“Markets can handle Omicron and higher yields,” JPMorgan strategists led by Marko Kolanovic wrote Monday, as traders continued to press bets on a March Fed hike while analysts debated the ramifications of tighter monetary policy for richly-valued US shares amid sharply higher real rates.

While there’s a strong consensus building around three (or four) Fed hikes in 2022 and the onset of balance sheet runoff (possibly as soon as spring), opinions vary on the outlook for equities.

Certainly, most agree that higher reals are an impediment for growth shares, tech and particularly so-called “hyper-growth,” as exemplified by the Cathie Wood complex. Ark’s flagship product was down another ~3% by midday Monday following an 11% rout during 2022’s opening week.

But the jury is still out on the fate of equities as an asset class. “As usually happens when real yields rise substantially over a short period of time and market depth is low, VIX spiked and risk markets de-rated,” Kolanovic and co. said, recapping markets’ reaction to the release of the December Fed minutes. “While we already knew from the December dot plot that FOMC participants saw hikes ‘sooner or at a faster pace,’ what was new were the clues given to how balance sheet normalization would play out.”

The figure on the left (below) shows diminished liquidity across both stocks and bonds. Impaired liquidity can lead to outsized moves, which then feed on themselves. Market depth is inversely correlated to volatility.

The figure on the right (above) is interesting in the context of the “2018 redux” thesis. “A key difference versus 2018 is that, at the time, real rates were rising to the more challenging >1% region, which was out of sync with falling PMIs,” JPMorgan said Monday, noting that in 2022, reals are simply catching up to a macro environment characterized by strong growth and inflation.

Like Goldman, JPMorgan pointed to the rolling over of the latest COVID wave in South Africa and encouraging (albeit nascent) signs of improvement out of the UK.

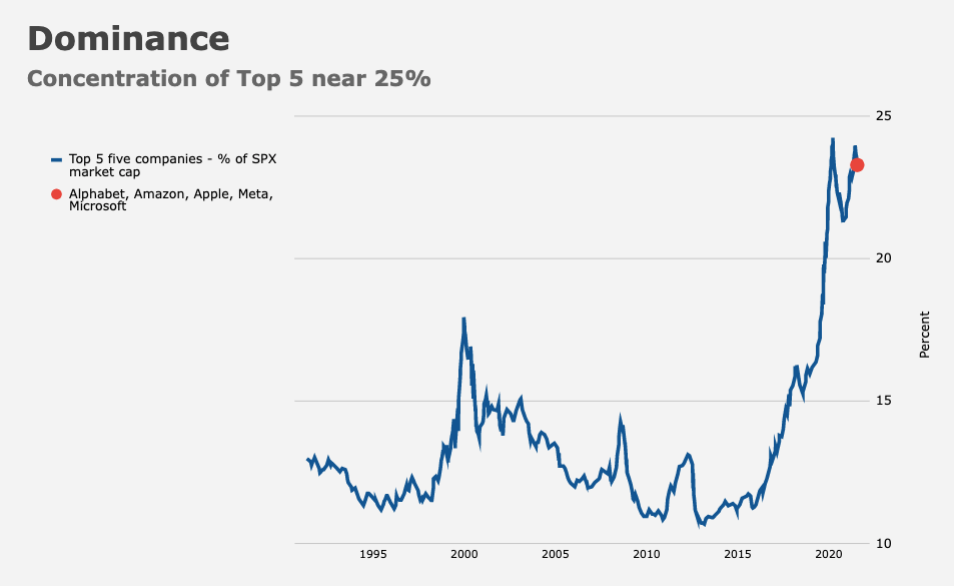

Although the bank acknowledged downside risks to economic output in the near-term, and also the possibility that a swoon in heavily-weighted, large-cap growth stocks could weigh on the broader market precisely because the “broad” market isn’t so broad in the US, where the Top 5 names comprise nearly 25% of market cap, the bank is constructive. Recent tumult, Kolanovic, Nikolaos Panigirtzoglou and Bram Kaplan suggested, is another manifestation of frayed nerves.

“Whether it is Fed news or the Omicron scare, [last] week’s moves highlight the fragility of sentiment since the onset of COVID,” the bank said, adding that “generally speaking, the bouts of risk aversion that have stalled the reflation and reopening trades have proven to be overdone, initially with Delta and now with Omicron, in addition to earlier worries about faster central bank normalization.”

With the caveat that fragile sentiment can become self-fulfilling (Kolanovic didn’t say that explicitly on Monday, but he talked at length about the importance of confidence during the selloff that occurred in Q4 of 2018, when the Fed last engaged in simultaneous hikes and balance sheet runoff), JPMorgan ventured there’s “a good chance we are coming to the end of this period of fragile sentiment, although it may take a few weeks for the market to process the Fed’s incremental changes and Omicron’s beneficial (yes, beneficial) impact as the more dominant, less severe strain.”

In a survey of JPMorgan clients conducted from December 13 through January 7th, 65% said they were likely to increase their equity exposure over the coming days and/or weeks. 84% said they were inclined to cut duration in their bond portfolio.

{kind=link}

You must be logged in to post a comment.