The world is changing. Nobody knows that better than Cathie Wood.

Wood’s meteoric rise was predicated on a changing world. She built an ETF empire making large, concentrated bets on disruptive technology in all its manifestations, from AI to clean energy. The world was changing and, in many respects, dying. In 2014, Wood decided to go all-in on companies changing with it or trying to save it. Subsequently, she made a fortune for her investors and, one imagines, for herself.

Wood’s equally spectacular fall from grace (illustrated by the poignant visual below) came courtesy of a changing world too. In an especially cruel, deeply ironic twist of fate, some of the very problems Wood’s investment philosophy aims to address — including existential public health threats and the rising odds of climatic oblivion brought on by humanity’s hopeless addiction to fossil fuels — triggered a macro regime shift that undercut her strategy.

Irony atop irony: The belated character of efforts to address climate change condemned us to a desperate, haphazard approach, which entailed, among other things, deliberately discouraging investment in traditional energy, a state of affairs that’s now amplifying a global energy crunch.

To Wood’s critics, Ark is a dot-com redux. Indeed, the drawdown in Wood’s flagship fund has unfolded over a more compressed timeframe than the tech meltdown two decades ago.

With inflation soaring and monetary policymakers rushing to rein it in, rates are rising rapidly, undercutting high-growth, long-duration equities. The accompanying surge in bond yields is insult to injury for strategies like Wood’s, as is a forced pivot back to reliance on fossil fuels on the excuse we can’t save future generations if we freeze (or burn up) before we can have kids and grandkids. Recession fears associated with stretched consumers and higher interest rates imperil the prospects of profitless companies and may prevent startups with world-changing ideas from accessing the capital they need to bring new technology to scale.

“Against a backdrop of sky-high inflation, rising rates and growing recession concerns, the S&P 500 has had its worst start to the year since 1962, with the tech-heavy Nasdaq and unprofitable Growth companies performing even more dismally,” Goldman’s Allison Nathan wrote, in the introduction to the latest installment of the bank’s “Top of Mind” series, which features interviews with industry heavyweights, who weigh in on the key issues facing investors. In 2022, one such issue is “whether equity markets are in the midst of a paradigm shift,” as Nathan put it.

Naturally, Goldman spoke to Wood, who’s spent the last several months defending her strategy against a growing chorus of detractors, even as her fervent fan base continues to pour money into her funds. Wood recently insisted that deflation, not inflation, remains the most entrenched secular theme and thereby the biggest risk.

Asked by Nathan “how concerned” she is that macro factors will continue to weigh on performance, Wood doubled down. “We are not overly concerned because we’re already seeing signs that inflationary pressures are beginning to ease,” she said, adding that,

We have long believed that the current inflation surge is a one-time shock to the system, although it has lasted a lot longer than we initially expected. I’ve never seen supply chain issues take this long to work out, and we didn’t expect Russia to invade Ukraine — both of which have extended the duration of the inflationary shock. But inflationary pressures have begun to unravel, as reflected in declining global shipping rates and record-high inventory levels at the major retailers — that are up by as much as 30-40% YoY — which is forcing them to reduce prices to clear their shelves. And, on the labor side, the sector that suffered from the biggest post-pandemic worker shortages — retail — has seen average hourly earnings growth decline from a peak of 20% YoY in late 2020 to the 3-4% range today, which is below total average hourly earnings for the economy as a whole. So, while many people won’t believe it until we see clearer evidence in the data, especially as oil prices remain elevated, I do think we are on the other side of the inflation problem. I also take comfort in what the level of longterm rates is telling us about inflation. The 10-year US Treasury yield, which has historically closely tracked nominal GDP growth, is currently sitting at around 3%, indicating that nominal GDP growth over the next decade will average around 3%. If inflation persistently remained in the mid- to high-single digits, that would translate to a decade of negative real growth, which seems highly unlikely. So, I think the rates market is telling us that inflation will eventually come down to levels consistent with positive real growth, and have been surprised that more investors don’t seem more reassured by this.

