It was liquidation time across the cryptoverse on Saturday.

At one point, Bitcoin dropped to ~$34,000, 50% below its all-time high. That equated to a roughly $600 billion selloff, measuring from the peak (figure below).

The CEO of Alpha Impact, a social crypto trading platform which also offers staking, stated the obvious in remarks to Bloomberg: Margin calls were afoot. Data from Coinglass suggested liquidations during crypto’s multi-day swoon were the highest since the December 3 flash crash.

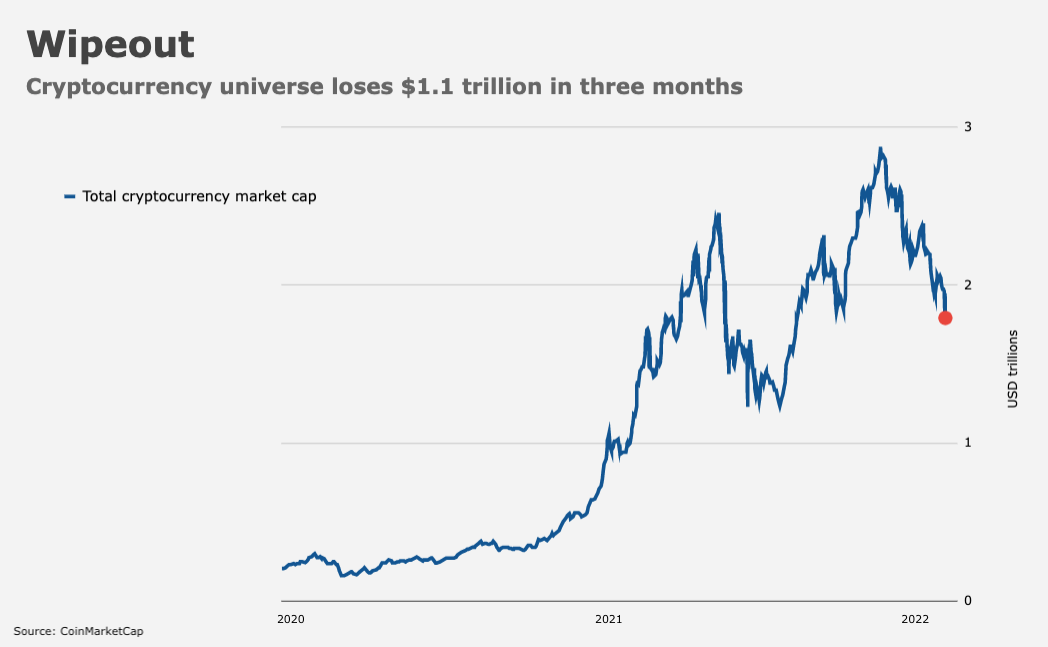

Total crypto market cap fell to $1.58 trillion on Saturday, the lowest in nearly six months and down some $1.3 trillion from record highs reached less than three months ago.

There’s a sense in which this is a meaningless discussion. Even at $20,000, Bitcoin is impossible to fathom. The gains since inception may as well be incalculable. To say the genie is out of the bottle would be a good early candidate for understatement on the 21st century.

In a good piece on Dan Morehead and Pantera, Bloomberg put a number to the immeasurable. Morehead “launch[ed] his first crypto fund when a Bitcoin cost less than a bag of groceries,” the linked article said. “As a result, the Pantera Bitcoin Fund has returned more than 65,000% since 2013.”

The same article found Morehead, who traded bonds at Goldman and worked for Julian Robertson, describing bets on a secular decline in bond yields and inflation as a trade that “basically made my career.” Given that, he’s acutely aware of the risks associated with rising inflation and, more to the point, the extent to which relatively zealous policy tightening from central banks has the potential to weigh on prices for assets deemed speculative — assets like Bitcoin, and crypto more generally.

Bitcoin is trading in tandem with US tech shares, which just suffered their worst one-week rout since the onset of the pandemic thanks to an ongoing surge in US real rates catalyzed by expectations of aggressive rate hikes from the Fed.

