While I suspect there were few kind words for him in the 1980s, today Volcker is recalled as a folk hero while Burns is noted as a political toady. It does not take a psychiatrist to suggest that Mr. Powell would much prefer “Volcker Revisited — Powell Saved the Nation” rather than “Arthur Burns Redux — Powell as Political Coward.”

A Commentary by Harley Bassman

Over a century ago, Alfred Henry Lewis observed that “there are only nine meals between mankind and anarchy,” a not unfathomable possibility if the complications from COVID were closer to Ebola rather than Influenza.

Notwithstanding the $801 billion US Defense budget, larger than the next ten countries combined, little effort is required to imagine the result if the workers at Consolidated Edison and the Croton Dam aqueduct were too fearful to punch in.

And while I have little interest in joining the bleating mob of financial pundits whose weak egos require a steady stream of “likes” and “re-tweets,” I will note that our “Rhyme with History” is not 1930s Europe, but rather to 1850s America.

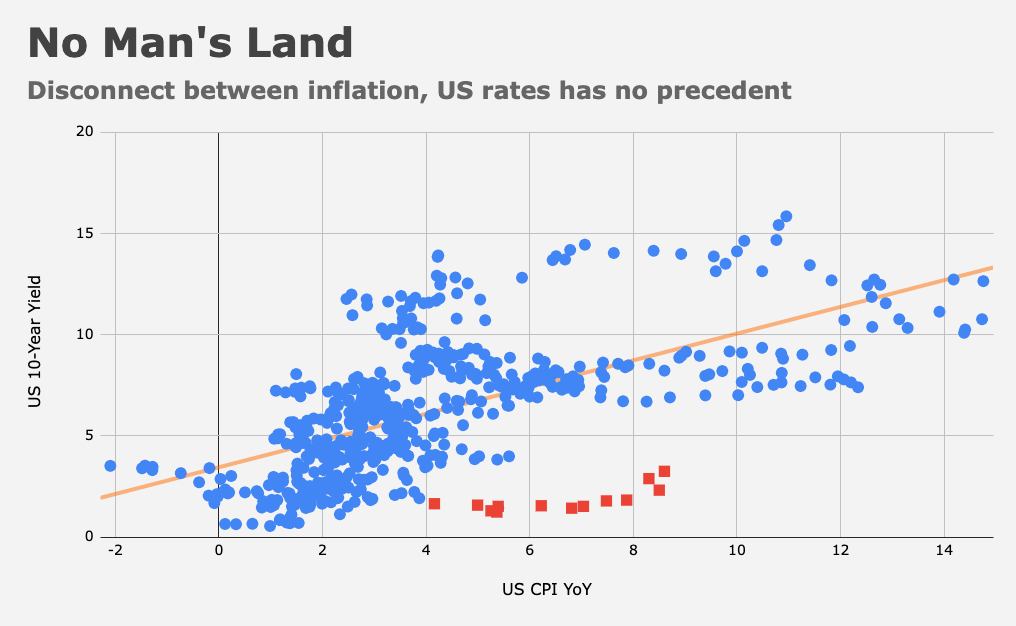

The Fed is “behind the curve” and is accelerating their policy actions to catch up to both the economic data, as well as financial market rates and prices. The question we explore today is the potential severity of the resulting unintended consequences.

Jerome Powell serves a four-year term at the pleasure of the President. His first term started on February 5, 2018, and was set to expire in February 2022. To maintain continuity at the world’s most important financial institution, a nomination (or re-nomination) often occurs in the late summer of the year prior to let the machinery of government grind efficiently.

For a variety of reasons, Mr. Powell’s re-nomination did not occur until November 2021, and his confirmation was not offered for a vote until May 12, 2022, a full three months after his term officially ended.

Inflation, as measured by the benchmark CPI, had been bubbling at 5.4% from June to September 2021, well above the FED’s stated “target level” of 2.0%. The CPI for November, the same month Mr. Powell was re-nominated, was reported at 6.8%. Nonetheless, the FED maintained their overnight Fed Funds rate near zero, and continued bond purchases at $120 billion a month.