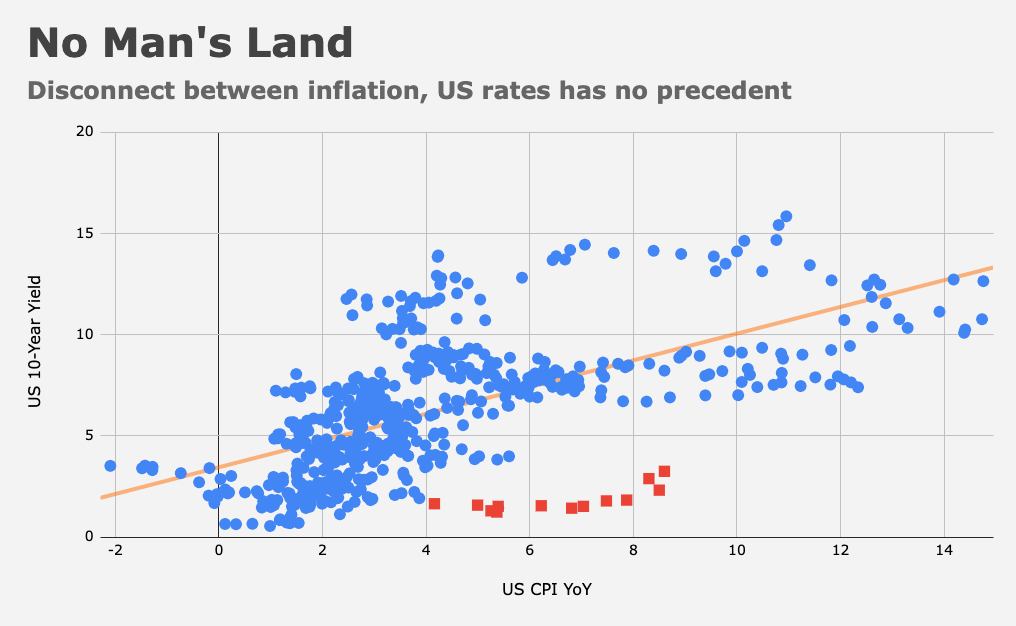

Wood is certainly correct on the math. The disconnect between 10-year nominals and headline CPI remains very pronounced, even after yields rose sharply over the first half of 2022.

“Market variables have achieved autonomy from economic fundamentals and their disagreement can no longer be interpreted as a temporary dislocation that is likely to converge, but emergence of an altogether new framework,” Deutsche Bank’s Aleksandar Kocic wrote late last year.

The figure (above), shows that despite the worst quarterly performance for US Treasurys in decades, virtually no progress was made towards normality. The red squares depict CPI-yield conjunctures witnessed over the past 13 months.

Of course, yields could be sending a false signal about the likely trajectory of inflation, but Nathan gave Wood the benefit of the doubt. “Even if we are on the other side of the inflation problem, isn’t the recent rout for Growth companies telling us that prices and valuations for certain stocks, particularly those of unprofitable companies, rose way too far, not unlike during the dot-com bubble?” she wondered.

Wood’s answer was classic Cathie. After conceding that the scope of the drawdown in her flagship fund (illustrated in the first figure, above) is comparable to the Nasdaq’s collapse during the 2000 tech bust, she said there are a pair of “important differences” between 2000 and 2022.

“During the dot-com bubble, many companies were chasing a dream and simply shouldn’t have existed. Too much capital was chasing too few opportunities too soon,” she said, calling yesteryear’s technologies not “ready for prime time.” She cited AI, which was in its infancy, and the exorbitant costs associated with advances that, just two decades later, can be had for a song.

She acknowledged the derisive language often used to describe her strategies — “profitless tech,” “tech wreck” and so on. Wood cited that as anecdotal evidence that “a lot of negative news is already priced in.” She also noted that consensus still expects robust revenue growth and rising profitability from her companies, versus falling estimates and expectations for margin contraction at a comparable period during the dot-com bust.

“Despite these differences, investors are still running for the hills, towards their benchmarks,” she told Goldman. That decision, she said, may “prove to be as wrong as racing towards the dream was during the dot-com bubble.”

As for her dream, it’s organized around five platforms: Genomic sequencing, adaptive robotics, energy storage, AI and blockchain technology. “AI is here. Cloud is here. Gene editing is here,” Wood said. “The dream back then is now a reality.”

She might be right about everything she says but for the unfortunate masses, their dream is to be able to pay for gas, utilities, and food and have a little something left over each month.

Unfortunately the masses are slow to realize that we need to stop burning gas, we have to convert our utilities to renewables, and we need to change the way we produce and consume food. If we (our species) were on a rational path to realize these changes, then it would absolutely make sense to invest in these areas. But we aren’t on a rational path.

