“Serene progress.”

That amusing characterization of global equities’ monumental post-pandemic rally comes from a 64-page, 2022 global strategy piece published Sunday by Morgan Stanley. (‘Tis the season for year-ahead outlook tomes.)

The figure on the left (below) is certainly indicative of “progress.” If you like policy jokes, you might call it “substantial further progress.”

The figure on the right (above) shows the pace of inflows to global equity funds rebounding to ~$24 billion per week, as stocks look to post a second consecutive monthly gain after erasing September’s swoon, the only substantial setback of the year.

If you read Morgan’s macro outlook, you’d be forgiven for thinking the bank must be bullish. They conceded as much. “At face value, our global macro forecasts suggest a continued benign backdrop for equities in 2022 with strong nominal (and real) GDP growth, moderating inflation through the year and no rate hikes from any of the G3 central banks,” Mike Wilson, Graham Secker and Jonathan Garner (hereafter shortened to “Wilson”) wrote.

Alas, a look “underneath the surface” suggests stocks are likely to exhibit more volatility going forward, the bank said.

Their rationale is simple enough. Earnings momentum is bound to wane, yields will probably rise and companies are staring down a laundry list of gale-force margin headwinds.

US stocks are most exposed, Wilson said, noting that “the persistent price outperformance of MSCI USA versus MSCI ACWI for much of the last decade has been driven by superior and more durable EPS trends.”

The bank expects “solid” earnings growth for corporate America next year, but flagged significant ambiguity attributable to elevated costs, persistent supply chain frictions and what Wilson somewhat euphemistically called “tax and policy uncertainty that’s unique to the US.”

It’s against that backdrop that profit trends have diverged from performance (figure on the left, below) while the valuation gap remains very large (figure on the right).

European and Japanese shares aren’t as exposed. Indeed, the record valuation disparity between US shares and the rest of the world is at least partly attributable to the dominance of richly-valued growth stocks, some of which are highly sensitive to rising yields.

As Wilson wrote, “the US’s high exposure to growth stocks means that its relative performance has been inversely correlated to real bond yields in recent years.” The bank sees real yields rising “materially” next year, quite possibly to the detriment of secular growth shares like those which dominate US benchmarks (figure below).

Note that concentration risk in US shares has never been higher than it is currently.

But isn’t it rare for US shares to underperform? Yes. But also no. American exceptionalism (in the market context) is in part the product of the “slow-flation” macro environment, which favored secular growth shares.

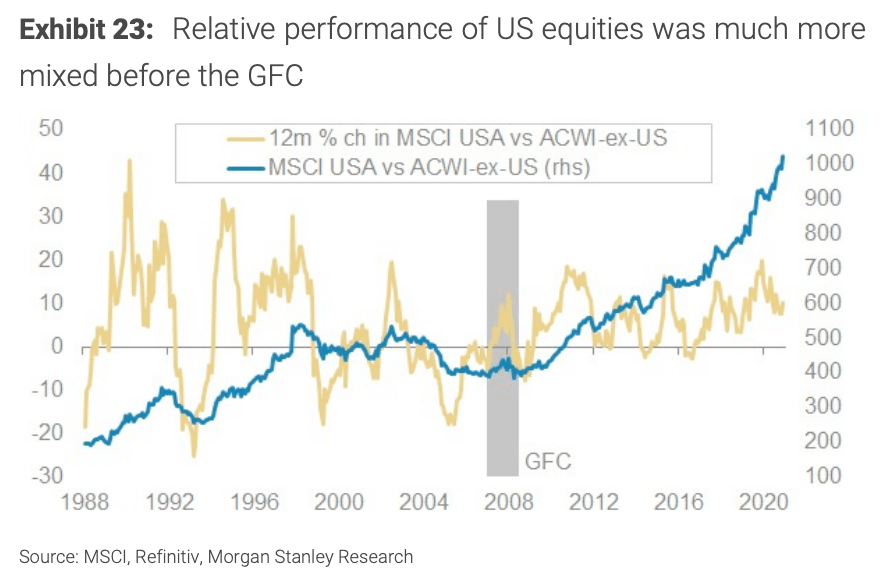

“US equity underperformance has been rare post-GFC, but the secular backdrop may be shifting,” Morgan’s equity strategists wrote, adding that “after a decade of strong and steady outperformance from US stocks, the potential for their sizable underperformance versus global peers may seem unlikely, but it is worth noting that such occurrences were not so uncommon before the GFC.” The figure (below) illustrates the point.

So, you can thank secular stagnation for massive US outperformance.

If we are, in fact, entering a new macro regime defined by more robust nominal growth, Morgan suggested that “a return to pre-GFC performance patterns” is “more plausible.”

Ultimately, the bank’s base case for the S&P in December of 2022 is 4,400, representing 5% downside from current levels. By contrast, European shares will rise 8%, Japanese shares 12% and emerging market equities 3% over the same 13-month window.

As the bank’s Andrew Sheets put it, “mid-to-late cycle environments are generally supportive for equities outright, and relative to other assets,” but Morgan is looking for “valuations that are reasonable enough and fundamentals that are sustainable enough to not buck that trend.”

Europe and Japan fit the bill, especially considering the ECB and the BoJ are less likely to be forced into tightening by inflation pressures.

Moreover, Morgan doesn’t see as much evidence of “over-earning and excessive profitability” in those markets.

Remember: In today’s political environment, “over-earning and excessive profitability” are out of style.

How accurate has “Wilson” been on prior predictions, over the past 3-5 yrs?

Wilson actually had a pretty good record recently.