Call me cynical, but I suspect Mr. Powell was worried that he might lose support from some in Congress if he abruptly hiked interest rates and curtailed QE before his confirmation.

A past FED chair had noted it was their job to “take away the punch bowl just as the party gets going.” Here, the FED was juicing the Kool-Aid with 151 until they finally hiked a paltry 25bps in March, coincident with a 7.9% CPI report.

Mr. Powell’s tone turned hawkish soon after he received the nod from Congress, but by then inflation was headed toward 8.6%, the highest in 40 years. The FED was now chasing inflation, a rotten position for a policymaker.

While the FED slept, the bond market was jittery with anticipation as it recognized that action, while delayed, was surely forthcoming. From a standing start at 65 before Mr. Powell’s re-nomination, the -shavkapito line- MOVE Index more than doubled to 135 by the time he was confirmed.

Concurrently, the yield curve flattened as the spread between the two-year rate and the 10-year rate compressed from 110bps to a full inversion in April.

While a lot of hand waving about security selection occurs on this topic, it is a stone, cold fact that the best predictor of a recession is the yield curve, and presently the yield curve is inverted via most vector variations.

Most impacted by the FED has been the retail 30-year mortgage rate, the rate a homeowner borrows at to buy a house. This is different from the MBS (mortgage-backed security) rate, which is the yield one can earn when purchasing bonds guaranteed by the government (Ginnie, Fannie and Freddie) that hold such loans.

Residential construction, and its associated entanglements, constitute over 15% of our economic activity. And such a rate increase combined with the jump in home prices has nearly doubled the median cost of a new mortgage over the past 2.5 years.

Last year, one could buy a $500,000 house by borrowing $450,000 at 3.25% for a monthly payment of $1,958. At a 5.50% rate, that same $1,958 monthly payment and $50,000 down payment can only buy a house priced at $395,000.

All else equal, higher rates could reduce housing prices by more than 20%.

There will not be a repeat of the 2008/09 mortgage mess, but housing activity is going to slow significantly, which means GDP will slow in a meaningful way.

I have always wondered how the Wall Street economists project the spending patterns of the median family when they have so little in common economically — a family’s grocery bill can be dwarfed by Thursday night’s bar tab at the club.

It is common practice to focus upon “core inflation,” where the costs of food and energy are stripped out. (Isn’t inflation less everything zero?) So, why ignore the most basic and inelastic items in the shopping cart?

Up in their Ivory Tower, “team transitory” opines that we are not experiencing “real” inflation, while down in the street, the cost of the most basic of necessities has elevated by double-digits annually.

While I will stipulate that inflation likely has peaked, estimates still model inflation at well over 5% one year hence.

The Conundrum

The FED has an effective dual mandate to keep unemployment low while at the same time limiting inflation. The realpolitik of this public policy balance is that, at this moment in time, controlling inflation supersedes supporting the economy.

The second- to fourth- quintiles of the US population earn between $27,026 and $141,110 (2020 dollars). Assuming that the top quintile is only marginally affected by inflation, and the bottom quintile has access to various means of public support, the 60% middle section will likely have to make lifestyle-altering decisions with inflation above 5%.

On the contrary, if unemployment rises from its current 3.6% to the 6.2% peak of the “tech-bubble pop” 2001 recession, only 2.6% of the population suffers.

But let’s toss the abacus and consider the human emotions of the situation. As I often note, we still read the Greek tragedies (Aeschylus, Sophocles, Euripides) and Shakespeare because they identify Hubris (ego), mankind’s destroyer.

Arthur F. Burns was the FED Chairman between 1970 to 1978. He was famously accommodative to politicians, particularly Richard Nixon, who demanded the unemployment rate be limited to 4.0%. Of course, this did not end well as inflation reached 12.3% in 1974. Mr. Burns is not remembered fondly.

