“Are you a buyer of dips?”, an anchor asked a guest, during a painfully generic television interview on Monday afternoon in the US.

A continual source of amusement for me is unmuting financial news at random intervals, catching anchors and guests mid-sentence and then using the soundbites in articles.

The quote (above) came from a discussion between Bloomberg TV’s Romaine Bostick and someone I didn’t recognize. Later in the show, Bostick and his colleagues engaged one another in a comically contrived recap of a Bloomberg article juxtaposing a recent note by Goldman’s Peter Oppenheimer with the latest from Morgan Stanley’s Mike Wilson. “He’s a smart guy,” someone said, of Wilson.

After five or so minutes, I hit the mute button again. If you’re wondering, Bostick’s guest is a buyer of dips. And the consensus among Bloomberg’s afternoon anchors is that Wall Street thinks a small correction is coming. “It’s just a matter of when.”

It’s tantalizing stuff. And the best thing about buying a Samsung Crystal UHD TV is that they come with a handful of free HD channels now, one of which, inexplicably, is Bloomberg. In ultra high definition. So, on Sundays, if there’s no golf on and you’re out of Klonopin, you can drift off to sleep by watching reruns of last week’s Bloomberg programming in eye-watering 4K.

I’m just kidding. Sort of. Bloomberg TV is infinitely better than CNBC, but no-data Mondays in mid-December offer slim pickings when it comes to producing compelling programming, and the fact that US equities were perched at record highs coming off their second best week of 2021 took the edge off Monday’s selloff.

Ostensibly, market participants were worried about Omicron. An Oxford study provided fresh evidence of the variant’s capacity to evade vaccines and Boris Johnson said someone died with the strain in the UK. But, as Tom Essaye wrote, it’s “really all about the Fed and whether it meets market expectations” this week.

BMO’s Ian Lyngen and Ben Jeffery captured the give-and-take between virus concerns and the primacy of the year’s final FOMC meeting. “As headlines regarding delayed return-to-office schedules (once again) complicate the next phase of achieving the ever-elusive new normal, it follows that investors are growing increasingly apprehensive on the growth front [but] it’s far too soon for the Fed to backtrack its characterization of pandemic-linked disruptions at this stage, therefore we continue to see Wednesday’s risks skewed toward the hawkish side,” they wrote, adding that “this dynamic will only serve to exacerbate the dueling macro narratives; on one hand, the Fed’s efforts to combat inflation will keep yields in the front end of the curve anchored to the upside [while] growth concerns have manifested in a bid for duration.”

Long-end yields were richer by as much as seven basis points on the day. The 5s30s flattened inside of 60bps again. As discussed at length here over the weekend, there’s a compelling argument for flattening pressure from both ends. The short-end from the perception that the Fed will bring forward hikes and the long-end from concerns about the impact of an accelerated tightening cycle on growth. Potential Omicron “drag” is another excuse for the long-end to rally. That was evident on Monday.

In “Event Risk,” I wrote that while strategists are certainly justified in being wary of policy tightening, especially vis-à-vis a US equity market that’s propped up on deeply negative real rates, one might suggest the subtle tendency for investors to reclassify COVID as a source of ambiguity rather than a source of risk, is itself a risk.

As it happens, the latest edition of BofA’s credit investor survey, dated Monday, underscored my point almost to the letter. “Based on our survey, investors seem to think there is only one risk that matters: A policy error by central banks,” the bank’s Barnaby Martin wrote, adding that,

Almost half of those surveyed say this is their major concern, close to the largest reading ever for a top concern. Investors feel entrenched inflation will end the era of central bank predictability, with forthcoming rate hikes being quicker, bigger and more chaotic than in the past. Note that 2021 has already delivered a historic 75 net rate hikes, surpassing the intensity of the 2011 hiking cycle. And “Dr. Yield Curve” (the 5s30s global government bond curve) has drastically flattened, and is now within 20bps of its all-time low. What of the “big nothings”? December’s survey shows no concern over global recession, debt sustainability, an equity market correction, geopolitics or shareholder-friendly activity. And just 5% say COVID lingering is their top concern for 2022.

That’s anecdotal evidence to support my contention that investors may have become too single-minded in their risk assessment.

Additionally, that passage (from Martin) lends credence to the idea that, because taking a view on the distant future is mostly impossible due to ambiguity around pandemic cross currents and the longer run consequences of unprecedented stimulus, markets have defaulted to obsessing over the only thing to which odds can still be assigned — the near-term path of monetary policy.

That entails trying to assess the level of panic at the Fed over inflation. Not easy, but certainly easier than predicting how many times a virus might mutate over the course of a half-decade, what those mutations might mean for supply chains, and so on.

As BMO’s Lyngen went on to say, there’s “a strong argument to be made that Tuesday and Wednesday represent the two final trading days of the year.” Although it wouldn’t be wise to “completely dismiss the final two weeks of 2021,” Lyngen said that at least as it relates to rates, he and Jeffery “are open to the notion that investors will have the bulk of the fundamental/policy insight in hand once Powell’s press conference concludes.”

