When the headlines start to get repetitive, it usually means everyone’s on the same side of the boat. And unbalanced boats are prone to capsizing.

The problem right now is that although various trades associated with a rotation away from perennial secular growth winners look crowded, mega-cap tech remains one of the most crowded trades on the planet.

On a quick stroll through the “Markets” section of Bloomberg’s public website Wednesday, I was subjected to a trio of headlines touting a tight oil market, “dwindling” spare capacity and resilient demand.

Beneath those stories: A file picture of a forlorn Cathie Wood gazing off into the wild blue yonder and a piece dedicated to that Treasury options strike I mentioned Tuesday in “This Is ‘The Most Critical Level In Global Markets.'”

If you’re the contrarian type, you know what to fade. The figure (below) shows energy sprinting ahead of tech in the new year.

Over the last two weeks, energy outperformed tech by the most since the original Pfizer vaccine announcement. As Cameron Crise noted on Tuesday, outside of November 2020, it’s been two decades since energy bested tech by a comparable margin.

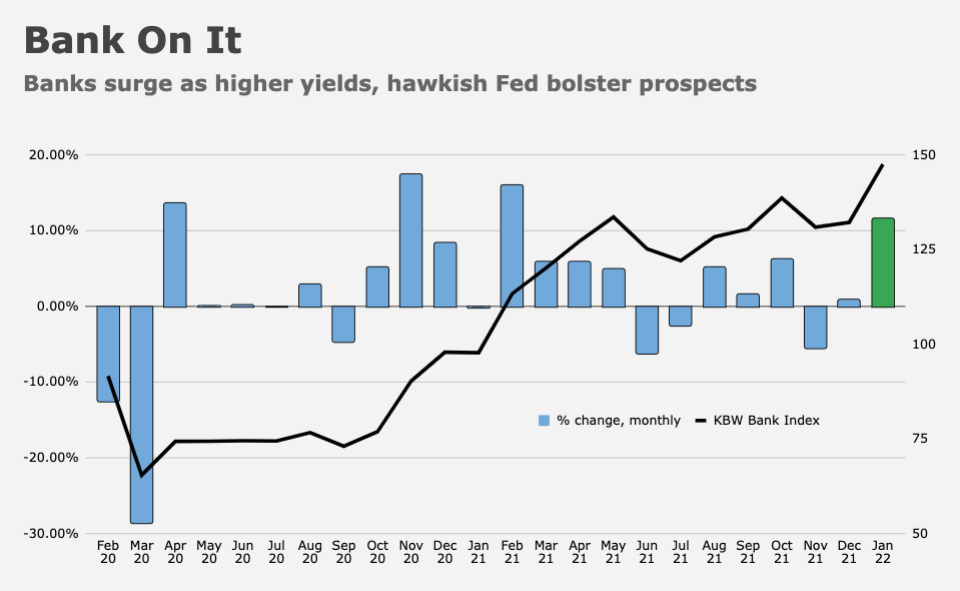

It’s a similar story with banks. Although steep earnings-day losses for JPMorgan and Goldman took some of the shine off financials, banks started 2022 on a ridiculous run. Even with steep losses logged over the past several sessions, the KBW Bank Index is still up more than 6% for the month.

All of the above was captured vividly in this month’s installment of BofA’s Global Fund Manager survey. “FMS investors drastically cut their net OW to tech to 1%,” down 20% MoM, the bank’s Michael Hartnett remarked, in the color accompanying the poll results. That, he wrote, is “the lowest level since December of 2008.”

You’ll note from the visual (above) that tech has virtually never been out of favor in the post-financial crisis era.

Remember, when it comes to Info Tech, it’s not just about great companies, although that’s obviously a big part of the US tech story. Over the past dozen years, secular growth stocks benefited handsomely from the “slow-flation” macro environment.

The notion that we’ve now transitioned to a new macro regime characterized by hot nominal growth, higher rates and elevated inflation is part and parcel of many a bull case for cyclical value in 2022 — and many an attendant “rotation” call.

The idea that the macro has shifted durably in favor of cyclicals and value stocks was also reflected in the BofA survey, which showed the net allocation to banks jumped 20% from December to 41%, near record highs seen five years ago (figure on the left, below).

Meanwhile, the net allocation to commodities hit a new record (figure on the right).

Coming full circle, these trades are becoming consensus, even as many market participants (and strategists) are understandably reluctant to give up on the bull case for mega-cap US tech, given the sheer ubiquity of the FAAMG cohort in the everyday lives of countless people all around the world.

There’s a very real sense in which FAAMG is synonymous with existence, but then again, so is banking (until more people take the plunge into DeFi, anyway) and so are commodities (as long as people need to stay warm and eat). The difference is, sluggish growth and subdued inflation favored tech for a decade, thus providing a macro kicker for company-specific, fundamental bull cases.

For whatever it’s worth, Ned Davis Research just abandoned their outright bullish stance on US stocks for the first time in 15 months, citing model changes and “evidence” that Fed and earnings cycles are maturing.

“A neutral US equity outlook incorporates expectations for positive, albeit lower, returns,” Ed Clissold said, in a note. “The reduction in risk appetite is not an outright bearish call.”

{kind=link}

Oh great, now I’m scared of what’s working AND what’s not working . . . absolutely right, it is a scary market.

H-Man, this storm will make landfall soon. It will then be time to sort the debris.

I think we’re just getting notification that a storm might form. I’m girding for a long term (5+ years akin to the 2000s) asset devaluation. With the double punch of monetary and fiscal tightening, we’re overshooting into recession territory. Given we’ve learned from previous tightening errors, it might take longer for a crisis to trigger easing again.

There’s no way to know that. For all you know, The Fed may backtrack and pivot hard again, like Jay Pow’s infamous volte-face in Q42018. But they may allow markets to experience some more pain before then – as harrowing as it has been, the drawdown has not been steep enough to invoke the Fed put.

Energy was identified as a growth opportunity right around the time inflation was being dismissed as transitory. As it began to rise, the US responded with tapping reserves and prices abated, temporarily and everyone went back to congratulating themselves on being smarter than the analysis. Fast forward 3 months and the predictive data sets for both inflation and energy prove to be correct.

Knowing the catalyst for inflation (The CPI bad kind not all the great kinds people want to keep seeing) I don’t really see how Fed policy will alter the trajectory we are on. Covid simply won’t go away, it keeps mutating and infecting people. Maybe not killing them but maybe leaving them with permanent long Covid. We are not the masters of our own universe, we are learning the harsh reality of our ancestors. That disease can dominate the most dominant species on the planet. It is unironic to me that how we were able to so easily invade the Americas is because of the very thing we’re trying to pretend like isn’t a problem. It is projected that the flu, measles, black plague, and dysentery wiped out millions of indigenous people in the America’s after Columbus arrived and before colonists started showing up.