On the heels of a massive three-day rally on Wall Street, analysts are raising their 2022 year-end S&P targets.

That’s a joke. I mean, it’s technically true, but the implication (that just-released targets for the benchmark are being revised higher in real time based on daily swings) is misleading. Banks typically project the index at least a couple of years out, so there were 2022 targets for the S&P long before this year’s batch of year-ahead outlooks made the rounds.

Nevertheless, I, for one, chuckled to see Credit Suisse hike their forecast just a day after the S&P succeeded in largely erasing its Omicron/Powell-inspired swoon.

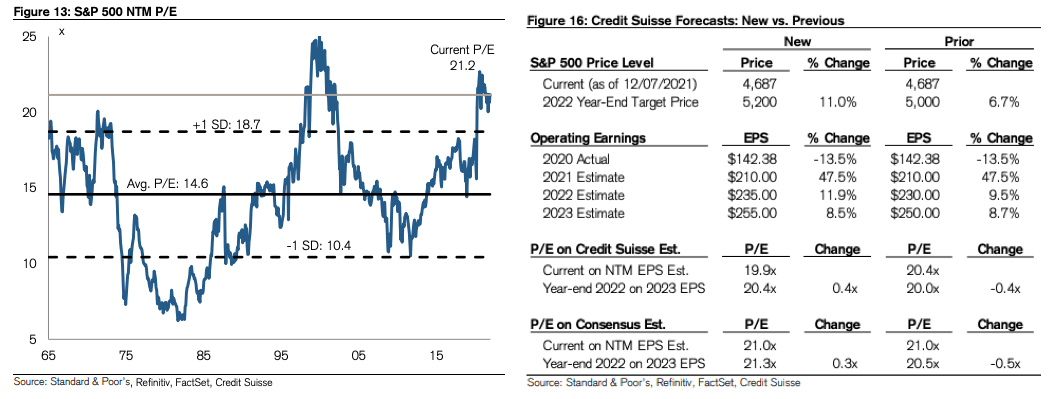

“We are raising our 2022 S&P 500 price target to 5,200 from 5,000,” the bank’s Jonathan Golub declared, in a Wednesday note. He cited “robust projections for economic growth in both real and nominal terms, further margin upside in cyclical groups, a pickup in buybacks and a favorable discount rate despite Fed tightening.”

The shaded area in the simple figure (below) shows the down-trade that accompanied the emergence of the variant and Jerome Powell’s abandonment of the “transitory” characterization of inflation.

Credit Suisse also sees $5 more in index-level earnings both for next year and 2023. The bank’s previous estimates baked in a corporate tax hike, an outcome Golub “no longer expects.”

Notably, he doesn’t expect the index to de-rate either. Part and parcel of many a cautious outlook is the notion that a relatively hawkish Fed and rising real rates will force at least some modest multiple contraction. Even constructive outlooks (e.g., UBS’s 5,000 forecast) assume some risk to valuations.

By contrast, Credit Suisse assumes 8.5% EPS growth for 2023 and a half-point expansion of the S&P’s forward multiple (figures below from the note).

“We believe that tight spreads and low interest rates will support modest valuation upside,” Golub said.

I suppose what I’d add is that notwithstanding the temptation to enumerate everything that can go wrong, it’s sometimes useful to take a step back and otherwise flip your internal sarcasm switch off in the interest of assessing the situation dispassionately. Stocks typically rise. If you predict a down year for US equities, history isn’t on your side, especially not recent (i.e., post-GFC) history.

Consider that even if the Fed accelerates the taper, they’ll still be expanding the balance sheet through Q1. And even if, by some cosmic miracle, the Committee finds the courage to hike three times in 2022, that increase would still leave rates extraordinarily low. All of that is to say nothing of the fact that the Fed isn’t thinking of actually letting the balance sheet run down. The Fed will probably never be an active seller of the assets it holds, and certainly not anytime soon.

Toss in the corporate bid and assume no disastrous turn in the pandemic, and you’re left to ponder who really deserves the sarcastic derision — bullish analysts or the cynical comedian that whispers in your ear and lives in your Twitter feed.

Meanwhile, BofA’s data showed buybacks by corporate clients accelerated to their highest weekly level since March last week.

![]()

“Previously we had not seen any evidence of corporates accelerating buybacks into year-end given tax reform risk,” the bank said, in a note dated December 7.

Hedge funds, institutional clients and private clients were all net buyers too, Jill Carey Hall wrote, adding that client inflows of $6.7 billion “were the largest since 2017” and the biggest as a percentage of US market cap since December of last year.

Does that make dumb money thats been in btfd mode the smart money?

The eternal question that haunts every PM on the planet: “What if I’m the dumb money?”

“I’ll see your 5,000 (oh wait, that was my bet!) and raise you 200…..and pass me the bottle of Jack!!!”

H-Man,

The variables shrink — Omicron is going to the back of the bus. Not sure about the treasury comment. Current debt 28T Government owned debt 6T. Private investors 16T. The 6T Govies will sit. The 16T in Private will move to higher rates.

Just up to the Fed to raise the rates.