Again, all that matters is the Fed.

Postscript

As you consider all of this, don’t forget to take account of the totality of the easing impulse.

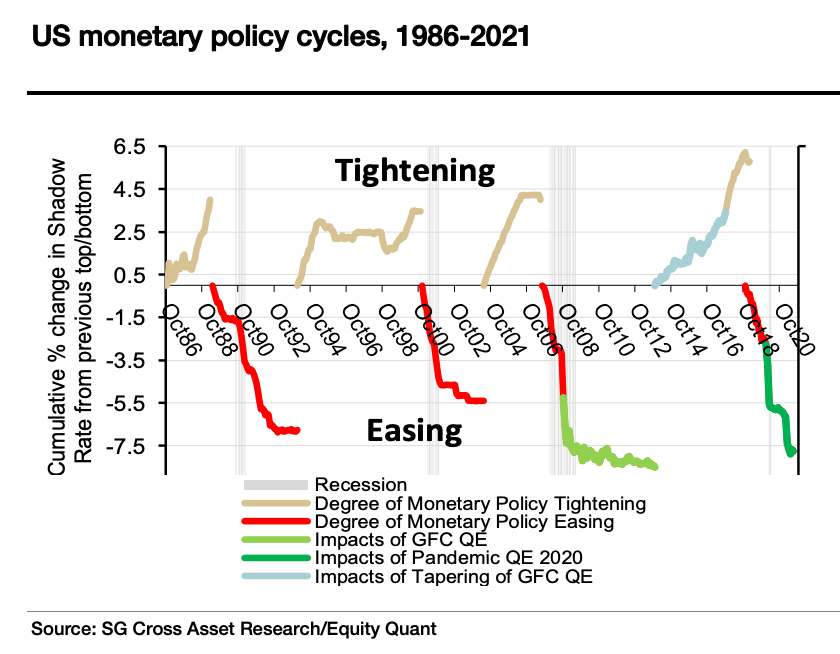

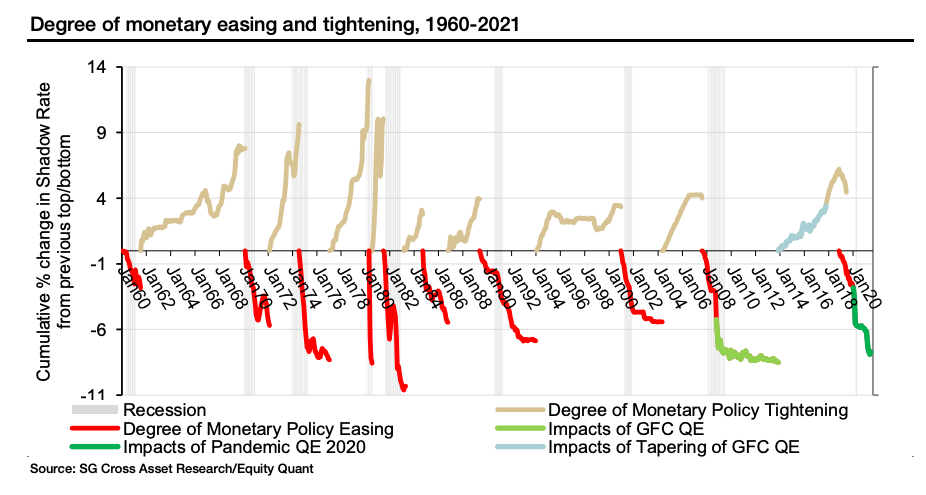

If you measure from the lows in the shadow rate (which accounts for unconventional easing), the last tightening cycle was the most acute in decades (figure below).

“The monetary policy stance of a central bank is difficult to judge from the official policy rate when the latter is constrained by the zero bound,” SocGen’s Solomon Tadesse reminded market participants last month.

As measured from peak tightening in mid-2018, the total decline in short rates during the current easing phase which began in July of 2019 was nearly -8% by May of this year. That, Tadesse remarked, was on par with the amount of accommodation seen across the entire GFC and post-financial crisis easing phase from September of 2007 to November of 2013.

Simply put: It’s the implicit short rate that matters when you assess the stance of monetary policy in the post-GFC world.

Powell’s rate hikes in 2018 hardly pushed US rates to historically high levels. But the totality of the tightening impulse (which obviously began prior to his tenure) summed to nearly 650bps.

That’s a lot. Even if you zoom out to capture six decades of monetary easing and tightening in the US (figure above).

H-Man, it is the pre-game show waiting for the kick off on Wed. Just a bunch of blubbering over the same old, same old. Tuesday will bring nothing more than the same meandering squabble. Sorta like waiting for a hurricane to make land fall.

Likely.

To be fair, with the death toll from COVID becoming manageable, it’s fair to consider the health situation an ambiguity rather than a massive risk anymore. Unless you happen to be in one of the at-risk category, of course (old, overweight etc).

should the tightening or easing by done in nominal or real space, just asking?