve regretted not reaching for more. US equities, taking their cues from Jerome Powell’s somewhat timid remarks following that month’s gathering, staged one of the largest post-FOMC rallies in recent memory. Late last month, in Jackson Hole, Powell effectively disavowed the July press conference.

The BoC has since downshifted to 75bps hike increments, but if the Fed wanted another go at 100bps in light of August’s vexingly hot monthly core CPI reading, the Riksbank offered up another opportunity for Powell to claim full-point increments wouldn’t make the US a global outlier.

As many readers are no doubt aware, Sweden raised rates 100bps Tuesday (figure below), the largest move since the introduction of inflation targets. The decision was unanimous and came amid the highest domestic inflation in more than 30 years. “Inflation is too high,” the bank said, in an amusingly blunt opening line.

The Riksbank was adamant about the risk asymmetry. Suffice to say they don’t believe the short-term pain from higher rates is a sufficient rationale for risking entrenched (or un-anchored) inflation down the road.

“Rising prices and higher interest costs are being felt by households and companies, and many households will have significantly higher living costs,” the bank said, before extolling the virtues of aggressive front-loading. “It would be even more painful for households and the Swedish economy in general if inflation remained at the current high levels.”

Those “high levels” are set to be even higher over the next several months, according to the new projections (figure below).

“The development of inflation going forward is still difficult to assess and the Riksbank will adapt monetary policy as necessary to ensure that inflation is brought back to the target,” officials remarked.

Rates are seen rising further over the next six months, peaking at 2.5% midway through 2023. “The risk is still large that inflation becomes entrenched and it is extremely important that monetary policy acts to ensure that inflation falls back and stabilizes around the target of 2% within a reasonable time perspective,” the accompanying monetary policy report read.

Tuesday’s move was the third hike this year and, as noted, it had no precedent (figure below). Given Sweden’s famously dovish predisposition, the upsized increment felt especially anomalous, even as the market was fully aware that the policy rate would at least double.

“By raising the policy rate more now, the risk of high inflation in the longer term is reduced, and thereby the need for greater monetary policy tightening further ahead,” the bank went on to say.

There’s also some consternation about upcoming wage negotiations. “Compared with when the current agreements were concluded, in the pandemic year of 2020, unemployment is now lower and inflation significantly higher, at the same time as wages abroad are expected to increase faster than in recent years,” policymakers wrote. “This will contribute to wages in Sweden also rising faster in the coming years, especially in 2023.” That’s not necessarily a bad thing to the extent pay growth starts to catch up with inflation, but as the bank emphasized, it’s “important that monetary policy… make[s] it clear to price- and wage-setters that the inflation target can continue to be used as a benchmark.”

In April, the Riksbank paired liftoff with new projections and a plan to shrink the balance sheet, in what one analyst described at the time as “a record-large hawkish policy pivot” indicative of the Riksbank’s willingness to “throw the economy under the bus.”

If the bank was prepared to let a bus hit the economy five months ago, policymakers are apparently willing to sacrifice it, Aztec-style, now.

The new forecasts include a relatively mild contraction next year (-0.7%) and a more tepid pace of growth in 2023, but the Riksbank surely realizes it’s running the risk of triggering a much deeper contraction in the event rate hikes undercut the notoriously bubbly housing market, where variable rate loans comprise a large portion of borrowing.

Household indebtedness appears very high based on the Riksbank’s data (figure above). “It looks like, as of now, the bank accepts the housing market slowdown,” ING said Tuesday.

Even if house prices don’t “crash,” per se, the combination of higher debt costs and near double-digit consumer price growth could strangle consumption. So, you needn’t adopt a doomsday housing narrative to construct a downside case for the domestic economy.

According to the Riksbank, household interest expenditures as a percentage of disposable income will more than double over the next three years (figure above).

In any event, the point isn’t so much to forecast the near-term evolution of the Swedish economy, or to opine on the proper trajectory for local monetary policy. Rather, it’s important to recognize the signaling effect of Sweden’s 100bps bazooka shot.

Even if the Fed eschews the temptation to follow the Riksbank and, on a delay, the BoC, in resorting to a full-point hike aimed at preventing inflation from becoming even more entrenched than it already is, the fact that we’re not only talking about 100bps hikes, but in fact witnessing them, is a testament to the sense of urgency among policymakers in developed markets.

“100bps has real delta,” Nomura’s Charlie McElligott said Tuesday, before suggesting that when it comes to front-loading, the Riksbank merely “said what everybody else is thinking.”

{kind=link}

H-Man, it will be interesting tomorrow to see if Powell can deliver a “risk off” message. Unfortunately, his track record suggests he will say something that turns “risk on”. But you never know.

“100 bps is a necessity to stay front-footed on hitting the demand-side of inflation as hard as possible,” McElligott said in a note to clients on Tuesday.

In Canada, Trudeau and his financial illiterate finance minister are still showering money to the class with the highest propensity to spend, throwing more gasoline to the inflation fire. Anecdotally, I am seeing inflation is getting more wide spread here with all service sectors increasing price by 10+% (i.e. car service, dental, restaurant). With the declining Canadian dollar (so far mainly against US dollar), inflation will only go higher, forcing BoC to hike more aggressively. I hope Trudeau doesn’t make the same mistake as Liz, but my confident is not high, as the minority government is prop up by the left leaning party.