If the current malaise on Wall Street is a non-recession correction, it’s an unusually long one.

“Corrections outside of recessions typically ended in three months,” Deutsche Bank’s Binky Chadha and Parag Thatte wrote, in an exhaustive, chart-heavy piece called “At The Recession Crossroads.”

May marked the fifth month of the selloff. There’s no end in sight. Even a tactical rally now seems like a dubious proposition to some observers. “It no longer makes sense to own equities,” one strategist sighed, while abandoning a call for a tradable bounce.

The figure (below) illustrates Chadha’s point. The current selloff is 34 sessions longer than the median non-recession correction.

Chadha and Thatte walked through a hodgepodge of figures and statistics which together suggest the market sees “an imminent recession.” Stocks are pricing an ISM of 40, for example, and a ~20% decline in earnings.

The data tells a different story. Payrolls may be a lagging indicator, but the US labor market is still strong, notwithstanding the uptick in jobless claims and this week’s cringeworthy regional Fed surveys. Chadha said there are “no signs” of big capex cuts just yet and leading indicators don’t signal a downturn tomorrow.

That said, Deutsche Bank cautioned we’re late cycle, and noted that even with this year’s de-rating, multiples are far from low. At ~16.5, the S&P’s forward P/E is merely back in the range seen from 2015 to 2019.

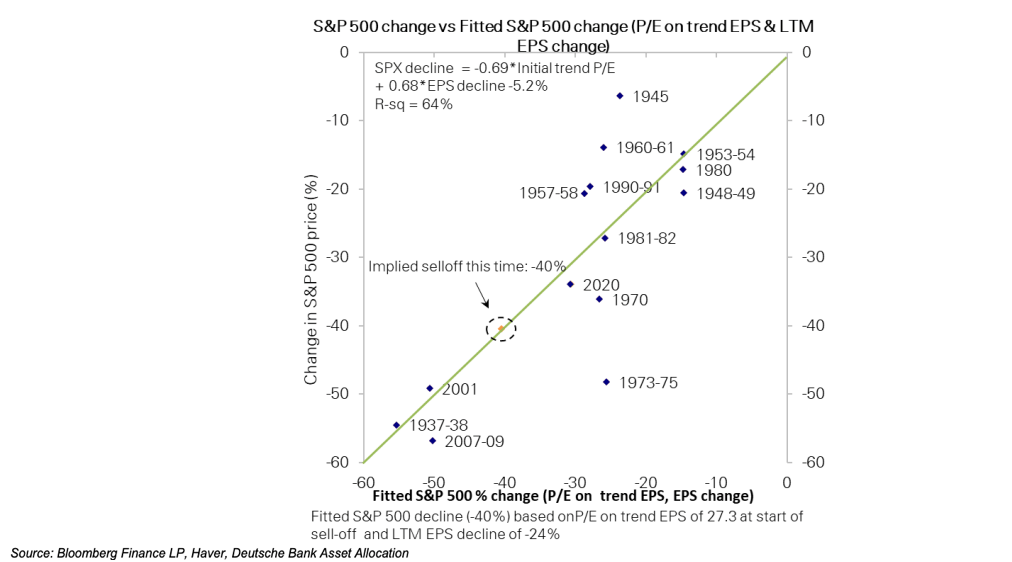

The valuation point is important because, as Chadha emphasized, selloffs are “well explained by initial valuations and earnings declines.” If there’s a recession, one pretty much has to assume a drop in earnings commensurate with historical downturns, but considering the extremely elevated starting point for multiples, the accompanying equity drawdown could be deeper than the historical median (24%).

“In the event we slide into a recession imminently, we see the market selloff going well beyond average,” Chadha wrote, suggesting the S&P could fall between 35% and 40% to around 3,000. The scatterplot (above) illustrates the point.

But it’s not just a valuation and earnings story. Generally speaking, stocks bottom in the middle of recessions. The recession hasn’t even started yet, or at least not that we know of. Assuming we’re in a recession now, stocks would bottom sometime in November which, I’d note, would be extraordinarily inconvenient for Democrats and the White House, albeit totally consistent with the Biden administration’s unfathomably bad luck.

Additionally, Chadha noted that although equity outflows have picked up, we’re nowhere near any kind of wholesale exodus. Remember: 2021 was a bonanza for inflows to global equity funds. We’re just starting to see that reverse (figure below).

The implication: There’s a long way to go in any kind of recessionary scenario.

As for buybacks, Chadha wrote that although the corporate bid is still supportive for stocks, it’s obviously tied to earnings. “In a recession, an earnings decline would also mean lower buybacks as they tend to be highly cyclical,” he said.

For discretionary investors to get more bullish, the growth scare needs to abate. For systematic cohorts to re-leverage, vol needs to recede. Neither of those two conditions are met right now. Between that, the late cycle dynamic, still elevated multiples and the “sticky inflation” that’s keeping the Fed in full-hawk mode, Deutsche Bank expects the S&P “to at least price in a full recession decline of -24%.”

From there, Chadha said, “the outlook looks relatively binary.” Either the US falls into recession or it doesn’t. If it does, the S&P could drop to 3,000, as noted above.

One shudders to think where the index might end up in some manner of worst case scenario that finds the world’s largest economy succumbing to a “major recession.” Fortunately, almost no bank is predicting such a thing.

In a recession scenario, the “S&P could drop to 3,000”. The S&P first crossed 3,000 in October 2019, less than three years ago. I suggest that a recession bottom of only 3,000 might be a win. In the early 80s (the last recession tied to fighting inflation), the S&P bottom was the same level as 10+ years prior. In 2002, the S&P 500 bottom was the same level as 5+ years prior. In 2009, the S&P 500 bottom was the same level as 12+ years prior.

I think fair value for SP500 in a mild recession is around -12% down from here. Assume overshoot below FV. A severe recession and/or long rates rising more than 100 bp from here would, naturally, take FV lower.

Begs the question often raised by @RIA, how high/tight can rates/FCI go before there’s a big “accident”.

As for timing, markets often bottom before the economy does, and everything seems to happen faster now. Events may unfold more rapidly than in prior downcycles when the Fed was fighting against the downturn instead of actively causing it.

H-Man,

Since Joe consumer is 70% of GDP, if Joe checks out bad news for GDP and bad news for equities. Walmart and Target + Kohls tell us Joe is under stress. If gas breaks $6 a gallon this summer while rates are rising, Joe is not going to be eating cake. Toss in higher rents, higher mortgage rates, higher electricity, higher water costs, oh and higher food costs —- Joe will be running to peanut butter and jelly while nixing anything that is non-essential (Netflix). Meanwhile Joe will scream for higher wages to combat those effects. But if your business is making less, Joe’s cry for higher wages will not be answered.

Bottom line, this is going to end ugly and a 40% drop may be optimistic.

It is not looking good. However, there are a lot of folks on one side of the boat right now. At present we have a really strong $, a hawkish fed, tightening financial conditions, a pandemic still, and a regional war in Europe in danger of spreading. It is actually amazing the market is not down more. If the Fed backs off after a couple of fitties you could see a pretty major rally in stocks, a weaker $, and lower intermediate interest rates. Without too much strain I could see Ukraine winding down, and the pandemic becoming more or less endemic. In that case S&P could be 5500 by end of 2023. Or we could go into the tank. Isn’t it great?

I don’t think in this case or in many cases what is happening to the Biden administration can be boiled down to luck. Afghanistan was a gift from Trump. BBB failing is squarely on two Democrats. And the economy tanking just in time for midterms is a failure of the Fed. It’s incompetence and corruption railroading this administration, not luck. Not that most voters will bother to try to understand that.