The holiday lull began to set in Wednesday — finally.

The arrival of Omicron and the ensuing deluge of dour news flow made for a somewhat harrowing December, as rising volatility collided with year-end dynamics to upend markets anew.

It’s a somewhat morbid analogy, but COVID is a bit like the villain in an 80s slasher flick. As Jamie Kennedy’s Randy put it in Scream (the clever 1996 classic in which the protagonists relied on horror movie clichés to survive their own small town nightmare), “Careful. This is the moment when the supposedly dead killer comes back to life, for one last scare.” (As it happens, Scream is being rebooted for 2022).

“Volume is a function of volatility, and the latter had been pushed higher by Omicron fears, worries over US stimulus and hawkish pivots at the Fed and other central banks,” Bloomberg’s Eddie van der Walt wrote Wednesday. “For now, it seems as if global financial markets are finally approaching their Christmas slumber.”

“Volatility has been on the move in the final weeks of 2021, with unusually high volatility of VIX futures,” Goldman’s Rocky Fishman wrote, in a note dated December 21. He called elevated vol-of-VIX “a fitting end to a year characterized by sharp transitions between low and high realized volatility.”

Fishman noted that so far this month, the median VVIX is higher than the median in February of 2018, around “Vol-pocalypse,” as market participants affectionately refer to the day when the VIX ETP complex imploded. Not only that, it’s also “higher than any calendar month outside of H1 2020,” Fishman remarked.

He went on to call outsized swings in vol a reflection of a market “trying to balance the potential for weakening liquidity and systematic funds’ selling to drive up volatility in a further selloff, versus increased clarity around key catalysts potentially driving realized volatility back toward mid-2021 lows.”

As a reminder, one-month realized vol spiked hard amid the Omicron scare, triggering large de-leveraging flows from systematic cohorts.

In the course of recapping the “straight line” rally from Monday’s lows into Tuesday’s turnaround, JonesTrading’s Mike O’Rourke called a return to all-time highs on the S&P “highly plausible in the thin holiday trading environment of the next two weeks.” “US equity trading volumes were approximately 11% slower” on Tuesday versus Monday, he said.

Last week, JPMorgan’s Marko Kolanovic cited thin markets and the necessity of closing out hedges and shorts as potential catalysts for a year-end squeeze. On Tuesday, Nomura’s Charlie McElligott suggested risk assets may get some “relief” as liquidity “should really begin deteriorating from here on out into year-end.”

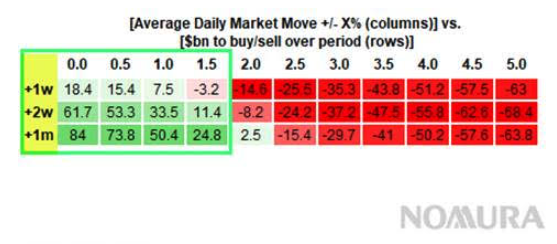

After massive de-leveraging on the back of the spike in realized vol, McElligott said CTAs and vol control strats “are likely to be substantial sources of mechanical demand for equities” going forward.

The table (above) shows potential vol control adds assuming smaller daily changes.

Meanwhile, BofA saw large equity inflows across all client groups last week. Excluding buybacks, inflows have been the largest in three months over the past four weeks, the bank’s Jill Carey Hall and Savita Subramanian said.

In the same short blog post mentioned above, Bloomberg’s van der Walt delivered a warning reminiscent of Randy’s famous line from Scream. “Buyer (and seller) beware,” he said. “These times of thin liquidity and the current decade’s penchant for delivering surprises should mean none of us can drift too far away from a terminal screen.”