Paul Volcker ascended to the FED Chair in 1979, and quickly raised short-term interest rates to 20% which jolted the economy into a short recession. After easing rates back to 8.0% in 1980, he again slammed on the brakes taking the FED Funds rates to 22% and unemployment to a post-war high of 10.8%.

While I suspect there were few kind words for him in the 1980s, today Volcker is recalled as a modern-day folk hero while Burns is noted as a political toady. It does not take a psychiatrist to suggest that Mr. Powell would much prefer to have the headline of his WSJ obituary read “Volcker Revisited — Powell Saved the Nation” rather than “Arthur Burns Redux — Powell as Political Coward.”

Whether one is swirling the tea leaves of the yield curve which are indicating a recession early next year, or the head-turning Atlanta Fed GDPNow forecast of a negative 1.2% GDP, I can assure you we are soon headed towards an economic decline, but this does not matter.

The “inflation is transitory” nerds may point to a declining PCE Index, but CPI above 6.0% will grab the headlines, and Mr. Powell will not relent until this measure is well below 4.0%.

If indeed real GDP is reported as negative in the second quarter, that would qualify as a recession since the unofficial definition is two consecutive quarters of real economic decline.

However, that would still produce a -bokchoy line- Nominal GDP in excess of 6%, which is well above the -clementine line- rate of the 10-year US Treasury at 3%.

While I cannot produce a formula for a correlation, I can offer that it is fundamental that the means of production should have a relationship to the cost of production, otherwise there exists a macro-economic arbitrage that must be closed — either by a rise in interest rates or decline in nominal GDP.

Managing the Inflection Point

Via its construction, it is highly unlikely that reported CPI will break below 4.0% before the November election. And this underpins the FED’s median “dot” projection of 3.4% for year-end 2022, and 3.8% for December 2023. This is at odds with the financial futures market that is betting the FED will be cutting interest rates shortly after the new year.

This cognitive dissonance may explain why interest rate volatility, both realized and implied, has tripled since January 2021 while equity volatility is almost unchanged. And to be clear, both the MOVE and the VIX are “fair” relative to the actual volatility for each asset class.

The bottom line here is that there is significant potential for disruption — social, economic and political — if the relationship between inflation and long-end yields normalizes at the same time jobs are shed as the economy chokes on reduced housing activity and higher consumer prices, which is not a ridiculous suggestion.

Closing Comments

As noted, financial risk is currently concentrated in the bond market where the path of interest rates is uncertain. And while the cost for a one-month option is prohibitive (The MOVE ~150), the implied volatility for long-dated options on long-term interest rates is less than half that level.

As such, a long-dated Payer Swaption Hedging Strategy with a relatively small “modeled” one-year theta decay of 3.9% is still reasonable.

More interesting is the relatively low cost of out-of-the-money SPX put options. Despite a ~20% decline marking an official

“bear market,” its slow, grinding path has kept the VIX mostly under 30 with a put skew 1SD under the average.

“It is never different this time,” or so I often remind myself. Market inflections are only obvious after the fact.

My advice is to check your portfolios for short convexity positions and make sure you can handle a drawdown. This would include covered call strategies, lower-rated credit, callable bonds and levered investments with unsecured funding risks.

I am adding risk with guardrails and as you might imagine, listed products with embedded long option positions (hint, hint!).

Remember: For most investments, sizing is more important than entry level.

Harley S. Bassman July 12, 2022

Bought a put on SPY last week — indeed more inexpensive than I expected.

Wish I knew what this meant “listed products with embedded long option positions (hint, hint!).”

He is talking about the products they offer at his firm Simplify

Naybe I don’t understand the No Man’s Land chart but it looks to me like we’ve had a similar size disconnect-just on the other side of the line. Was that Mr. Volker?

Harley is my guy….

Clear thinking leads to clear writing… This covers risk…Let’s add uncertainty- Vlad the Mad….