Investors pulled billions from money market funds in the four weeks through mid-February, a period that coincided with a deluge of inflows to global equity funds.

The outflows from cash stand out considering sharply higher short-end rates and the distinct possibility of more curve inversions as the Fed commences tightening into a slowing economy.

Total money market fund assets fell by $34.35 billion in the week ended February 9, ICI’s data showed.

Plainly, money market fund balances remain extremely elevated. It’s the juxtaposition with the evolution of the Fed narrative and rapidly rising yields that’s notable.

Citing EPFR, BofA counted almost $48 billion fleeing cash during the latest weekly reporting period. That, “despite soon-to-be-inverted yield curves encouraging reallocation from long-end to short-end,” the bank’s Michael Hartnett remarked.

Apparently, some of the money is going into stocks, which have de-rated materially, even as many expect more turbulence.

Global equity funds took in an enormous $46.6 billion over the latest weekly reporting period, a mirror image of the cash outflow. As noted here last week, there’s been no capitulation in stocks if you go by flows.

Last week’s inflow brought 2022’s YTD haul to almost $153 billion, still slightly ahead of 2021’s pace (figure above).

Hartnett contrasted apparently voracious appetite for stock “bargains” with deteriorating sentiment, and the “quiet” selloff in corporate credit.

There’s been a “big reversal in credit flows,” he wrote. The figure on the right (below) speaks volumes.

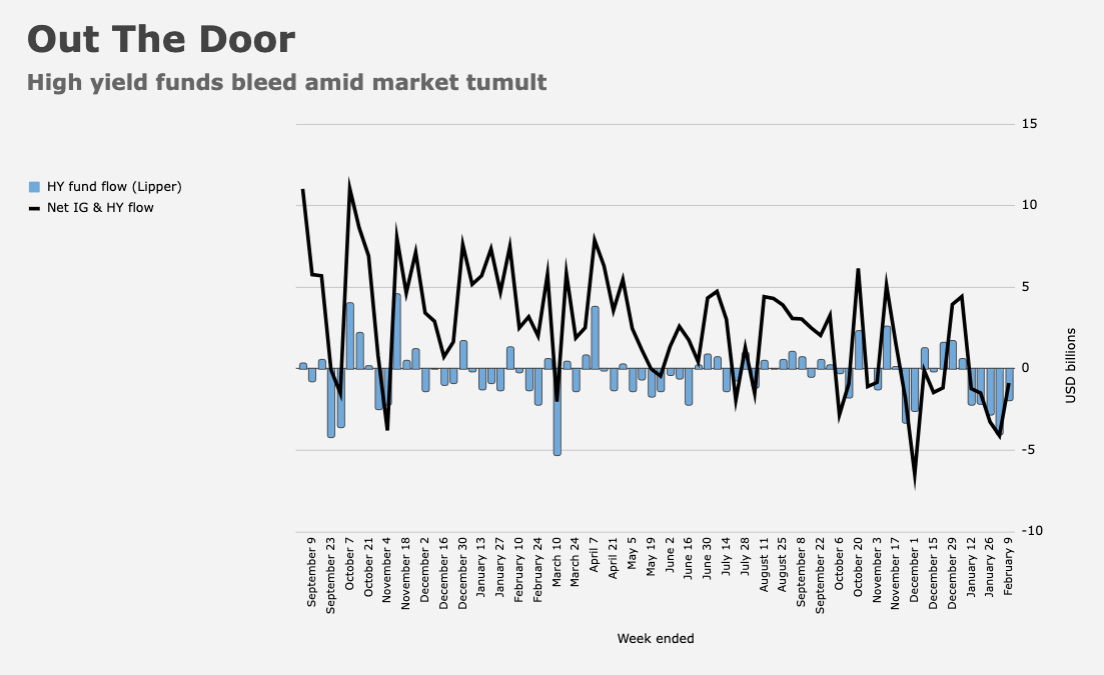

There was more evidence of credit jitters this week. CDX IG was the widest since September 2020 on Friday, for example. And Lipper data showed junk funds bled another $2 billion in the week through Wednesday.

I suppose the “sinister” adjective still applies. Although IG funds saw inflows, the five-week exodus from high yield sums to almost $14 billion.

Notwithstanding the late-week swoon, stocks still aren’t listening. It’s the “same story with institutions,” Hartnett said, flagging “big outflows from cash” and the “largest 10-week inflow to stocks in 10 years.”

{kind=link}

The financial media has done an excellent job of selling “buy the dip.”

Dip buyers maintain stability. If there was no dip buying in the last two years where would we be?

Without any chips? Oh, nevermind.

It is always good to remember that every market transaction has two sides, each of which believes that doing what they are doing will make them more money than doing something else or they wouldn’t do it. Half of all market participants believe the other half is wrong and this difference of opinion creates the space for transactions to take place.

I don’t see widespread bargains in US stocks, defining “bargain” as substantial (>10%) upside to fair value. This is after doing a bottoms up valuation of the entire SP500.

The only way I can see such is if you cut risk free rate by about 100 bp (10 yr at 100 bp) while keeping FCF growth at current consensus, two assumptions that seem antithetical.

Similar conclusion using multiple-based valuations.

I do see attractive upside in some sectors with relatively small index weight. Also in a couple of the mega-cap names, the ones with the worst looking charts.

There’s an argument that everything including the kitchen sink has been thrown at stocks, referring to 5 rate hikes + QT + yield curve inversion, yet the indices have stabilized, so it is time to buy. None of those things have actually happened, so the conclusion feels premature. And whether the indicies have in fact stabilized can change in a couple days.

As the yield on shorter duration Treasury bonds rises, the relative appeal of sectors that pay dividends diminishes: consumer staples, utilities and REITS. The Tech stocks that have high valuations and are valued on price/sales have lost their appeal in arising rate environment. And the dollar is rising nicely as Fed will be forced to remove liquidity due to inflation which I suspect will rise further since supply chain improvement has stalled due to trucker protests and crude oil spot continues its ascent. So the sectors which will attract more capital have narrowed: energy, materials, big-cap tech with predictable revenues (sans FB, Netflix).

I went very overweight REITs and energy early last year, now working down the former and figure the latter is getting close to top. Financials that are not sensitive to yield curve look good, The bond proxy sectors might be winners in 2H, if economy rolls over and takes long rates with it. Generic industrials feel risky but I bought some defense contractors last year, for obvious reasons. Really don’t see a lot of leadership groups.

My BTI is smoking hot!

Has anyone reported on how thousands of truckers were able to coordinate such a big blockade. Where they egged on by social media’s invisible hands, whosever they might be.

Citizen Band Radio Breaker Breaker

H-Man, it could be the fish are making pods to lessen the effect of the sharks. We know how that ends?