The accompanying losses for Ethereum, Solana and Avalanche would be described as catastrophic if they played out in traditional assets over such a compressed time frame (figure below).

Of course, some crypto adherents would say that’s just “another week at the office,” so to speak. The difference this time is that there’s a policy catalyst — a macro driver.

That’s not to say everyone who’s panic-selling their crypto is doing so based on an assessment of what higher risk-free rates mean for the fundamental bull case. My point, rather, is that crypto is now bound up with traditional assets thanks to heightened interest and increased investment in the space. Somewhat ironically given that mainstream recognition was (and still is) part of the bull case, that link may be a liability in 2022 if long duration US equities succumb to a painful, drawn-out de-rating predicated on tighter monetary policy.

The greatest irony of all, though, is the juxtaposition between Morehead’s scathing critique of the Fed’s presence in the US bond market and the implications for crypto of the central bank’s attempt to reduce their footprint.

“The biggest Ponzi scheme in history is the US government and mortgage bond market all being driven by one non-economic actor with a dominant position who is trading based on material, non-public information,” he said, in a December 7 note. This week, in a piece dated January 18, he wrote that,

Ponzi schemes keep going until the perpetrator is stopped from the outside. They never stop of their own volition. Bernie Madoff kept going until federal agents arrested him. Senator Manchin and 7.0% CPI growth are what stopped this one. The Fed is far out on their Wile E. Coyote moment. Financial gravity just locked on. If you have not yet sold your bonds to the Fed, you might want to. By March they’ll be out of the bond manipulation business. They won’t do it again in my lifetime. If you are thinking of refinancing your mortgage, do it quickly. With the Fed shut down, mortgage rates will revert to the free-market rate. We will likely never see these rates again.

I imagine that passage will resonate with some readers, but for crypto adherents, I’d suggest this is a “be careful what you wish for” moment.

If the Fed were to, say, hike rates five times in 2022 and become an active seller of the assets in SOMA (as opposed to just letting the balance sheet run down “naturally”), it’s very likely that real rates would embark on a determined trek higher. If the economic outlook were to falter simultaneously, pushing breakevens lower, the situation could worsen materially, driving real rate differentials dramatically in favor of the greenback.

Such a scenario (which, frankly, seems likely to play out in some form) would be highly destabilizing for crypto, especially to the extent any attendant weakness in richly-valued growth shares forced big players with concentrated positions to liquidate their riskiest exposure.

Crypto enthusiasts may initially take some pleasure in seeing the Fed’s quantitative easing Ponzi scheme unravel. But the near-term fallout is unlikely to benefit Bitcoin, let alone any other coins. Crypto, blockchain and DeFi may well be the future. But as we saw in March of 2020, the vast majority of humanity still lives in the past. That means when something really goes wrong, all anyone wants is US dollars.

{kind=link}

Fiat currency backed by governments is the present not the past. Crypto is the new gold attempting to enslave people by virtue of nothing other than it’s own self righteousness. Those at the top of the food chain love creating new gods for the Poor to bow to.

It is a force that I hope regular people never need to be impoverished by. Gold caused enough harm around the world

In what way is crypto really a solution unless of course you were there first

The one good thing about crypto is that the young will become interested in macroeconomics and monetary policy as they search for answers to why Bitcoin, Pudgy Penguins, and “stable”-coins (backed by the faith and credit of Madoff-copycats) became worth less than Chuck E. Cheese tokens over the next years.

It’s pretty ironic crypto enthusiasts don’t see that their coins are based on pyramid schemes where people “stake” stable coins to get absurd returns. The way things are going, either stablecoins entice newcomers with better yields (to compete with reals) or they run out of bag holders and collapse (become unable to redeem tokens for fiat). As we know, increasing yields in a pyramid scheme shortens its lifespan. At some point, the only way to sell stablecoins will be to buy some non-pegged coin and sell it for fiat, further collapsing that coin.