Over the weekend, I noted that the marked spike in realized vol precipitated by last week’s post-Thanksgiving down-trade on Wall Street had the potential to trigger de-leveraging from the vol-control universe.

Although Monday found stocks rebounding to reclaim some of the egregious losses logged on “Red Friday,” it was back to risk-off on Tuesday amid another set of foreboding Omicron headlines.

Moderna CEO Stephane Bancel told FT that the variant may challenge vaccine efficacy, while Dow Jones said Regeneron’s COVID-19 antibody cocktail loses effectiveness against Omicron, or at least in preliminary tests.

George Yancopoulos, Regeneron’s chief scientific officer, said the company has developed other treatments which it believes may retain their effectiveness.

“What we have to admit is, in the course of the past six days, our urgency has increased,” Yancopoulos remarked. “What started out as a backup plan has now been made a lot more urgent.”

Separately, Dow Jones reported that Eli Lilly’s cocktail may lose some of its effectiveness when confronted with the variant as well.

Read more:

‘This Is Not Going To Be Good’: Moderna Execs Spook Markets

Nosebleed Markets Ponder Uncertain Year-End In Latest Virus Panic

All of this had the potential to drive up volatility and tip dominoes, although the usual caveats apply: Everyone needs more information.

There was still a palpable sense of panic, and generally speaking, panicked traders don’t make the best decisions. Fingers crossed that early reports suggesting the variant produces only “mild” symptoms prove some semblance of accurate.

“With this new information, markets are again suddenly pivoting back to being concerned that global leaders — particularly in Europe — are at risk of going back to the failed playbook of growth-killing lockdowns, despite the Biden pledge yesterday to avoid using them in the US,” Nomura’s Charlie McElligott said.

He described policymakers’ decision calculus as extremely asymmetric. There’s “effectively no bar to ease versus a very high bar to hike,” he wrote, citing Jerome Powell’s allusion to the possibility that the variant could further delay a return to full employment stateside.

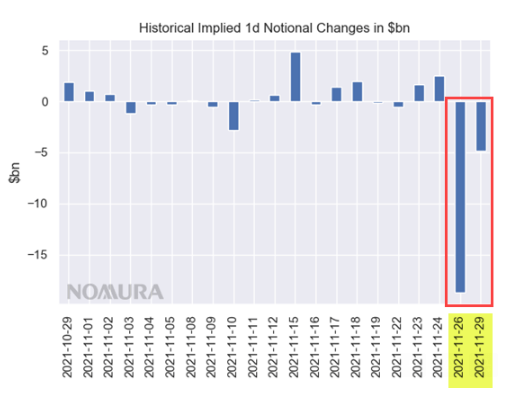

As for equities and the impact of a volatility expansion tied to the latest COVID scare, McElligott wrote that “the ‘true-ing up’ of rVol to iVol, which knee-jerked trailing Vol window inputs powerfully higher, has had a profound impact on systematic target vol / risk control strategies, trigger[ing] a substantial two-day exposure reduction via Equities futures selling.”

The bank’s model suggests vol control de-allocated to the tune of nearly $24 billion in US equities futures over two days. The overall allocation to stocks is now down to the 64th%ile from the 76th prior to Omicron.

The market, Charlie went on to say, is “open to an ongoing exposure reduction in coming days in almost all daily-change scenarios, but especially if we were to see sustained ~1% or greater moves.”

Dealers are now perilously close to short gamma versus spot territory in SPX, while we’re already there in small-caps.

The read-through is familiar. “You’re not getting a lot of ‘stabilization help’ here from dealer hedging flows,” McElligott remarked. “So with this backdrop of vol / risk control selling, CTA signal pivots and dealers increasingly in short Gamma territory, we should then too think about discretionary longs.”

After getting burned, the discretionary crowd may now be inclined to protect their year instead of playing offense into what, just a week ago, seemed like a semi-ideal setup for a year-end rally. Seasonality can’t save the market from Mother Nature.

Don’t forget debt ceiling dramatics to come shortly. You’d like to think that Republicans would realize this is not a time to play brinksmanship, but I’m not hopeful as their goal appears to be 1) sink the ship 2) blame Biden for sinking the ship.

Is Santa really supposed to thread the needle between 11/30 and 12/15 or between 12/16 and 12/24? He’s too fat for that.

I’m still in derisking mode.

H-Man, the data on Omicron suggests it may not have legs. If that gets confirmed before the December meeting, rates will be rocking since all eyes will be on inflation and it will be Powell leading the charge to tame the demon.