If you’re betting on anything more than a short-lived bounce in US equities, an end to the war in Ukraine is your best (and perhaps only) hope.

“Outside of a peace agreement, it’s difficult to construct a case for more than a bear market rally,” Morgan Stanley’s Mike Wilson said, in a Tuesday note.

Wilson has, of course, been skeptical of stocks for months. Earlier this year, he flagged a buildup in inventories as a potential headwind for corporate profits to the extent discounting might eventually be required given goods-to-services switching or outright consumer retrenchment in the face of surging costs for necessities.

That call proved prescient. It was borne out by earnings reports from America’s largest retailers, who are now sitting on tens of billions in “extra stuff” (as Bloomberg put it).

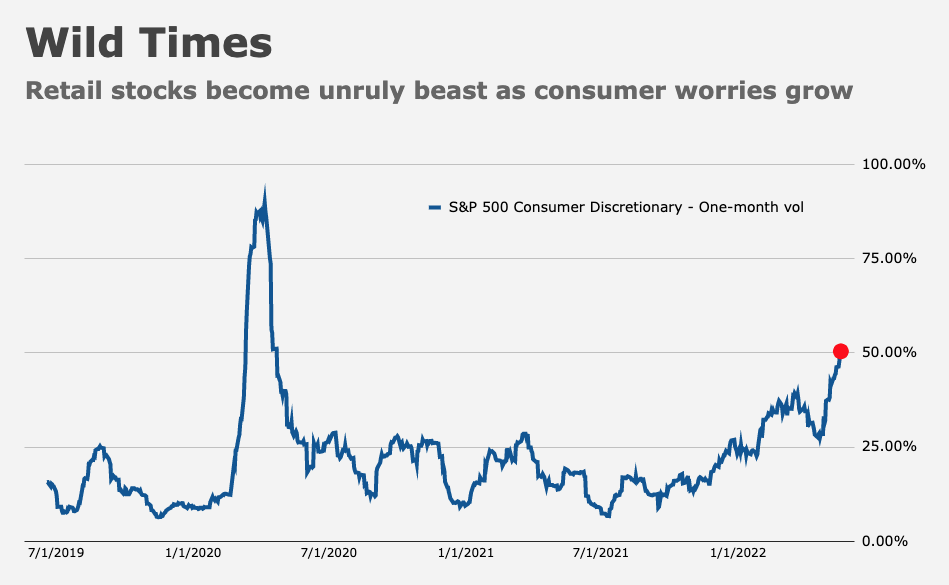

“We remain firmly in the bear market camp but relief rallies can happen at any time, and it appears we are now in the midst of one,” Wilson said. He mentioned a short squeeze in beleaguered discretionary shares, which have performed very poorly in 2022 (figure below).

Recall that discretionary stocks became a volatile beast recently.

Additionally, Wilson suggested any rally in tech and comms services will likewise prove fleeting. “Both are vulnerable to a payback in demand and/or a cancellation of orders in the case of tech hardware and semiconductors,” he said.

Note that the FAAMG stocks, along with Tesla and Nvidia, recently surrendered the entirety of the gains logged since 2021 (figure below).

The malaise weighed heavily on hedge fund returns, given the popularity of the top tech names.

Wilson attributed last week’s rally (the largest weekly gain since November 2020) to speculation about a Fed “pause” at the September meeting, a prospect I both doubt and don’t doubt.

I doubt it in the sense that 175bps of tightening (which, barring something unexpected, will be the amount of delivered rate hikes by September) won’t be sufficient to slow the economy such that enough demand evaporates to offset the most severe negative supply shock in modern history.

I don’t doubt it in the sense that the Fed, since Volcker, has shown little appetite for large declines in financial asset prices and severe economic contractions, both of which are likely in the event policymakers attempt to push rates into restrictive territory over a compressed time frame, as officials continue to insist they’re prepared to do.

Wilson is ambivalent on the issue. He walked through both sides of the argument, noting that although the Fed is nowhere near achieving price stability, higher real rates, falling stock prices and a slowdown in housing market activity suggest markets are doing the Fed’s job already. But the Fed may yet surprise investors by refusing to change course.

Ultimately, Wilson doubts it matters until inflation recedes. In Morgan’s view, “inflation remains too high for the Fed’s liking and so whatever pivot investors might be hoping for will be too immaterial to change the downtrend in equity prices,” he wrote.

The annotated figure (above, from Morgan) is simple, but sometimes there’s elegance in simplicity.

None of the above precludes bear market rallies, like the one seen last week. It just means that a compelling, fundamental case for stocks is challenging to construct right now, even when you’re trying. And I’ve tried.

The best such case involves an end to hostilities in eastern Europe, which seems far-fetched.

“If such a cease fire were to happen and could be sustained, it would relieve a lot of pressure on global growth and commodity prices, thereby improving the outlook for equities,” Wilson said.

As things stand now, though, he regretfully wrote that “the probability of our bull case target of 4450 12 months out is looking less likely than when we published it just three weeks ago.”

{kind=link}

H-Man, I agree the cease fire will be a boon (as well as the demise of Putin) but it appears they are simply digging in which will be a protracted battle in Ukraine. I can’t argue with the logic of Wilson, this is ultimately going to be a landslide dragging everything down in it’s path.

I can’t see sanctions on Russia stopping while Putin remains in power (which seems likely longer than Biden will be in office).

The push for non-Russian energy means higher prices for US producers along with a great case for renewables and incentive for Europe to truly break its addiction.

The major change for improving global stability would be a breakthrough in shipping all the foods and goods Ukraine have – otherwise sadly the world’s (economically) fine with some random corner being in a forever war (Iraq, Afghanistan).

Hopefully someone creative figures a way to transport westward or more likely (Turkey who get a commission?) negotiates a deal for Black Sea shipping.

(Alternate universe: enough Russian warships are sunk by drones so that they leave – much like the tanks that were destroyed on the way to and running away from Kiev).

Here is what troubles me. Yes, the war and zero-Covid will eventually end, supply of energy and food and China-made stuff will return to something like “normal”, inflation will ease off, Fed will back off. Market will probably front run that and rally big. We all hope to catch that move, whenever it is. Late 2022 maybe?

When the dust settles, will there have been a structural change in business models such that SP500 margins should stay as far above the pre-pandemic level as they are now? Have SP500 companies really moved to a permanently higher profitability level? Or have they just been over earning for the past two years?

I mentioned, in comments to a prior post, what can happen to 2023 estimates if margins simply revert to “normal”, e.g. 2019 levels. Down revisions, sizeable.

Maybe it’s too early to worry about that. It’s not 2023 yet.

But estimates can get cut fast – ask WMT TGT shareholders.

And, worse case, if inflation/tightening stick around long enough to overlap the “normalization” of margins, that could really be, well, interesting.