Rational thought also told us we should have started all this work decades ago and, if we didn’t, we would just be driving up our costs. Those chickens are once again coming home.

In a society governed by selfish greed and officials who only care about protecting their seats, no chance we’ll ever change the way we must in a timely matter. The cost of fixing the mess we made is now trillions higher than if the fix had started in Reagan’s time. The biggest fear controlling our lives is the Fear of Pissing Off our Constituents, who just want to keep their piece of the pie growing.

Quite apart Joey’s point, it’s also worth noting that the masses are rarely at the forefront of history. Not never (revolutions being the big exception) but not commonly.

Cathy is financing people who have a very decent shot at transforming the masses’ lives for the better.

H-Man, isn’t it always a matter of timing?

Look at the top 10 of ARKK.

TSLA ROKU TDOC SQ ZM SHOP SPOT TWLO COIN U

Not exactly the laser focus on “Genomic sequencing, adaptive robotics, energy storage, AI and blockchain technology” that she touts. I see a streaming device, a video conference service, another one, a streaming service – all kind of pedestrian stuff really. An exchange that is a consumer of rather than a source of blockchain technology. A car company whose days of biggest product differentiation are in the past. A payment processor that is branching into other things with just as much competition and just as thin margins as its original biz. Etc.

She’s claiming the market’s behaving irrationally, if she can stay solvent long enough…

(Also, VC is probabilistic, so how many companies does she really need to return 100x?)

Interestingly Warren Buffet’s “own it” approach protects from public market (sometimes wild) sentiment, and of course he’s into Oil and Railroad and only recently a big Apple fan…

Her macro view sounds right.

However, I have not/can not willingly invest in a company that is not profitable or has an insanely high PE….I am ok with “slightly insane” (for both stocks and people)!

For sure, you can modulate her strategy. Ignore the highest PE ones unless you know enough to judge their products directly. And add some ‘defensive’ tech (AAPL, MSFT, AMZN, GOOG maybe FB if you’re feeling brave).

Of ARKK’s 35 holdings, only 10 have any “E” at all and for most of those it’s a very little “e”.

Possible to cherry pick a name here and there, but her strategy is so extremely extreme that modulating it to be otherwise basically means building an entirely different portfolio.

I looked at ARKG’ holdings list about a year ago, hoping to harvest ideas from her crack research team. It turned out to just be a dump of every name that had an (sometimes remote) association with “gene-“anything – gene sequencing, genetic testing, genetically directed customized medicine, gene editing, gene therapy.

There was no actual security selection discernible. Basically Ark was doing “thematic investing”.

Thematic investing is dangerous in very early stage industries. The great majority of the companies will fail and be your huge losers. You need the remaining 5% to be monster winners (10-20 baggers) just to break even.

Thematic investing only pulls in investors when the theme is “hot”. The stocks are already bid way up by the time most of your AUM arrives. You need 10-20 baggers from names that are already very expensive by any standard metric.

When I saw what Ark was doing in an industry that I know about (I picked and traded clinical stage biotech stocks for a decade) I didn’t bother to look at what they were doing in industries that I don’t know as much about (ARKF, etc).

Like JYL, a while back i looked at the holdings in ARKG. The head-scratcher for me was the size of their holdings in ARKG. Telemed as a genomics play? Huh?

Interesting that Cathie Wood still firmly believes that her dream is still alive, but just hit a temporary bump in the road.

AUMs began to increase significantly in late 2020 and during all of 2021, AFTER the meteoric rise of the ARK funds during the pandemic period of 2020.

For all of these late investors, the dream has now become a nightmare.

Her dream is very much alive.

$15BN AUM implies management fees of $150MM or so? I’m not going to look up her fees, just using 1%. Even if her AUM drops another 50%, the company is still taking in $75MM ish revenue? She is so promotional that I’ll wager she can maintain several $ billion AUM levels for the next decade almost regardless of performance. Unlike the companies it invests in, I’m sure that Ark is very profitable.

(I mean, Hussman Funds has an unmatched record of miserable performance, but has held on to an appreciable amount of its peak AUM. After looking through ARKK and ARKG, I think I’m more likely to scour the Hussman portfolios for ideas than Ark’s, especially in this market environment which really should be his cup of tea?)